What is the IP Camera Market Overview – definition, scope, and significance?

The IP Camera Market comprises network‑enabled video surveillance devices that transmit digital footage over internet protocols for monitoring, recording, and analytics. Its scope includes hardware components (sensors, lenses, processors) and related services (cloud storage, installation, maintenance). Significance lies in enhancing security across residential, commercial, and government sectors, driving smart‑city initiatives, and enabling advanced analytics such as facial recognition and behavior detection.

What are the main drivers, restraints, challenges, and opportunities in the IP Camera Market?

Key drivers include growing demand for remote monitoring, declining hardware costs, and increased adoption of AI‑powered video analytics. Restraints stem from privacy‑related regulations and concerns over data security. Challenges involve integration complexity with legacy systems and the need for high‑bandwidth connectivity. Opportunities arise from expanding 5G networks, edge‑computing capabilities, and rising investments in smart‑home and smart‑city projects that require scalable, high‑resolution camera deployments.

Which growth trends are currently shaping the IP Camera Market?

Current trends feature a shift toward higher resolution (4K and beyond) cameras, the proliferation of pan‑tilt‑zoom (PTZ) units for flexible monitoring, and greater use of infrared sensors for low‑light environments. AI‑enabled analytics—such as object detection, people counting, and loitering alerts—are becoming standard. Additionally, cloud‑based service models are gaining traction, reducing upfront capital expenditure for end‑users.

How did COVID‑19 impact the IP Camera Market and what is the recovery trajectory?

The pandemic accelerated demand for remote surveillance as businesses sought to monitor facilities with limited on‑site staff. Supply‑chain disruptions temporarily slowed hardware shipments, but the surge in digital transformation offset the slowdown. Post‑2020, the market rebounded strongly, with continued growth fueled by heightened security awareness and the expansion of contact‑less monitoring solutions.

What does the competitive landscape of the IP Camera Market look like?

The market is highly competitive, featuring a mix of established multinational firms and fast‑growing regional players. Consolidation is evident through strategic acquisitions and partnerships aimed at broadening product portfolios and enhancing AI capabilities. Companies compete on image quality, software ecosystems, and service offerings, while also pursuing vertical integration to control component supply and reduce costs.

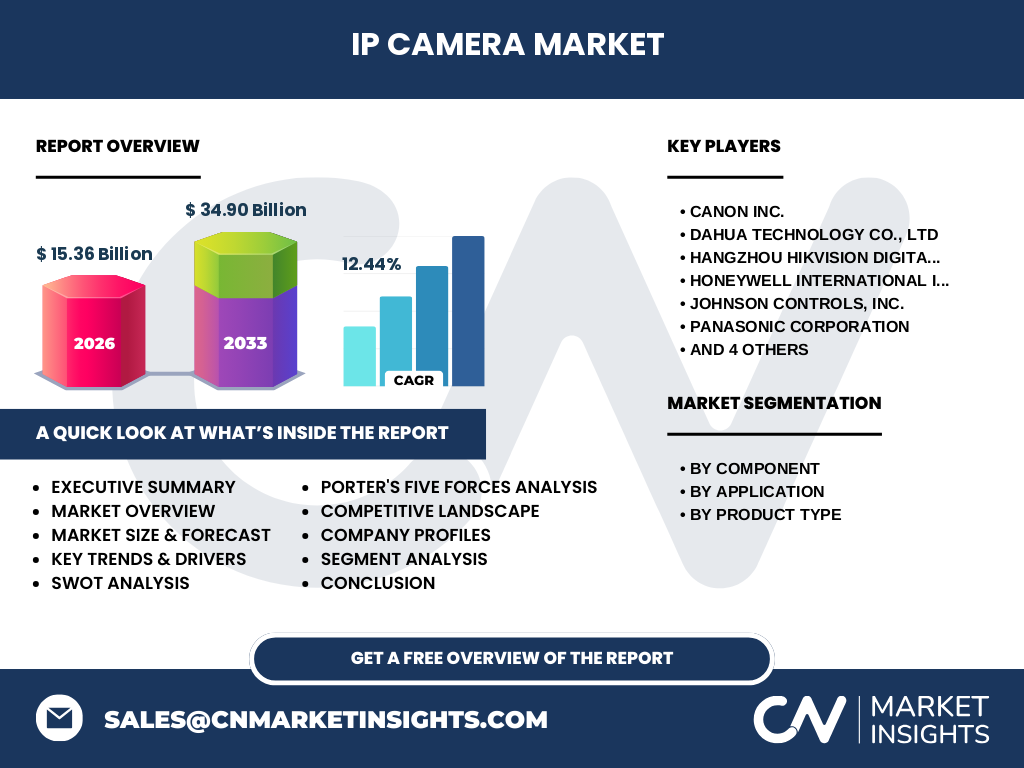

What are the key findings highlighted in the Executive Summary?

The IP Camera Market is projected to reach 34.90 billion by 2033, growing at a CAGR of 12.44 % from 2027 to 2033. The 2026 market size stands at 15.36 billion. Growth is driven by AI analytics, rising smart‑city investments, and expanding cloud services. Hardware remains the dominant component, while services are gaining share due to subscription‑based models. Regional demand is strongest in North America, Europe, and Asia‑Pacific.

What are the forecast expectations for the IP Camera Market from 2025 to 2032?

Based on the provided CAGR of 12.44 %, the market is expected to more than double its 2026 value by 2033, reaching 34.90 billion. The forecast indicates steady year‑over‑year expansion, with accelerated growth in segments featuring AI‑driven analytics and edge‑computing. Investment in next‑generation hardware, particularly PTZ and infrared models, will support the upward trajectory.

How is the IP Camera Market sized and shared by segment?

Segmentation is defined by component, application, and product type. By component, hardware accounts for the majority of revenue, while services capture a growing portion through maintenance contracts and cloud storage. Application‑wise, commercial deployments lead, followed by residential and government installations. Product‑type distribution shows fixed cameras as the base, PTZ units gaining market share due to their flexibility, and infrared cameras growing in low‑light sectors.

What is the global IP Camera Market size and share by region?

The market exhibits a balanced geographic spread. North America and Europe together hold a significant portion of the 2026 market value, driven by early adoption of smart‑city projects and stringent security regulations. Asia‑Pacific shows the fastest growth rate, propelled by large‑scale infrastructure development and expanding consumer smart‑home adoption. The combined regional markets support the overall 2026 size of 15.36 billion.

What does the regional analysis of the IP Camera Market reveal?

North America leads in high‑value service contracts and AI integration, while Europe emphasizes compliance with data‑privacy standards, influencing product design. Asia‑Pacific benefits from cost‑effective manufacturing and rapid urbanization, resulting in strong demand for both residential and commercial solutions. Emerging markets in Latin America and the Middle East are beginning to invest in surveillance infrastructure, indicating future growth opportunities.

Which companies are the leading players in the IP Camera Market and what are their strategies?

Key companies include Canon Inc., Dahua Technology, Hikvision, Honeywell International, Johnson Controls, Panasonic, Pelco, Robert Bosch GmbH, Sony Corporation, and Z3 Technology. Strategies focus on expanding AI analytics, forging cloud service partnerships, investing in R&D for higher‑resolution sensors, and pursuing acquisitions to broaden market reach. Many are also enhancing after‑sales service networks to capture the growing services segment.

How does Porter’s Five Forces analysis apply to the IP Camera Market?

Threat of new entrants is moderate due to high R&D costs and brand loyalty. Supplier power is moderate; component suppliers (image sensors, lenses) are few but diversified through vertical integration. Buyer power is strong as end‑users demand advanced features at competitive prices. Rivalry among existing firms is intense, driven by rapid innovation cycles. Substitutes are limited, mainly traditional analog cameras, which are losing relevance.

What are the SWOT insights for the IP Camera Market?

Strengths: High scalability, integration with IoT, and robust AI analytics.

Weaknesses: Data‑privacy concerns and dependence on high‑speed connectivity.

Opportunities: Expansion of 5G, edge‑AI processing, and growth in smart‑city funding.

Threats: Regulatory restrictions on surveillance and potential cybersecurity breaches.

What does the value chain of the IP Camera Market look like?

The value chain begins with raw material suppliers (optics, semiconductors), proceeds to component manufacturers (image sensors, processors), then to system integrators assembling hardware and embedding firmware. Software developers add analytics platforms, followed by distribution channels (OEMs, VARs). After‑sales services—installation, maintenance, cloud storage—complete the chain, creating recurring revenue streams.

What key investment insights can be drawn for the IP Camera Market?

Investors should target companies with strong AI‑analytics portfolios and scalable cloud services, as these segments promise higher margins. Funding firms that own critical component supply lines can mitigate supplier risk. Emerging markets in Asia‑Pacific present growth upside, while firms addressing data‑privacy compliance may capture premium enterprise contracts.

What are the concluding takeaways from the IP Camera Market analysis?

The IP Camera Market is on a rapid expansion path, slated to more than double by 2033. AI‑enabled hardware and service‑based revenue models are the primary growth engines. While regulatory and cybersecurity challenges persist, the rollout of 5G and edge computing offers substantial opportunity. Companies that innovate across hardware, software, and services are best positioned to capture market share.

How was the research methodology designed for this report?

The study combined primary interviews with industry experts, secondary data from reputable market databases, and financial statements of key players. Trend analysis employed CAGR calculations based on the provided 2026 market size (15.36 billion) and forecast (34.90 billion). Segmentation was validated through cross‑referencing product catalogs and service offerings.

What is the scope of the research and its limitations?

The research covers global IP camera hardware, services, applications (residential, commercial, government), and product types (fixed, PTZ, infrared). Geographic coverage includes all major regions, with a focus on North America, Europe, and Asia‑Pacific. Limitations stem from the reliance on publicly available data and the exclusion of confidential financial details beyond the provided market size and CAGR.

Which key companies have made recent developments in the IP Camera Market?

Recent developments include Canon’s launch of AI‑enhanced 4K fixed cameras, Hikvision’s expansion of edge‑AI processors, and Honeywell’s partnership with cloud‑service providers for integrated surveillance platforms. Panasonic introduced a new infrared line optimized for low‑light environments, while Sony unveiled a PTZ model with advanced autofocus technology. Z3 Technology announced a strategic acquisition to strengthen its services portfolio.