What is the Nuclear Decommissioning Services Market Overview – Definition, scope, and significance?

The Nuclear Decommissioning Services Market comprises all activities required to retire nuclear facilities safely, including planning, dismantling, waste management, site remediation, and long‑term monitoring. The scope covers commercial power reactors, research reactors, and prototype installations across all capacity ranges—from below 100 MW to installations above 1 000 MW. Its significance lies in ensuring environmental protection, public safety, and regulatory compliance while unlocking value from legacy assets. As governments worldwide implement stricter nuclear phase‑out policies, the market provides critical expertise to manage high‑cost, technically complex projects that can span decades.

What are the key drivers, restraints, challenges, and opportunities in the Nuclear Decommissioning Services Market?

Key drivers include aging reactor fleets, heightened regulatory scrutiny, and increasing public demand for safe waste disposal. Mandatory decommissioning schedules in Europe, North America, and parts of Asia create a predictable pipeline of projects. Restraints stem from the enormous capital intensity and lengthy timelines, which can deter investment. Challenges involve limited availability of skilled deconstruction personnel, complex radiation safety requirements, and fluctuating policy environments. Opportunities arise from technological advances such as remote‑operated dismantling robots, modular waste processing units, and the emergence of “greenfield” decommissioning contracts that bundle services for faster execution.

What are the current growth trends shaping the Nuclear Decommissioning Services Market?

Current trends emphasize a shift toward immediate dismantling strategies driven by tighter deadlines, while some operators still favor deferred dismantling to spread costs. Digital twins and predictive analytics are increasingly adopted to optimize decommissioning schedules and reduce unforeseen delays. Collaborative consortia among engineering firms, waste processors, and technology providers are emerging to share risk and pool expertise. Additionally, the market is seeing a rise in “service‑as‑a‑platform” models that combine consultancy, execution, and post‑closure monitoring under a single contract.

How has COVID‑19 impacted the Nuclear Decommissioning Services Market, and what is the recovery trajectory?

The pandemic caused temporary project pauses due to lockdowns, supply‑chain disruptions, and workforce constraints, leading to schedule slippages of 3‑6 months on average. However, the essential nature of nuclear safety ensured that most contracts remained in force. Post‑2022, the market has entered a recovery phase, with projects resuming at a pace that aligns with pre‑pandemic levels. The renewed focus on energy security and climate goals is further accelerating decommissioning activities, supporting a robust rebound.

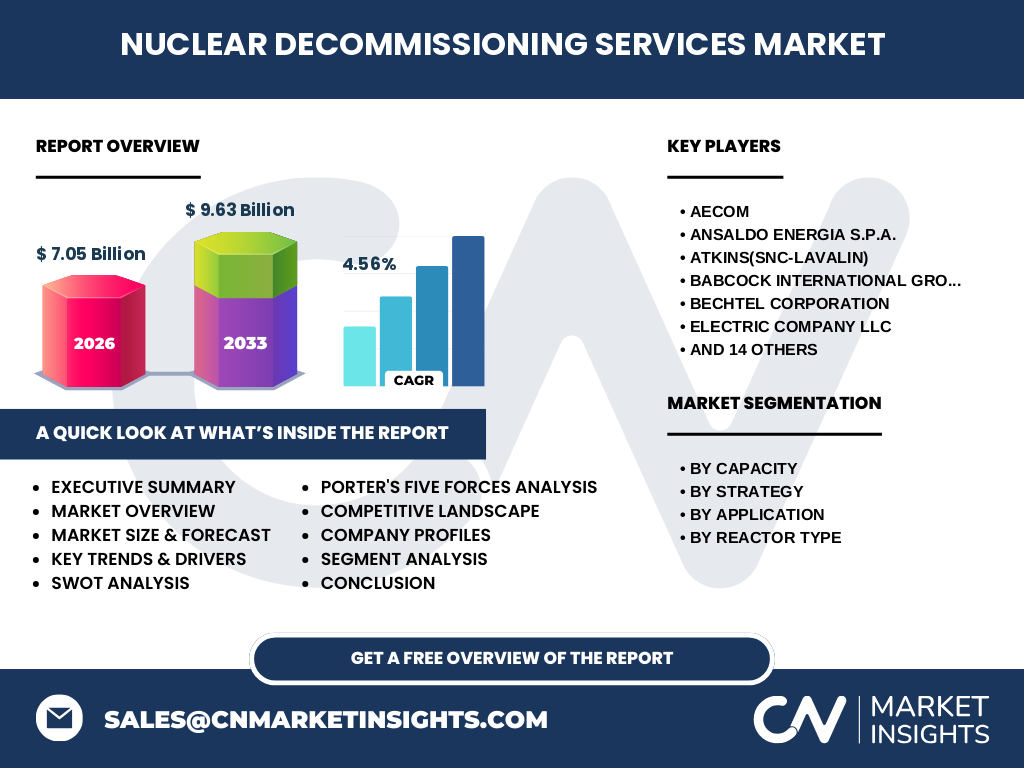

Who are the major competitors and what is the competitive landscape in the Nuclear Decommissioning Services Market?

The market is highly consolidated around a few global engineering and construction giants with deep nuclear expertise. Leading competitors include AECOM, Bechtel Corporation, Fluor Corporation, Westinghouse, and GEHitachi Nuclear Energy. European specialists such as Orano, Studsvik AB, and Nuklear‑Service mbH also hold strong positions. Recent consolidation trends involve strategic acquisitions to broaden service portfolios, such as larger firms acquiring niche waste‑management companies to offer end‑to‑end solutions.

What are the high‑level findings in the Executive Summary of the Nuclear Decommissioning Services Market?

The market is valued at $7.05 billion in 2026 and is projected to reach $9.63 billion by 2033, reflecting a 4.56 % CAGR. Growth is propelled by aging reactor inventories, stricter decommissioning mandates, and innovations in remote dismantling. Regional demand is strongest in Europe and North America, with emerging opportunities in Asia‑Pacific as several reactors approach end‑of‑life. Competitive dynamics favor firms that can integrate engineering, waste handling, and long‑term monitoring under unified contracts.

What are the forecast expectations for the Nuclear Decommissioning Services Market from 2025 to 2032?

Based on the projected CAGR of 4.56 %, the market is expected to expand steadily each year, crossing the $9 billion threshold by 2030 and reaching the $9.63 billion mark by 2033. The forecast reflects continued decommissioning of reactors in the 100‑1 000 MW range, increased adoption of immediate dismantling, and heightened spending on waste management and site remediation.

How is the Nuclear Decommissioning Services Market sized and shared by segmentation?

By capacity, projects are divided into Below 100 MW, 100‑1 000 MW, and Above 1 000 MW. By strategy, the market includes Immediate Dismantling, Deferred Dismantling, and Entombment. Application segments consist of Commercial Power Reactor, Research Power Reactor, and Prototype. Finally, reactor type segmentation covers Pressurized Water Reactor, Boiling Water Reactor, and Gas Cooled Reactor. Each segment presents distinct technical requirements and budgetary profiles, influencing contractor selection and service bundling.

What is the global Nuclear Decommissioning Services Market size and share by region?

The market’s global footprint is driven primarily by Europe and North America, where the majority of nuclear plants are reaching end‑of‑life. Asia‑Pacific contributes a growing share as countries like Japan and South Korea plan systematic phase‑outs. While exact regional monetary figures are not disclosed, the geographical distribution aligns with the concentration of aging reactors and regulatory frameworks that mandate decommissioning.

What does the regional analysis reveal about Nuclear Decommissioning Services market performance?

In Europe, stringent EU directives and substantial legacy capacity generate a steady pipeline of large‑scale contracts, especially for reactors above 1 000 MW. North America shows strong demand for immediate dismantling of commercial reactors, with an increasing focus on waste disposition. Asia‑Pacific, led by Japan’s post‑Fukushima policy, is transitioning toward deferred dismantling for certain units, creating opportunities for phased service models. Emerging markets in the Middle East and Latin America are still nascent but may contribute incremental demand as new nuclear programs consider end‑of‑life planning.

Which companies lead the Nuclear Decommissioning Services Market and what are their strategies?

Key players include AECOM, Bechtel, Fluor, Westinghouse, GEHitachi Nuclear Energy, Orano, Studsvik AB, and Nuklear‑Service mbH. Their strategies focus on expanding service breadth through acquisitions, investing in robotics and AI for safer dismantling, and forming joint ventures with waste‑treatment specialists. Many are also pursuing long‑term service contracts that encompass post‑shutdown monitoring, positioning themselves as one‑stop providers.

How does Porter’s Five Forces framework assess the Nuclear Decommissioning Services Market?

Threat of new entrants is low due to high capital requirements, specialized expertise, and regulatory barriers. Bargaining power of suppliers is moderate; while equipment manufacturers are few, large firms can negotiate favorable terms. Bargaining power of buyers (utility owners and governments) is high because decommissioning budgets are scrutinized, prompting competitive tendering. Threat of substitutes is minimal, as no alternative to professional decommissioning exists. Industry rivalry is intense, driven by a limited number of qualified firms competing for sizable contracts.

What are the SWOT insights for the Nuclear Decommissioning Services Market?

Strengths: Established technical expertise, long‑term contractual relationships, and high entry barriers.

Weaknesses: Capital‑intensive projects, limited talent pool, and dependency on regulatory timelines.

Opportunities: Adoption of advanced robotics, growth in emerging markets, and integrated waste‑to‑energy solutions.

Threats: Policy shifts, fluctuating waste disposal costs, and potential public opposition to nuclear activities.

What does the value chain of the Nuclear Decommissioning Services Market look like?

The value chain begins with Regulatory Planning, followed by Engineering Design, Site Characterization, Dismantling Execution, Radioactive Waste Segregation, Transportation & Disposal, and ends with Site Restoration and Long‑Term Monitoring. Supporting activities include Project Financing, Supply Chain Management, and Health‑Safety Assurance. Integration across these stages provides competitive advantage.

What key investment insights can be drawn for stakeholders in the Nuclear Decommissioning Services Market?

Investors should target firms with diversified service portfolios and proven execution on large‑scale projects, as they are better positioned to win multi‑year contracts. Capital allocation toward companies developing remote‑handling robotics and digital twins offers upside potential. Strategic partnerships with waste‑processing specialists can mitigate exposure to regulatory changes. Finally, monitoring policy developments in Europe and Asia‑Pacific will help identify upcoming project windows.

What conclusions can be drawn from the Nuclear Decommissioning Services Market analysis?

The market is on a steady growth trajectory, underpinned by aging reactor inventories and evolving regulatory frameworks. While capital intensity and skill shortages pose challenges, technological innovation and integrated service models create pathways for value creation. Companies that can combine engineering excellence with advanced waste‑management capabilities are poised to capture the expanding contract pool.

How was the research for this Nuclear Decommissioning Services Market report conducted?

The study employed a mixed‑method approach, combining secondary data from industry reports, regulatory filings, and company disclosures with primary insights from expert interviews across engineering, waste management, and nuclear regulatory bodies. Data triangulation ensured consistency, while trend analysis leveraged historical decommissioning schedules to derive the forecasted CAGR.

What is the scope of the Nuclear Decommissioning Services Market research?

The scope covers global decommissioning activities for commercial, research, and prototype reactors across all capacity brackets and dismantling strategies. It includes analysis of engineering services, waste handling, site remediation, and post‑closure monitoring, but excludes upstream nuclear fuel production and downstream power generation activities.

Which key companies and recent developments are notable in the Nuclear Decommissioning Services Market?

Notable companies include AECOM, Bechtel, Fluor, Westinghouse, GEHitachi Nuclear Energy, Orano, Studsvik AB, and Nuklear‑Service mbH. Recent developments feature AECOM’s launch of a robotic decontamination platform, Bechtel’s acquisition of a specialized radioactive waste processor, and Orano’s partnership with a European consortium to standardize entombment procedures for legacy sites. These moves illustrate a trend toward technology‑driven service expansion and collaborative risk sharing.