What is the Talc Market Overview – definition, scope, and significance?

The talc market comprises the mining, processing, and distribution of talc mineral, a magnesium‑silicate known for its softness, lubricity, and chemical inertness. Its scope extends from raw ore extraction to value‑added products used in a wide range of end‑use industries such as plastics, ceramics, paints & coatings, rubber, pharmaceuticals, food, and pulp & paper. Talc’s significance lies in its role as a multifunctional filler that enhances product performance, reduces manufacturing costs, and meets stringent regulatory standards, making it a critical input in both consumer and industrial applications worldwide.

What are the Talc Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include growing demand for lightweight polymers in automotive and packaging, increased consumption of high‑performance ceramics, and expanding pharmaceutical and food applications that require chemically pure talc. Restraints stem from environmental concerns related to mining activities and regulatory scrutiny over talc purity, especially in cosmetics and pharma. Challenges involve volatile raw‑material prices and the need for continuous compliance with safety standards. Opportunities arise from innovations in talc beneficiation, development of talc‑based nanocomposites, and rising investments in emerging markets that are upgrading their manufacturing infrastructure.

What are the current Talc Market Growth Trends?

Current trends show a shift toward talc grades with higher purity and lower iron content to meet stringent quality requirements in food and pharmaceutical sectors. Manufacturers are also focusing on sustainable mining practices and circular economy models, recycling talc‑containing waste streams. Additionally, the integration of talc in polymer nanocomposites is gaining traction, driven by the demand for materials that combine strength, thermal stability, and lightweight characteristics.

How has COVID‑19 impacted the Talc Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in talc mining operations and logistics, leading to modest supply constraints in 2020‑2021. Simultaneously, demand from end‑use sectors such as automotive plastics declined, while medical‑grade talc saw a brief uplift due to increased pharmaceutical production. Recovery began in late 2021 as supply chains normalized and demand rebounded across most industries, with the market now on a robust growth path toward the 2027‑2033 forecast horizon.

What does the Talc Market Competitive Landscape look like?

The competitive landscape is characterized by a mix of large multinational miners and specialized regional players. Major competitors such as Imerys SA, Minerals Technologies Inc, and Elementis Plc dominate worldwide supply, while companies like Golcha Minerals Pvt Ltd and Sun Minerals Pvt Ltd focus on emerging market niches. Recent years have seen strategic acquisitions and joint ventures aimed at expanding geographic reach and broadening product portfolios, indicating a moderate level of market consolidation.

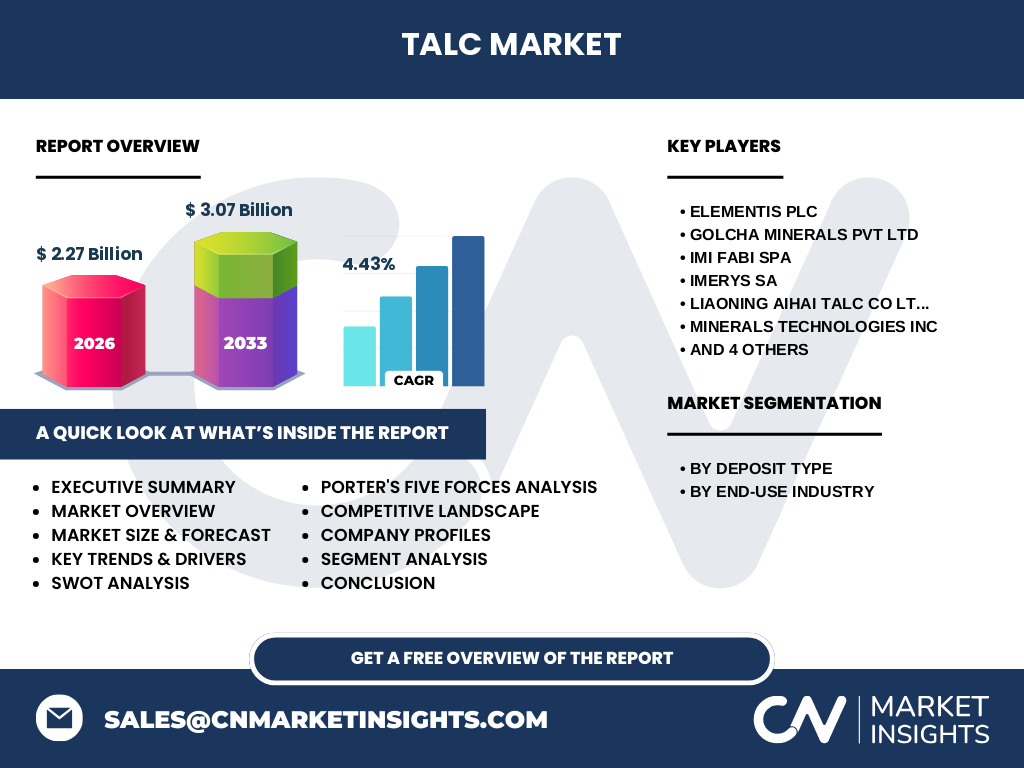

Can you provide an Executive Summary of the Talc Market?

The global talc market was valued at USD 2.27 billion in 2026 and is projected to reach USD 3.07 billion by 2033, expanding at a CAGR of 4.43 %. Growth is propelled by expanding end‑use applications, especially in lightweight plastics, high‑performance ceramics, and regulated pharmaceutical and food sectors. Despite environmental and regulatory challenges, the market benefits from technological advances in mineral processing and increasing demand for sustainable filler solutions. Leading players are strengthening positions through acquisitions, capacity expansions, and product innovation.

What are the Talc Market Forecasts for 2025‑2032?

Based on the provided CAGR of 4.43 %, the talc market is expected to maintain steady growth through 2032. The forecast indicates a gradual increase in demand across all major end‑use segments, with plastics and ceramics showing the strongest upside due to automotive lightweighting trends and high‑temperature applications. The market’s value trajectory reflects continued investment in mining capacity, higher‑purity product development, and expanding geographic penetration, particularly in Asia‑Pacific.

How is the Talc Market Size and Share divided by segmentation?

Segmentation by deposit type includes Talc Chlorite and Talc Carbonate, each serving distinct processing requirements and end‑use specifications. By end‑use industry, the market is categorized into Plastics, Pulp & Paper, Ceramics, Paints & Coatings, Rubber, Pharmaceuticals, and Food. While precise share percentages are not disclosed, plastics and ceramics traditionally command the largest portions due to their volume requirements, whereas pharmaceuticals and food occupy niche but high‑value segments demanding ultra‑pure talc.

What is the Global Talc Market Size and Share by Region?

The global market, valued at USD 2.27 billion in 2026, is geographically distributed across North America, Europe, Asia‑Pacific, and Rest of World. Asia‑Pacific holds a substantial share driven by rapid industrialization, extensive manufacturing bases, and growing automotive sectors. Europe and North America maintain strong positions due to mature downstream industries and stringent quality standards, while the Rest of World region shows emerging growth potential as new mining projects come online.

What does the Regional Analysis of the Talc Market reveal?

In Asia‑Pacific, demand is fueled by China’s expansive plastics and ceramics production and India’s rising pharmaceutical output. Europe’s market is anchored by strict regulatory frameworks that drive demand for high‑purity talc in food and pharma. North America’s growth is linked to the automotive sector’s shift toward lightweight composites and the paints & coatings industry’s need for consistent filler performance. Emerging regions exhibit incremental growth as infrastructure development stimulates construction‑related talc use.

Which companies lead the Talc Market and what are their strategies?

Leading firms include Imerys SA, Minerals Technologies Inc, and Elementis Plc, which focus on global expansion, technology‑driven beneficiation, and diversified product lines. Regional players such as Golcha Minerals Pvt Ltd and Liaoning Aihai Talc Co Ltd concentrate on cost‑competitive supply and local market penetration. Strategic initiatives across the sector involve capacity upgrades, development of specialty grades (e.g., pharmaceutical‑grade talc), and partnerships with downstream manufacturers to secure off‑take agreements.

How does Porter’s Five Forces apply to the Talc Market?

Threat of new entrants is moderate due to high capital requirements and environmental permitting. Bargaining power of suppliers is low because raw talc deposits are abundant, though high‑purity sources are limited. Bargaining power of buyers is moderate; large downstream users can negotiate pricing, but product specifications limit substitution. Threat of substitutes is low, as few minerals match talc’s unique combination of softness and chemical inertness. Industry rivalry is moderate to high, driven by price competition, capacity expansions, and differentiation through specialty grades.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Talc Market?

Strengths: Versatile applications, low cost, and established supply chains. Weaknesses: Sensitivity to regulatory changes and environmental concerns. Opportunities: Development of ultra‑pure grades, nanocomposite technologies, and expansion into emerging economies. Threats: Increasing scrutiny over talc purity in consumer products and potential restrictions on mining activities.

How is the Talc Market Value Chain structured?

The value chain starts with exploration and mining, followed by crushing, grinding, and beneficiation to produce various talc grades. Next comes classification and packaging, after which distribution channels deliver the product to downstream manufacturers in plastics, ceramics, pharma, and other industries. Value‑added services such as custom particle sizing and purity testing enhance differentiation, while logistics and compliance functions ensure timely, regulated delivery.

What key investment insights can be drawn for the Talc Market?

Investors should target companies with diversified grade portfolios and proven capabilities in producing high‑purity talc for regulated sectors. Projects that integrate sustainable mining practices and advanced beneficiation technologies offer long‑term competitive advantages. Geographic diversification, especially into Asia‑Pacific, can capture the fastest‑growing demand. Monitoring regulatory developments is essential to mitigate potential compliance costs.

What conclusions can be drawn from the Talc Market analysis?

The talc market is poised for steady growth, underpinned by expanding end‑use demand and modest but consistent CAGR of 4.43 %. While environmental and regulatory challenges persist, the sector’s ability to innovate high‑purity grades and adopt sustainable practices positions it well for future expansion. Market participants that invest in technology, geographic reach, and niche applications are likely to secure superior returns.

What research methodology was employed for this Talc Market report?

The study combined primary interviews with industry experts, secondary data extraction from company filings, trade publications, and reputable databases, followed by quantitative validation using trend analysis and CAGR calculations. Market sizing employed a top‑down approach anchored on the known 2026 valuation of USD 2.27 billion and projected forward to 2033 using the provided 4.43 % CAGR.

What is the scope of this Talc Market research?

The research covers global talc production, processing, and consumption across all major end‑use industries. It includes segmentation by deposit type (Talc Chlorite, Talc Carbonate) and end‑use sectors, geographic analysis of key regions, competitive profiling of the top ten companies, and strategic assessments such as Porter’s Five Forces, SWOT, and value‑chain mapping. The scope excludes unrelated mineral markets and focuses solely on the talc segment.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Elementis Plc, Golcha Minerals Pvt Ltd, IMI Fabi SpA, Imerys SA, Liaoning Aihai Talc Co Ltd, Minerals Technologies Inc, Nippon Talc Co Ltd, SCR‑Sibelco NV, Sun Minerals Pvt Ltd, and Xilolite SA. Recent developments comprise Imerys’s acquisition of a high‑purity talc facility in North America, Minerals Technologies’ launch of a new ceramic‑grade talc line, and Elementis’s partnership with a leading automotive plastics supplier to develop lightweight composite solutions. These initiatives reflect a market focus on grade specialization and strategic collaboration.