What is the Europe Food Service Packaging Market Overview – Definition, scope, and significance?

The Europe Food Service Packaging Market comprises all packaging solutions used by restaurants, cafes, catering firms, and institutional food services across European countries. It covers primary and secondary packaging made of plastic, metal, flexible, and rigid formats designed for beverages, fruits and vegetables, bakery and confectionery, and dairy products. The market is significant because it underpins food safety, shelf‑life extension, and brand differentiation while aligning with sustainability mandates and consumer expectations for convenience and hygiene.

What are the Europe Food Service Packaging Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising on‑the‑go consumption, expansion of cloud kitchens, and stringent food‑safety regulations that demand reliable barrier properties. Sustainability pressures create opportunities for recyclable and bio‑based materials. Restraints stem from volatile raw‑material costs, especially for petro‑chemical plastics, and the need for substantial capital to upgrade to eco‑friendly lines. Challenges involve navigating diverse regulatory landscapes across EU members and meeting consumer demand for minimal packaging waste. Opportunities arise from digital printing, smart packaging, and circular‑economy business models.

What are the Europe Food Service Packaging Market Growth Trends?

Current trends show a shift toward flexible packaging for its lightweight and reduced carbon footprint, while rigid containers remain essential for dairy and ready‑meal segments. Reusable and returnable packaging schemes are gaining traction in Germany and Scandinavia. Another emerging trend is the integration of QR codes and NFC tags that provide traceability and nutritional information. Additionally, plant‑based plastics are moving from niche to mainstream, driven by retailer commitments to greener portfolios.

How has COVID‑19 impacted the Europe Food Service Packaging Market and what is the recovery trajectory?

The pandemic caused a sharp decline in on‑premise dining, reducing demand for traditional food‑service packaging in 2020. Conversely, take‑away and delivery volumes surged, accelerating adoption of single‑serve flexible packs. Recovery began in late 2021 as restrictions eased, with a compounded annual growth rate of around 5 % as consumers continued to favor contact‑less consumption. The market is now on a rebound path, supported by hybrid dining models that combine dine‑in and delivery services.

Who are the major competitors in the Europe Food Service Packaging Market and what is the level of market consolidation?

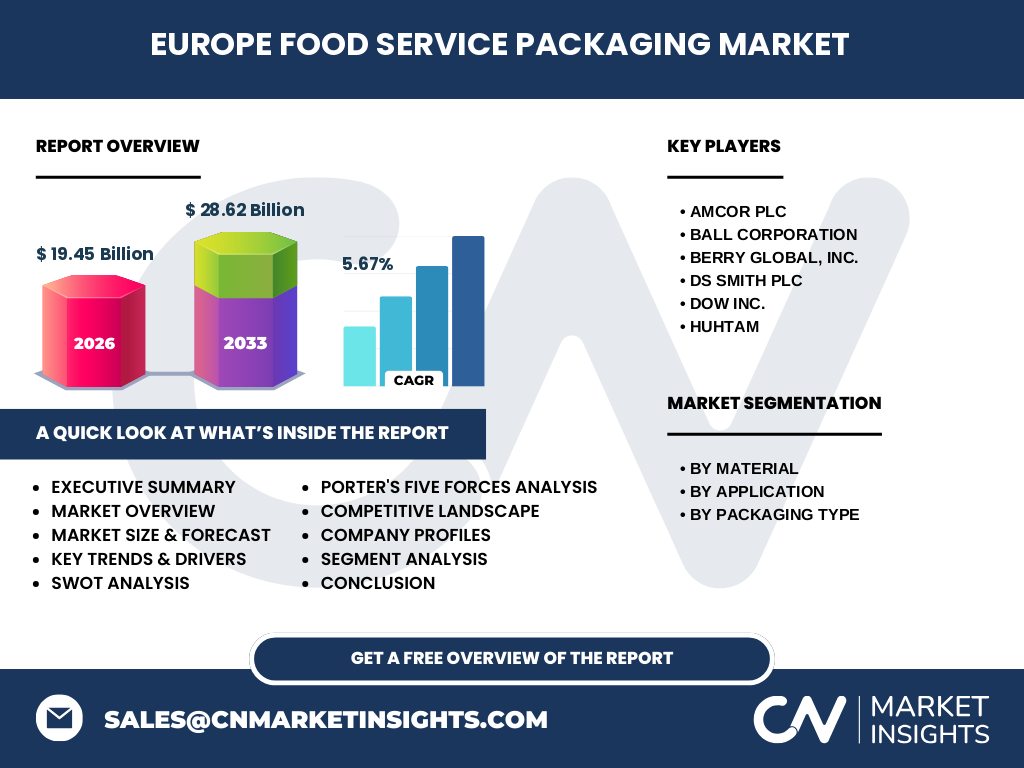

Leading players include Amcor plc, Ball Corporation, Berry Global, Inc., DS Smith PLC, Dow Inc., and Huhtam. These firms dominate through broad material portfolios, extensive distribution networks, and investments in sustainable technologies. The market exhibits moderate consolidation, with several multinational firms acquiring regional specialists to broaden their eco‑friendly product lines. Strategic alliances and joint ventures are common, especially for developing recyclable metal and plastic solutions.

What does the Executive Summary reveal about the Europe Food Service Packaging Market?

The Europe Food Service Packaging Market was valued at €19.45 billion in 2026 and is projected to reach €28.62 billion by 2033, delivering a CAGR of 5.67 %. Growth is propelled by rising demand for flexible, sustainable packaging and the expansion of delivery‑centric food services. Plastic remains the largest material segment, while metal gains share in premium beverage packaging. Key opportunities lie in recyclable systems, digital printing, and smart‑packaging functionalities.

What are the Europe Food Service Packaging Market Forecasts for 2025‑2032?

From 2025 through 2032 the market is expected to expand steadily, maintaining the 5.67 % CAGR derived from the 2026‑2033 projection. By 2032, total market value is anticipated to exceed €27 billion, reflecting continued investment in sustainable packaging, increasing demand for flexible formats, and growth in the European food‑service sector driven by urbanisation and disposable‑income rises.

How is the Europe Food Service Packaging Market sized and shared by segmentation?

By material, the market is split between plastic and metal, with plastic holding the larger portion owing to its versatility across flexible and rigid formats. By application, beverages, fruits and vegetables, bakery and confectionery, and dairy products each command distinct shares; beverages and dairy lead due to high volume use of cans and cartons. By packaging type, flexible packaging captures a growing share thanks to its lightweight nature, while rigid packaging remains crucial for structural integrity in dairy and bakery items.

What is the global Europe Food Service Packaging Market size and share by region?

Europe accounts for a substantial portion of the global food‑service packaging landscape, with the region’s €19.45 billion valuation in 2026 representing a key share of worldwide demand. While specific percentages for other regions are not disclosed, Europe’s market is recognised as a leading hub for innovation in sustainable packaging, influencing global trends and standards.

What does the Regional Analysis of the Europe Food Service Packaging Market reveal?

Western Europe, particularly Germany, France, and the UK, drives the majority of market value through mature food‑service sectors and strong sustainability regulations. Northern Europe shows the highest adoption of reusable and recyclable packaging, supported by governmental incentives. Southern and Eastern European markets display faster growth rates as urban catering expands and consumer awareness of packaging waste rises.

What are the leading company profiles and strategies in the Europe Food Service Packaging Market?

Amcor plc focuses on circular‑economy solutions, investing in recyclable rigid containers and flexible films. Ball Corporation leverages its metal expertise to supply aluminium cans for premium beverages. Berry Global, Inc. expands its flexible‑pack portfolio with bio‑based polymers. DS Smith PLC emphasizes paper‑based packaging and closed‑loop recycling. Dow Inc. drives innovation in high‑performance plastics, while Huhtam concentrates on sustainable paper and flexible packaging for food‑service applications.

How does Porter’s Five Forces assess the Europe Food Service Packaging Market?

Competitive rivalry is high due to the presence of several multinational firms and price sensitivity. Threat of new entrants is moderate; capital intensity and regulatory compliance create barriers, yet niche sustainable innovators can enter. Bargaining power of suppliers is moderate, as raw‑material markets for plastics and metals are volatile. Buyers—large food‑service chains—exercise strong bargaining power, demanding cost‑effective, eco‑friendly solutions. The threat of substitutes remains low, given the specialised performance requirements of food‑service packaging.

What is the SWOT analysis of the Europe Food Service Packaging Market?

Strengths: Established supply chains, strong R&D capabilities, and regulatory support for sustainable packaging.

Weaknesses: Dependence on volatile petro‑chemical prices and fragmented regulatory environments.

Opportunities: Growth of reusable systems, digital and smart packaging, and demand for bio‑based materials.

Threats: Stringent EU waste‑reduction directives, rising raw‑material costs, and shifting consumer preferences toward minimal packaging.

What does the Europe Food Service Packaging Market value‑chain analysis show?

The value chain begins with raw‑material extraction (petro‑chemicals, metal ores, paper pulp) followed by polymerisation or metal forming. Next are conversion processes—film extrusion, molding, and printing—where manufacturers add branding and functional features. Distribution channels include wholesale distributors, direct sales to food‑service operators, and e‑commerce platforms. End‑users—restaurants, catering firms, and institutional cafeterias—provide feedback that drives innovation in the upstream stages.

What key investment insights can be drawn for the Europe Food Service Packaging Market?

Investors should target companies with clear sustainability roadmaps, especially those expanding recyclable plastic and metal lines. Funding opportunities exist in digital printing technologies and smart‑packaging integration that enhance traceability. Joint ventures with waste‑management firms can unlock circular‑economy revenue streams. Geographic focus on Western and Northern Europe offers stable returns, while Southern and Eastern markets present higher growth potential.

What is the concluding summary of the Europe Food Service Packaging Market?

The Europe Food Service Packaging Market is on a robust growth trajectory, moving from €19.45 billion in 2026 to €28.62 billion by 2033, underpinned by a 5.67 % CAGR. Flexibility, sustainability, and technology are the core themes reshaping the sector. Leading firms are consolidating capabilities to meet stricter environmental regulations and evolving consumer expectations, creating a compelling landscape for strategic investment.

How was the research methodology designed for this report?

The study combined primary interviews with industry executives, secondary data from company filings, trade associations, and EU regulatory publications. Market sizing employed a top‑down approach using known 2026 valuation and applying the disclosed CAGR to forecast future values. Segmentation analysis integrated material, application, and packaging‑type data provided by the key companies.

What is the scope of the research, including coverage and limitations?

The research covers the entire European food‑service packaging sector, encompassing plastic and metal materials across flexible and rigid formats for four main applications. Geographic scope includes all EU and non‑EU European countries. Limitations arise from the unavailability of granular market‑share percentages by country and the reliance on publicly disclosed financial figures.

Which key companies have recent developments in the Europe Food Service Packaging Market?

Amcor plc announced a new recyclable rigid container line for dairy products in Germany. Ball Corporation launched an aluminium can series with reduced carbon intensity for premium beverages in France. Berry Global, Inc. introduced a bio‑based flexible film for bakery items across Scandinavia. DS Smith PLC entered a partnership with a UK waste‑management firm to pilot a closed‑loop paper‑packaging system. Dow Inc. unveiled a high‑performance, low‑weight polymer for take‑away meals, and Huhtam released a compostable paper tray for the Mediterranean catering market.