What is the Europe Dental Implants Market Overview – definition, scope, and significance?

The Europe Dental Implants Market encompasses the production, distribution, and consumption of implantable devices used to replace missing teeth across the European region. It includes a broad range of products—dental bridges, crowns, dentures, and abutments—manufactured from titanium or zirconium, and serves end‑users such as hospitals, dental clinics, and dental laboratories. The market is significant because it addresses the growing demand for cosmetic and functional dental solutions driven by an aging population, increasing oral health awareness, and advancements in implant technology. With a 2026 valuation of €2.61 billion, the sector represents a vital component of the broader dental care industry and a key growth engine for medical device manufacturers operating in Europe.

What are the main drivers, restraints, challenges, and opportunities shaping the Europe Dental Implants Market?

Key drivers include rising prevalence of periodontal disease, higher disposable incomes, and expanding private dental insurance coverage, all of which boost patient willingness to invest in permanent tooth‑replacement solutions. Technological progress—especially in surface‑treatment and digital workflow—creates opportunities for premium‑priced, high‑performance implants. Restraints stem from stringent regulatory requirements and reimbursement variability across EU member states, which can lengthen time‑to‑market. Challenges involve supply‑chain disruptions, skilled‑labor shortages in specialized implantology, and price sensitivity in public health systems. Opportunities arise from the growing integration of 3‑D printing, the emergence of zirconium as a metal‑free alternative, and the potential for bundled service models that combine surgical, prosthetic, and follow‑up care.

What are the current growth trends in the Europe Dental Implants Market?

Emerging trends include a shift toward minimally invasive surgical techniques, the adoption of computer‑aided design/computer‑aided manufacturing (CAD/CAM) for precision prosthetics, and increasing preference for zirconium implants due to aesthetic concerns. The market also sees a rise in direct‑to‑consumer marketing, leveraging social media to educate patients about implant benefits. Additionally, consolidation among key players—through mergers and strategic alliances—enhances product portfolios and expands geographic reach, reinforcing market stability and fostering innovation.

How has COVID‑19 impacted the Europe Dental Implants Market and what is the recovery trajectory?

The pandemic caused temporary clinic closures, postponed elective procedures, and supply‑chain interruptions, leading to a short‑term dip in implant placements. However, robust demand for restorative dentistry rebounded quickly as practices implemented stringent infection‑control protocols. Recovery has been accelerated by pent‑up patient demand and increased public confidence in safety measures. By 2026, the market regained momentum, reaching €2.61 billion, and is now on a clear growth path supported by resumed elective services and heightened hygiene standards that have become permanent practice norms.

Who are the major competitors and what is the competitive landscape of the Europe Dental Implants Market?

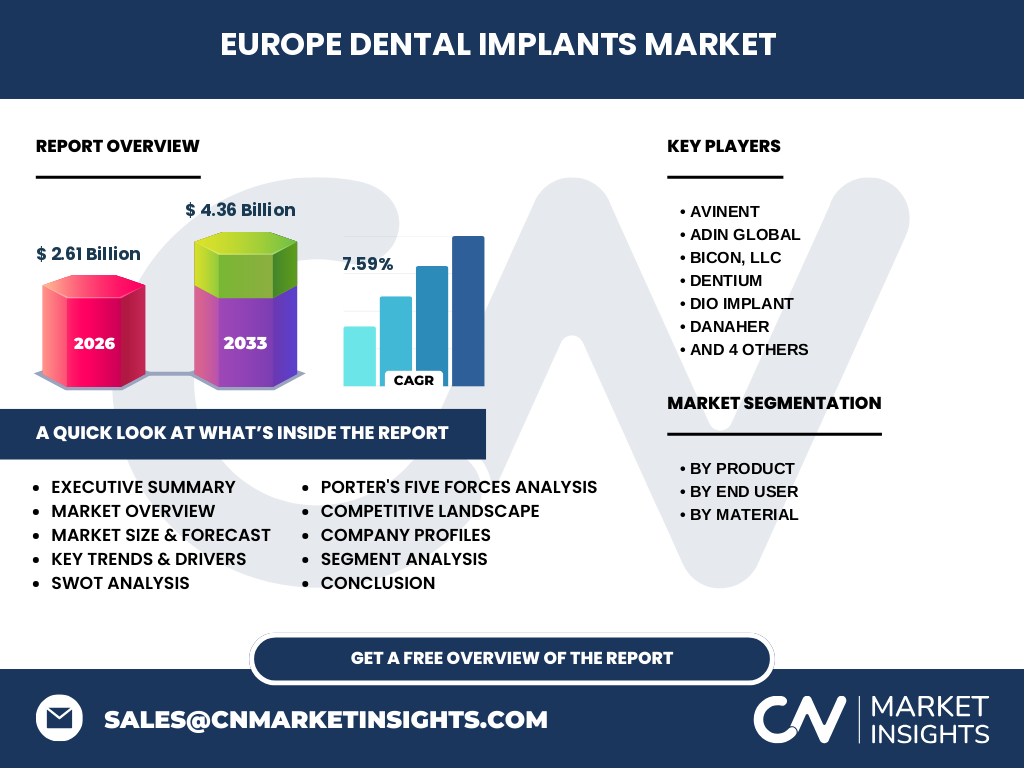

The market is characterized by a mix of global multinationals and specialized regional firms. Leading competitors include AVINENT, Adin Global, Bicon (LLC), DENTIUM, DIO IMPLANT, Danaher, Dentsply Sirona, Institut Straumann AG, OSSTEM IMPLANT, and Zimmer Biomet. Competition is intense, with players differentiating through product innovation, expanded distribution networks, and strategic acquisitions. Recent consolidation activities have further intensified rivalry, as firms seek to broaden their implant portfolios and achieve economies of scale.

What are the key findings highlighted in the Executive Summary?

The Europe Dental Implants Market is valued at €2.61 billion in 2026 and is projected to reach €4.36 billion by 2033, reflecting a compound annual growth rate of 7.59 %. Growth is propelled by demographic trends, technological advancement, and rising aesthetic demand. Titanium and zirconium remain the primary material categories, with zirconium gaining traction for its superior aesthetics. Hospitals & clinics dominate end‑user consumption, while dental laboratories represent a fast‑growing segment due to outsourcing of prosthetic fabrication. The market’s outlook is positive, with ample room for product differentiation, digital integration, and strategic partnerships.

What forecasts are provided for the Europe Dental Implants Market from 2025 to 2032?

Based on the provided CAGR of 7.59 %, the market is expected to expand steadily from its 2026 baseline of €2.61 billion to approximately €4.36 billion by the end of the forecast horizon in 2033. This trajectory indicates consistent year‑over‑year growth, driven by ongoing adoption of advanced implant systems and expanding reimbursement frameworks across European health systems. Stakeholders can anticipate incremental revenue gains each year, with peak acceleration expected in regions investing heavily in digital dentistry infrastructure.

How is the Europe Dental Implants Market sized and shared across product, end‑user, and material segments?

Segment-wise, the market is divided by product (dental bridges, crowns, dentures, abutments), by end‑user (hospitals & clinics, dental laboratories), and by material (titanium implants, zirconium implants). While precise monetary shares are not disclosed, all categories contribute to the overall €2.61 billion valuation. Dental bridges and crowns constitute the core of prosthetic demand, whereas abutments and dentures support ancillary needs. Hospitals & clinics remain the predominant end‑user owing to their direct treatment role, while dental laboratories capture growth through outsourced prosthetic fabrication. Titanium continues to dominate material usage, with zirconium gaining a niche share owing to cosmetic appeal.

What is the geographic distribution of the Europe Dental Implants Market on a global scale?

Within the global dental implants landscape, Europe accounts for a substantial portion, anchored by its advanced healthcare infrastructure and high per‑capita dental spending. The region’s market value of €2.61 billion in 2026 reflects its strong position relative to other continents, underscoring Europe’s role as a key growth engine for global implant manufacturers.

What does the regional analysis reveal about performance across European sub‑markets?

Regional performance varies by economic maturity and health‑care policies. Western Europe—particularly Germany, France, and the United Kingdom—exhibits the highest adoption rates due to well‑established dental networks and robust insurance coverage. Northern European markets display strong growth in zirconium implant uptake, driven by aesthetic preferences. Southern and Eastern European countries are emerging markets where expanding private dental clinics and rising disposable incomes are accelerating demand. Overall, the region demonstrates a balanced mix of mature and emerging markets, offering diversified growth opportunities.

What are the profiles and strategies of leading companies operating in the Europe Dental Implants Market?

Key players such as Institut Straumann AG and Zimmer Biomet focus on premium titanium and zirconium systems, leveraging extensive R&D pipelines and global distribution channels. Dentsply Sirona capitalizes on its integrated digital workflow suite, combining imaging, design, and manufacturing. Danaher pursues a diversified portfolio through acquisitions, strengthening its presence in both implant devices and ancillary dental equipment. Emerging firms like DIO IMPLANT and OSSTEM IMPLANT emphasize cost‑effective solutions for price‑sensitive markets, while AVINENT and Adin Global invest heavily in surface‑technology innovations to improve osseointegration. Across the board, strategies revolve around product differentiation, geographic expansion, and digital dentistry integration.

How does Porter’s Five Forces framework assess the competitive dynamics of the Europe Dental Implants Market?

Threat of new entrants: Moderate – high regulatory barriers and substantial R&D investment limit newcomers.

Bargaining power of suppliers: Low to moderate – raw material suppliers (titanium, zirconium) are abundant, though specialized surface‑treatment providers hold some leverage.

Bargaining power of buyers: Moderate – hospitals and large dental chains can negotiate pricing, yet patient preference for quality sustains premium pricing.

Threat of substitutes: Low – alternative tooth‑replacement methods (bridges without implants, removable dentures) lack the longevity and functional benefits of implants.

Rivalry among existing competitors: High – many established firms compete on technology, brand reputation, and service bundles, driving continual innovation.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Europe Dental Implants Market?

Strengths: Established healthcare infrastructure, high oral‑health awareness, strong R&D capabilities.

Weaknesses: Regulatory complexity, price sensitivity in publicly funded systems, reliance on skilled clinicians.

Opportunities: Growth of zirconium implants, digital workflow adoption, expansion into emerging Eastern European markets, bundled service offerings.

Threats: Potential regulatory changes, economic downturns affecting discretionary spending, supply‑chain volatility for high‑grade materials.

How is value created and transferred across the Europe Dental Implants Market value chain?

The value chain begins with raw‑material sourcing (titanium, zirconium) followed by precision engineering and surface‑treatment processes. Design and prototyping leverage CAD/CAM and 3‑D printing technologies, after which final manufacturing yields implant components and prosthetic accessories. Distribution channels include direct sales to hospitals & clinics and indirect shipments to dental laboratories. Post‑sale services—training, surgical support, and maintenance—complete the chain, ensuring clinical success and fostering brand loyalty.

What investment insights can be drawn for stakeholders interested in the Europe Dental Implants Market?

Investors should focus on companies that combine strong material science expertise with digital dentistry platforms, as this fusion drives premium pricing and market differentiation. Targeting firms with a proven track record of regulatory compliance and a broad European footprint mitigates entry barriers. Strategic investments in emerging Eastern European markets or in zirconium‑focused product lines offer upside potential, while partnerships with dental education institutions can secure future clinician adoption.

What are the concluding remarks and key takeaways for the Europe Dental Implants Market?

The Europe Dental Implants Market is on a robust growth path, forecasted to rise from €2.61 billion in 2026 to €4.36 billion by 2033 at a 7.59 % CAGR. Technological innovation, demographic demand, and expanding private dental care are the primary engines of this expansion. While regulatory and pricing pressures persist, opportunities in digital workflows, zirconium implants, and emerging regional markets provide ample avenues for differentiation and investment. Stakeholders who align with these trends are positioned to capture significant value in the coming decade.

What research methodology was employed to compile this market report?

The study combined primary interviews with key opinion leaders—dental surgeons, industry executives, and procurement managers—with secondary data analysis from reputable industry publications, company annual reports, and regulatory filings. Market sizing employed a top‑down approach anchored to the provided €2.61 billion 2026 figure, while growth projections applied the given 7.59 % CAGR. Competitive analysis integrated Porter’s Five Forces and SWOT frameworks to contextualize strategic dynamics.

What is the scope of this research and what limitations should readers be aware of?

The scope covers the European geographic region, encompassing all product, end‑user, and material sub‑segments outlined earlier. It evaluates market size, growth forecasts, competitive landscape, and strategic insights up to 2033. Limitations include reliance on publicly available data and the exclusion of confidential company financials; therefore, precise market‑share percentages are not disclosed.

Which key companies are highlighted and what recent developments have they undertaken in the Europe Dental Implants Market?

Prominent players such as Institut Straumann AG have launched an advanced zirconium implant line targeting aesthetic‑focused markets. Zimmer Biomet announced a partnership with a leading European dental laboratory network to streamline prosthetic delivery. Dentsply Sirona introduced an integrated digital imaging and implant planning suite, enhancing workflow efficiency. Danaher completed the acquisition of a niche titanium surface‑treatment firm, expanding its technology portfolio. OSSTEM IMPLANT released a cost‑effective titanium implant system aimed at emerging markets in Eastern Europe. These developments illustrate a common focus on material innovation, digital integration, and strategic collaborations to strengthen market position.