1. Europe Meter Data Management System Market Overview - Definition, scope, and significance?

The Europe Meter Data Management (MDM) System market comprises software platforms and associated services that collect, validate, store, and analyze consumption data from electricity, gas, and water meters. These systems enable utilities to automate meter reading, support billing accuracy, and provide actionable insights for demand‑side management, regulatory compliance, and grid modernization. The scope extends across residential, commercial, and industrial end‑users, covering smart‑grid, micro‑grid, energy‑storage, and EV‑charging applications. In a region where sustainability targets and digitalization mandates are strong, MDM solutions are essential for enabling reliable, real‑time data flows that underpin smart‑city initiatives and the transition to low‑carbon energy systems.

2. Europe Meter Data Management System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the EU’s ambitious decarbonization goals, increasing penetration of smart meters, and the need for advanced analytics to optimize grid operations. Regulatory pressure for accurate billing and consumer‑level transparency further fuels adoption. Opportunities arise from emerging use cases such as EV‑charging integration, demand‑response programs, and the rollout of micro‑grids and storage assets that require granular data. Restraints involve high upfront investment costs for legacy utility overhauls and data‑privacy concerns under GDPR. Challenges stem from fragmented standards across countries, the complexity of integrating heterogeneous devices, and a shortage of skilled data‑analytics talent within utilities.

3. Europe Meter Data Management System Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from on‑premise solutions toward cloud‑based, SaaS MDM platforms that offer scalability and faster deployment. Utilities are increasingly embracing AI‑driven analytics for predictive maintenance and load forecasting. An emerging trend is the convergence of MDM with IoT ecosystems, enabling real‑time communication between meters, DERs (distributed energy resources), and control systems. Interoperability standards such as OpenADR and IEC 61850 are gaining traction, facilitating seamless data exchange across multi‑utility environments. Finally, the rise of edge computing is allowing preliminary data processing at the meter level, reducing latency for critical grid‑balancing functions.

4. COVID-19 Impact on the Europe Meter Data Management System Market - Pandemic effects and recovery trajectory?

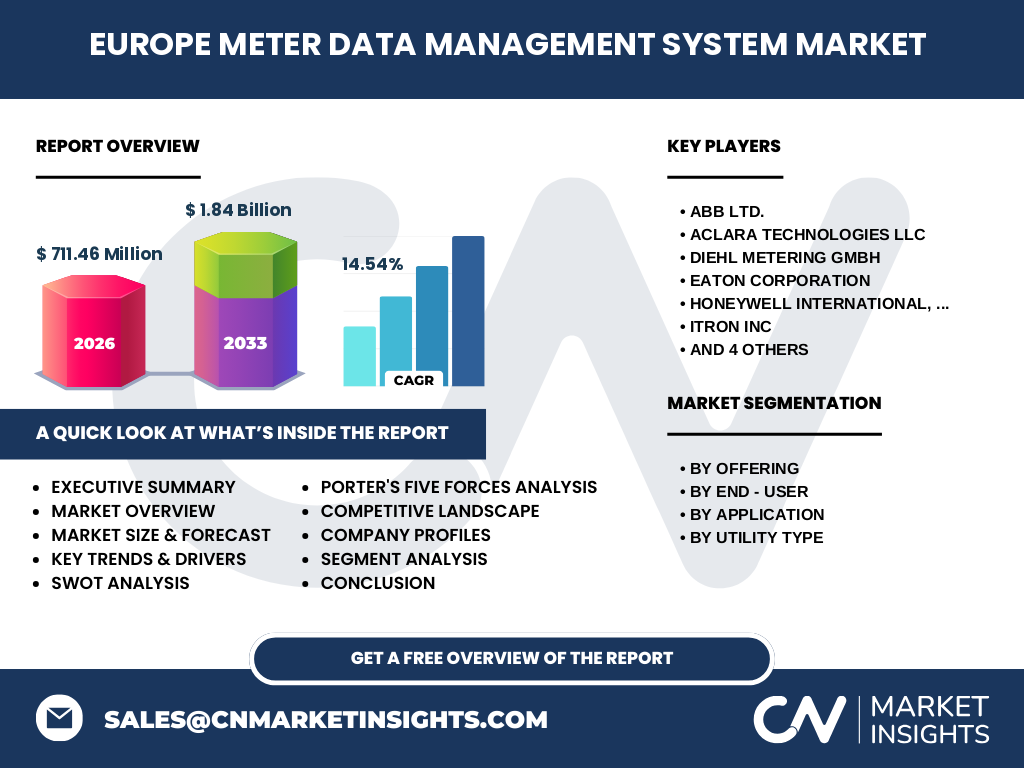

The COVID‑19 pandemic initially slowed field installations due to lockdowns and workforce restrictions, causing a short‑term dip in new project launches. However, the crisis accelerated digital transformation as utilities sought remote monitoring capabilities to maintain service continuity. Post‑2020, investment momentum rebounded, with utilities prioritizing non‑contact meter reading and automated data collection. The recovery trajectory is positive, reflected in the market’s projected CAGR of 14.54% and a forecasted size of 1.84 billion by 2033, indicating strong confidence in long‑term growth despite the temporary pandemic disruption.

5. Europe Meter Data Management System Market Competitive Landscape - Major competitors and market consolidation?

The market is highly competitive, featuring global OEMs and specialist software firms. Key players include ABB Ltd., Aclara Technologies, Diehl Metering, Eaton Corporation, Honeywell International, Itron Inc., Kamstrup A/S, Landis+Gyr Group, Schneider Electric, and Siemens AG. Consolidation activity is moderate, with strategic acquisitions aimed at expanding portfolio breadth (e.g., larger utilities acquiring niche analytics startups) and geographic reach. Partnerships with cloud providers and telecom operators are common to enhance connectivity and data‑hosting capabilities.

6. Executive Summary - High-level overview and key findings about Europe Meter Data Management System Market?

The Europe MDM market stands at 711.46 million in 2026 and is projected to reach 1.84 billion by 2033, driven by a robust 14.54% CAGR. Growth is powered by regulatory mandates, smart‑meter rollouts, and the need for integrated data platforms supporting smart‑grid and EV‑charging initiatives. Cloud‑based solutions, AI analytics, and edge computing are shaping the technology landscape. While investment costs and data‑privacy regulations pose challenges, the market offers ample opportunities for innovators delivering interoperable, secure, and scalable MDM services. Leading vendors are consolidating capabilities through acquisitions and strategic alliances.

7. Europe Meter Data Management System Market Forecast - Projections for 2025-2032 period?

Starting from a 2026 base of 711.46 million, the market is expected to expand steadily, reaching approximately 1.84 billion by 2033. This reflects a compound annual growth rate of 14.54% across the forecast horizon. The upward trajectory is underpinned by continued smart‑meter penetration, expanding EV‑charging infrastructure, and increasing utility interest in data‑driven grid optimization. The forecast suggests that by 2032, annual market intake will be close to the 1.8‑billion mark, indicating sustained investment in both software and services segments.

8. Europe Meter Data Management System Market Size and Share by Segmentation - Breakdown by segment?

By offering, the market divides into software and services, with software capturing the larger portion due to the shift toward cloud platforms and analytics tools. Services, including integration, maintenance, and consulting, complement software adoption and represent a growing share as utilities outsource complex deployments. End‑user segmentation shows residential as the dominant segment, driven by mass smart‑meter installations, followed by commercial and industrial sectors where advanced analytics and demand‑response are more pronounced. Application-wise, smart‑grid solutions lead, while micro‑grid, energy‑storage, and EV‑charging applications are gaining traction. Utility‑type segmentation indicates electricity as the primary focus, with gas and water utilities also investing in MDM to meet digitalization targets.

9. Global Europe Meter Data Management System Market Size and Share by Region - Geographic distribution?

Europe accounts for a substantial share of the global MDM landscape, reflecting the region’s early adoption of smart‑metering policies and strong regulatory frameworks. While specific global figures are not disclosed, Europe’s market size of 711.46 million in 2026 underscores its leading position, with growth expected to outpace other regions due to coordinated EU initiatives and high renewable‑energy integration demand.

10. Regional Analysis of the Europe Meter Data Management System Market - Detailed regional market performance?

Western Europe, particularly Germany, the UK, France, and the Benelux countries, shows the highest penetration of advanced MDM solutions, fueled by mature electricity markets and aggressive decarbonization roadmaps. Northern Europe, led by Scandinavia, emphasizes renewable integration and micro‑grid projects, driving demand for flexible MDM platforms. Southern Europe is accelerating smart‑meter rollouts to improve grid resilience, while Central and Eastern European markets are in earlier adoption phases but benefit from EU funding programs that support digital infrastructure upgrades.

11. Leading Company Profiles in the Europe Meter Data Management System Market - Industry players and strategies?

ABB Ltd. leverages its broadband automation expertise to deliver end‑to‑end MDM suites integrated with grid‑control systems. Aclara Technologies focuses on middleware that bridges legacy meters with cloud analytics. Diehl Metering offers modular hardware‑software combos tailored for gas and water utilities. Eaton Corporation expands its offering through energy‑management platforms that include MDM capabilities. Honeywell International emphasizes security‑focused cloud services. Itron Inc. provides a comprehensive portfolio from smart meters to advanced analytics. Kamstrup A/S specializes in water‑meter data solutions. Landis+Gyr Group capitalizes on its strong presence in electricity metering. Schneider Electric integrates MDM within its broader IoT ecosystem, and Siemens AG combines MDM with its grid‑automation portfolio. Most firms pursue partnerships with cloud providers and invest in AI/ML to differentiate their solutions.

12. Porter's Five Forces Analysis of the Europe Meter Data Management System Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and complex standards act as barriers, yet niche software startups can enter via SaaS models. Bargaining power of buyers is strong as utilities demand customized solutions and competitive pricing. Bargaining power of suppliers is low to moderate; hardware components are commoditized, while software talent is scarce, slightly increasing supplier influence. Threat of substitutes is limited; alternative manual reading methods are inefficient and non‑compliant. Industry rivalry is intense, with many global players competing on technology, service quality, and integration capabilities.

13. SWOT Analysis of the Europe Meter Data Management System Market - Strengths, weaknesses, opportunities, threats?

Strengths: Robust regulatory support, growing smart‑meter base, and high demand for data‑driven grid optimization. Weaknesses: High implementation costs and fragmented standards across countries. Opportunities: Expansion into EV‑charging data management, micro‑grid integration, and AI‑enabled predictive services. Threats: Data‑privacy regulations, cyber‑security risks, and potential market saturation in mature utility segments.

14. Europe Meter Data Management System Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with meter manufacturers producing intelligent devices, followed by communication infrastructure providers enabling secure data transmission. Next, software developers create MDM platforms that aggregate and process the data. System integrators and consultants deliver installation, customization, and training services. Utilities act as the primary customers, using the processed data for billing, grid management, and regulatory reporting. Finally, third‑party analytics firms may layer additional insights for demand‑response or market‑participation services.

15. Key Investment Insights in the Europe Meter Data Management System Market - Strategic investment recommendations?

Investors should target companies that combine strong software capabilities with proven integration services, especially those offering cloud‑native, AI‑enhanced platforms. Partnerships with telecom and cloud providers can accelerate market reach. Acquiring niche analytics or cybersecurity startups can bolster a vendor’s value proposition. Funding projects that enable cross‑utility data sharing (electricity, gas, water) presents a differentiated growth avenue, given the EU’s push for integrated resource management.

16. Europe Meter Data Management System Market Conclusion - Summary and key takeaways?

The Europe MDM market is on a rapid growth path, driven by regulatory imperatives, smart‑meter modernization, and the rise of distributed energy resources. With a projected market size of 1.84 billion by 2033 and a 14.54% CAGR, the sector offers lucrative opportunities for technology innovators and service providers. Success will hinge on delivering interoperable, secure, and analytics‑rich solutions that meet utility needs across residential, commercial, and industrial segments.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with senior utility executives, technology vendors, and industry analysts, alongside secondary data collection from regulatory reports, vendor disclosures, and reputable market databases. Trend analysis, CAGR calculations, and scenario modeling were used to project market size to 2033. Competitive mapping was based on product portfolios, recent contracts, and financial disclosures of the identified key players.

18. Research Scope - Coverage and limitations?

The research covers the European MDM market across software and services, all end‑user categories (residential, commercial, industrial), and applications including smart‑grid, micro‑grid, energy storage, and EV‑charging. It addresses electricity, gas, and water utilities. Geographical scope includes all EU and EEA member states. Limitations stem from the reliance on publicly available financial figures and the exclusion of proprietary vendor pricing data.

19. Key Companies and Recent Developments in the Europe Meter Data Management System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ABB Ltd. announced a cloud‑based MDM platform integrated with its grid‑automation suite, targeting large utility customers. Aclara Technologies launched a programmable API that eases integration with third‑party analytics tools. Diehl Metering introduced a water‑metering data hub supporting GDPR‑compliant cloud storage. Eaton Corporation released an energy‑management dashboard that combines MDM data with demand‑response signals. Honeywell International partnered with a leading European telecom to enhance low‑latency connectivity for real‑time meter data. Itron Inc. unveiled a next‑generation smart‑meter firmware that reduces data latency for EV‑charging stations. Kamstrup A/S expanded its water‑MDM solution into the Nordic market through a joint venture. Landis+Gyr Group secured a multi‑year contract with a German utility for a unified electricity‑MDM system. Schneider Electric integrated its EcoStruxure™ platform with AI analytics to offer predictive maintenance for micro‑grids. Siemens AG announced a strategic acquisition of a niche AI‑analytics start‑up to strengthen its MDM offering for industrial customers.