1. Europe Plant Protein Market Overview – Definition, scope, and significance?

The Europe plant protein market encompasses the production, processing, and distribution of protein derived from plant sources such as soy, wheat, and pea. It includes all forms—isolates, concentrates, and protein flours—used across food and beverage applications, including protein beverages, dairy alternatives, meat alternatives, protein bars, and bakery products. This market is significant because it supports the region’s shift toward sustainable, health‑focused diets, reduces reliance on animal‑based proteins, and aligns with EU environmental and nutritional policy goals.

2. Europe Plant Protein Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising consumer awareness of plant‑based nutrition, strict EU regulations promoting lower carbon footprints, and strong demand for functional foods. Restraints arise from price sensitivity to raw material costs and occasional supply chain bottlenecks for pulses. Challenges involve meeting consistent quality standards for isolates and navigating complex labeling regulations. Opportunities are abundant in product innovation—especially in clean‑label isolates—and in expanding into premium segments such as high‑protein bakery and fortified beverages.

3. Europe Plant Protein Market Growth Trends – Current and emerging trends shaping the market?

Current trends feature a surge in “clean label” isolates, increased use of pea protein due to allergen concerns, and the blending of multiple plant proteins to enhance texture and amino‑acid profiles. Emerging trends include the development of high‑protein oat and lentil flours, fortification of traditional bakery items, and the integration of plant protein into ready‑to‑drink (RTD) formats targeting on‑the‑go consumers. Digital traceability and sustainability certifications are also gaining traction among brands.

4. COVID‑19 Impact on the Europe Plant Protein Market – Pandemic effects and recovery trajectory?

The pandemic initially disrupted raw‑material logistics, causing short‑term price volatility for soy and pea. Simultaneously, lockdowns accelerated home‑cooking and health‑conscious purchasing, driving demand for protein‑rich pantry staples. By late 2021, the market rebounded, with a strong recovery in foodservice plant‑protein offerings as restaurants reopened. The overall trajectory remains upward, supported by sustained consumer interest in immunity‑boosting and sustainable nutrition.

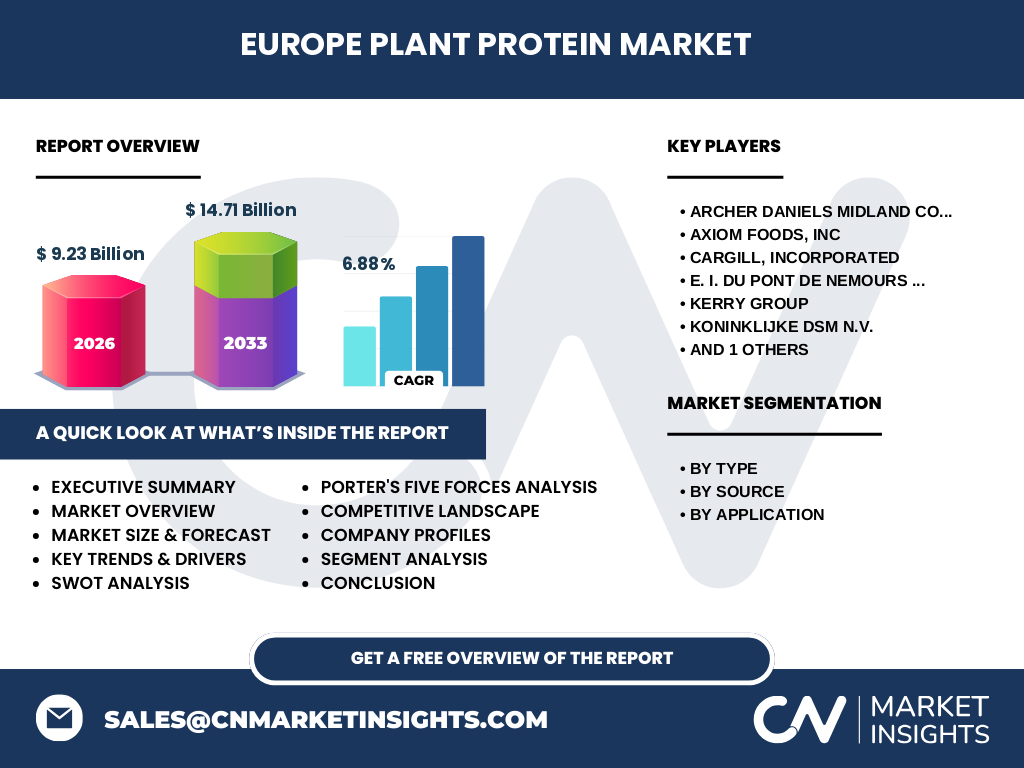

5. Europe Plant Protein Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is led by multinational agribusinesses and specialty ingredient firms. Key players include Archer Daniels Midland Company, Axiom Foods, Inc., Cargill, Incorporated, E.I. Du Pont De Nemours and Company, Kerry Group, Koninklijke DSM N.V., and Roquette Fr. Consolidation has been modest, with strategic joint ventures and acquisition of niche pea‑protein startups to broaden portfolios and accelerate R&D. Partnerships with food manufacturers further strengthen market positioning.

6. Executive Summary – High‑level overview and key findings about Europe Plant Protein Market?

The Europe plant protein market is valued at €9.23 billion in 2026 and is projected to reach €14.71 billion by 2033, reflecting a robust CAGR of 6.88 %. Growth is powered by health‑driven consumer demand, regulatory support for sustainable sourcing, and rapid product innovation across isolates, concentrates, and flours. While price pressure and supply chain resilience remain focal points, opportunities in premium functional foods and clean‑label protein isolates position the market for continued expansion.

7. Europe Plant Protein Market Forecast – Projections for 2025‑2032 period?

Based on the provided CAGR of 6.88 %, the market is expected to maintain steady growth through 2032, surpassing the €14 billion mark before reaching the €14.71 billion forecast for 2033. This trajectory suggests incremental annual increases in both volume and value, driven by expanding applications in dairy‑free beverages, meat‑alternative products, and high‑protein snack categories across the European Union.

8. Europe Plant Protein Market Size and Share by Segmentation – Breakdown by segment?

Segmentation by type divides the market into isolates, concentrates, and protein flour, each serving distinct functional needs. Isolates command premium pricing for high purity, concentrates offer cost‑effective protein enrichment, and protein flour is favored for bakery and cereal applications. By source, soy remains a traditional staple, while wheat and pea proteins are gaining share due to allergen‑free positioning. Application‑wise, dairy alternatives and meat alternatives lead usage, followed by protein beverages, bars, and bakery products.

9. Global Europe Plant Protein Market Size and Share by Region – Geographic distribution?

Within the global context, Europe accounts for a leading share of the plant‑protein landscape, underpinned by strong consumer demand and regulatory encouragement. The region’s market size of €9.23 billion in 2026 represents a significant portion of worldwide plant‑protein revenues, with Western European nations such as Germany, the United Kingdom, and France contributing the bulk of sales, while Central and Eastern European markets show accelerating growth rates.

10. Regional Analysis of the Europe Plant Protein Market – Detailed regional market performance?

Western Europe exhibits the highest per‑capita consumption of plant‑based proteins, driven by mature retail channels and extensive product portfolios. Northern Europe shows rapid adoption of innovative protein beverages and functional snacks. Southern Europe focuses on meat alternatives and dairy‑free desserts, reflecting culinary traditions. Eastern Europe, while currently smaller, demonstrates strong growth potential as cost‑effective concentrates and flours gain market entry.

11. Leading Company Profiles in the Europe Plant Protein Market – Industry players and strategies?

Archer Daniels Midland Company leverages its extensive grain processing network to supply high‑quality soy isolates. Axiom Foods specializes in pea‑protein innovations and partners with snack brands. Cargill emphasizes sustainable sourcing and large‑scale concentrate production. Du Pont focuses on proprietary isolation technology for clean‑label isolates. Kerry Group drives flavor‑enhanced protein blends, while DSM capitalizes on bio‑fortified pea proteins. Roquette Fr offers a broad portfolio of protein flours adapted for bakery applications.

12. Porter's Five Forces Analysis of the Europe Plant Protein Market – Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and stringent EU regulations create barriers, yet niche startups can enter via specialized pea or lentil isolates. Bargaining power of suppliers is moderate, as raw‑material sources like soy are globally traded, but climate impacts can tighten supply. Bargaining power of buyers is high, with large food manufacturers demanding cost‑effective, consistent quality. Threat of substitutes is low, given the unique nutritional profile of plant proteins versus animal alternatives. Industry rivalry is intense, driven by product innovation and brand differentiation.

13. SWOT Analysis of the Europe Plant Protein Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong consumer demand, supportive EU policies, and mature processing infrastructure. Weaknesses: Price sensitivity and occasional raw‑material volatility. Opportunities: Expansion into clean‑label isolates, fortified bakery lines, and high‑protein ready‑to‑drink formats. Threats: Potential regulatory changes on novel foods and supply chain disruptions caused by climate events.

14. Europe Plant Protein Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with agricultural production of soy, wheat, and peas, followed by extraction and processing into isolates, concentrates, or flour. Next, formulation occurs within food‑service and consumer‑goods manufacturers, integrating protein ingredients into final products. Distribution channels include wholesale bulk supply to industrial users and retail packaging for consumer purchase. End‑users span food manufacturers, beverage producers, and bakery firms, each adding value through product development and branding.

15. Key Investment Insights in the Europe Plant Protein Market – Strategic investment recommendations?

Investors should focus on companies that own proprietary isolation technologies and have diversified source portfolios to mitigate raw‑material risk. Funding blended protein blends and clean‑label isolates aligns with consumer trends. Strategic stakes in emerging pea‑protein startups or partnerships with dairy‑alternative brands can accelerate market entry. Additionally, infrastructure investments that enhance supply‑chain resilience for wheat and pea crops will support long‑term growth.

16. Europe Plant Protein Market Conclusion – Summary and key takeaways?

The European plant protein sector is on a clear growth path, underpinned by a 6.88 % CAGR and a projected market size of €14.71 billion by 2033. Health, sustainability, and innovation drive demand across isolates, concentrates, and flours, while soy, wheat, and pea remain the core sources. Competitive dynamics are shaped by major agribusinesses and innovative newcomers, creating a vibrant landscape for investment and product development.

17. Research Methodology – How this research was conducted?

The study combined primary interviews with industry executives, secondary analysis of company reports, trade publications, and EU regulatory documents. Market sizing relied on the provided financial figures, while trend identification used qualitative assessments of consumer behavior, product launches, and supply‑chain developments across the 2026‑2033 horizon.

18. Research Scope – Coverage and limitations?

The scope covers the European Union and associated markets, focusing on plant‑protein types, sources, and applications listed. It excludes animal‑based protein segments and does not quantify individual country‑level market shares beyond the regional overview provided.

19. Key Companies and Recent Developments in the Europe Plant Protein Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Archer Daniels Midland announced a new high‑purity soy isolate plant in Belgium to serve dairy‑free manufacturers. Axiom Foods launched a pea‑protein line tailored for clean‑label snack bars. Cargill entered a joint venture with a Nordic bakery group to develop protein‑enriched breads. Du Pont introduced a patented isolation process reducing water usage by 30 %. Kerry Group secured a partnership with a leading European coffee chain to incorporate protein flour into specialty drinks. DSM released a bio‑fortified pea protein targeting the meat‑alternative market, and Roquette Fr expanded its protein‑flour portfolio with a gluten‑reduced wheat variant for artisan bakeries.