What is the Asia Pacific Breast Cancer Screening Market Overview - Definition, scope, and significance?

The Asia Pacific Breast Cancer Screening Market encompasses all products, services, and technologies used to detect breast cancer at an early stage across the Asia‑Pacific region. This includes imaging modalities (such as mammography, ultrasound, and MRI), blood‑marker assays, genetic testing, and immunohistochemistry solutions, as well as the facilities that deliver these services—hospitals, diagnostic centres, cancer institutes, and research laboratories. The market’s significance stems from the rising incidence of breast cancer in the region, growing awareness of early detection benefits, and increasing government and private‑sector investment in preventive health programmes. Early screening improves survival rates, reduces treatment costs, and aligns with broader public‑health goals of lowering cancer‑related morbidity.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Breast Cancer Screening Market?

Key drivers include a rapidly expanding middle‑class population with higher health‑care spending, supportive government policies promoting cancer‑screening programs, and technological advances that improve test accuracy and patient comfort. Restraints arise from uneven health‑care infrastructure, especially in low‑income rural areas, and high capital costs for advanced imaging equipment. Challenges involve shortage of trained radiologists, cultural stigma surrounding breast examinations, and reimbursement variability across countries. Opportunities are evident in the growing adoption of minimally invasive blood‑marker and genetic tests, partnerships between multinational manufacturers and local providers, and the rollout of mobile screening units targeting underserved communities.

What are the current growth trends in the Asia Pacific Breast Cancer Screening Market?

Current trends show a shift from traditional film‑based mammography to digital and tomosynthesis platforms, driven by higher resolution and lower radiation dose. There is also an accelerating interest in liquid‑biopsy blood‑marker tests, which enable earlier detection with minimal discomfort. Integration of artificial intelligence (AI) for image analysis is gaining traction, helping to compensate for radiologist shortages and improve diagnostic consistency. Additionally, multi‑modal screening programmes that combine imaging with genetic risk profiling are emerging in high‑income economies such as Japan, South Korea, and Australia.

How has COVID‑19 impacted the Asia Pacific Breast Cancer Screening Market, and what is the recovery trajectory?

The pandemic caused a temporary decline in routine screening volumes as lockdowns limited access to hospitals and diagnostic centres. Delayed appointments and patient apprehension reduced market activity in 2020‑21. However, the sector demonstrated resilience; tele‑health triage tools and mobile screening vans helped restore service levels. By 2022, demand rebounded strongly, driven by a backlog of postponed scans and heightened awareness of health‑screening importance. The recovery path is expected to continue upward, with a steady increase in screening throughput as confidence returns and health‑care systems expand capacity.

Who are the major competitors in the Asia Pacific Breast Cancer Screening Market and how is the market consolidating?

The competitive landscape is anchored by multinational equipment and diagnostics leaders such as Becton, Dickinson and Company, Danaher Corporation, General Electric Company, Hologic, Inc., Koninklijke Philips N.V., Siemens Healthcare AG, and specialty genetics firms like Myriad Genetics, Inc. and Exact Sciences Corporation. Emerging niche players include OncoCyte Corporation, POC Medical Systems, and regional manufacturers. Consolidation is evident through strategic acquisitions—e.g., larger firms acquiring AI‑focused start‑ups—to broaden product portfolios and strengthen distribution networks across the diverse Asia‑Pacific markets.

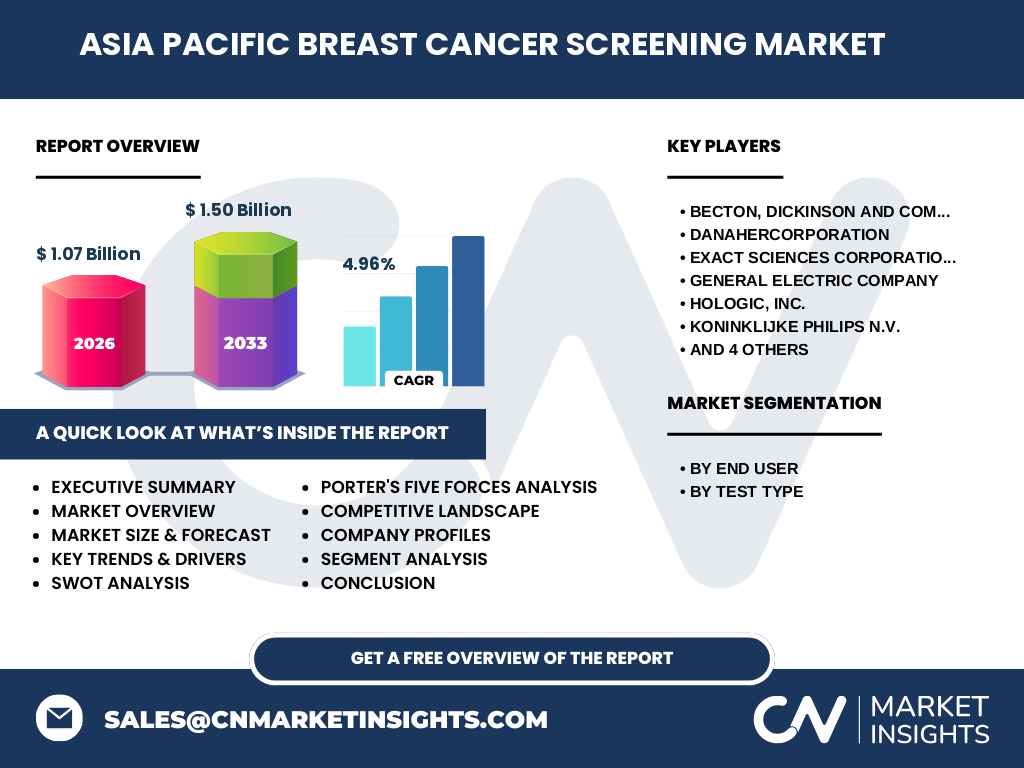

What are the high‑level findings in the Executive Summary of the Asia Pacific Breast Cancer Screening Market?

The market was valued at US 1.07 billion in 2026 and is projected to reach US 1.50 billion by 2033, reflecting a CAGR of 4.96 % over the forecast horizon. Growth is propelled by expanding health‑care infrastructure, rising breast‑cancer incidence, and adoption of advanced screening technologies. Imaging tests remain the largest segment, while blood‑marker and genetic tests show the fastest growth rates. Hospitals dominate the end‑user mix, but diagnostic centres are gaining share due to their agility and lower cost structures. Competitive dynamics are intensifying, with major players investing in AI and partnership models to capture market share.

What are the forecast expectations for the Asia Pacific Breast Cancer Screening Market from 2025‑2032?

Based on the given CAGR of 4.96 %, the market is expected to maintain a steady upward trajectory, growing from the 2026 base of US 1.07 billion to approximately US 1.50 billion by 2033. The forecast reflects continued demand for both imaging and emerging molecular tests, incremental penetration of AI‑enabled diagnostics, and expanding public‑health screening initiatives across the region. Growth is anticipated to be broad‑based, with all major sub‑segments contributing positively to the overall market expansion.

How is the market sized and shared by segmentation (End User and Test Type)?

Segmentation by end user shows hospitals as the primary channel, supported by diagnostic centres, cancer institutes, and research laboratories. In terms of test type, imaging tests command the largest share due to their established role in detection, followed by blood‑marker tests, genetic tests, and immunohistochemistry. While exact numerical shares are not disclosed, the hierarchy reflects current utilization patterns, with imaging leading and molecular diagnostics gaining momentum as complementary tools.

What is the geographic distribution of the Asia Pacific Breast Cancer Screening Market?

The market spans the entire Asia‑Pacific region, encompassing mature economies such as Japan, Australia, and South Korea, as well as fast‑growing markets like China, India, and Southeast Asian nations. Each geography contributes to the aggregate market size of US 1.07 billion in 2026, with higher per‑capita screening intensity observed in Japan and Australia, and rapid expansion potential in China and India driven by large populations and increasing health‑care budgets.

What does the regional analysis reveal about market performance across the Asia Pacific?

Japan leads in technology adoption, with widespread digital mammography and AI integration. Australia shows strong public‑funded screening programs and high compliance rates. South Korea’s market is characterized by early‑stage adoption of genetic testing. China and India present the largest absolute volume potential, though current penetration is modest; government initiatives aimed at expanding rural screening are expected to accelerate growth. Southeast Asian markets such as Singapore and Malaysia are adopting hybrid models that combine imaging with emerging blood‑marker assays.

Which companies are leading in the Asia Pacific Breast Cancer Screening Market and what are their strategies?

Key players include Becton, Dickinson and Company (expanding point‑of‑care blood‑marker platforms), Danaher Corporation (leveraging its broad diagnostic portfolio and AI analytics), Exact Sciences Corporation (promoting colorectal‑cancer‑linked biomarker panels that can be cross‑applied to breast‑cancer screening), General Electric Company (enhancing digital imaging hardware), Hologic, Inc. (focused on 3‑D mammography and AI), Koninklijke Philips N.V. (integrated imaging‑AI suites), Myriad Genetics, Inc. (genetic test leadership), OncoCyte Corporation (liquid‑biopsy innovations), POC Medical Systems (portable imaging devices), and Siemens Healthcare AG (advanced MRI and AI solutions). Strategies revolve around product innovation, strategic partnerships with local health networks, and expanding service‑based models such as managed‑screening programs.

How does Porter’s Five Forces analysis apply to the Asia Pacific Breast Cancer Screening Market?

Threat of new entrants is moderate; high capital costs and regulatory barriers deter newcomers, yet niche biotech firms can enter via molecular test niches. Bargaining power of buyers is growing as hospitals and diagnostic chains consolidate, seeking volume discounts. Bargaining power of suppliers is limited for imaging equipment due to few large manufacturers, but higher for consumables and reagents where multiple vendors exist. Threat of substitutes is low; alternative diagnostics do not match the clinical efficacy of established screening tests. Industry rivalry is intense, with major multinational firms competing on technology, price, and service contracts.

What are the SWOT insights for the Asia Pacific Breast Cancer Screening Market?

Strengths: strong demand driven by cancer incidence, diversified technology base, and supportive policy environment. Weaknesses: uneven access in rural areas, high equipment cost, and skill shortages. Opportunities: adoption of AI, expansion of liquid‑biopsy and genetic panels, and public‑private partnership models. Threats: potential regulatory tightening, economic downturns affecting health‑care budgets, and competitive pressure from emerging low‑cost manufacturers.

What does the value‑chain analysis reveal about the Asia Pacific Breast Cancer Screening Market?

The value chain starts with R&D and component manufacturing (sensors, reagents), followed by equipment assembly by OEMs, distribution through regional wholesalers, and integration into health‑care facilities. After installation, service and maintenance contracts, consumables supply, and data‑analytics platforms add recurring revenue. End‑users—hospitals, diagnostic centres, cancer institutes, and research labs—generate the final value through screening services, reporting, and follow‑up care. Digital platforms and AI services increasingly reside between equipment and end‑user, creating new value‑add layers.

What key investment insights can be drawn for stakeholders in the Asia Pacific Breast Cancer Screening Market?

Investors should prioritize companies with strong AI and digital health capabilities, as these are likely to capture premium market share. Funding mobile‑screening initiatives and partnerships with government cancer‑control programs offers scalable growth in underserved regions. Acquiring or partnering with niche biotech firms developing blood‑marker or genetic tests can diversify product portfolios and address emerging demand for less invasive screening. Lastly, investing in training and service networks can mitigate talent shortages and improve customer stickiness.

What are the concluding takeaways from the Asia Pacific Breast Cancer Screening Market analysis?

The market is on a robust growth path, moving from a US 1.07 billion base in 2026 toward US 1.50 billion by 2033, driven by demographic shifts, technology adoption, and policy support. Imaging remains the core, yet molecular diagnostics and AI are reshaping the value proposition. Competitive pressures are high, prompting consolidation and innovation. Stakeholders who align with emerging trends—AI‑enabled imaging, liquid‑biopsy, and integrated screening programmes—will be best positioned to benefit.

What research methodology underpins this market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, health‑care administrators, and key opinion leaders across the Asia‑Pacific region, with secondary data from company filings, regulatory bodies, and reputable industry databases. Quantitative projections were derived using a compound annual growth rate (CAGR) of 4.96 % applied to the known 2026 market size of US 1.07 billion, extending through 2033. Qualitative insights were triangulated across multiple sources to ensure reliability.

What is the scope of this research and its limitations?

The scope covers the full range of breast‑cancer screening technologies and end‑user segments within the Asia‑Pacific geography, focusing on market size, growth trends, competitive dynamics, and strategic outlook up to 2033. Limitations include reliance on publicly disclosed financials and market estimates, which may not capture undisclosed private‑company data. Regional granularity is addressed at a high level; country‑specific nuances are summarized rather than quantified.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Becton, Dickinson and Company (launch of a new point‑of‑care blood‑marker kit for early‑stage detection), Danaher Corporation (acquisition of an AI‑diagnostics start‑up to enhance imaging analysis), Exact Sciences Corporation (expansion of its Cologuard platform into the breast‑cancer biomarker space), General Electric Company (release of a low‑dose digital mammography system), Hologic, Inc. (introduction of a 3‑D tomosynthesis unit with integrated AI), Koninklijke Philips N.V. (partnership with Australian health networks for population‑wide screening), Myriad Genetics, Inc. (new BRCA‑focused genetic panel), OncoCyte Corporation (commercial rollout of a liquid‑biopsy test in Southeast Asia), POC Medical Systems (deployment of portable ultrasound devices in rural India), and Siemens Healthcare AG (launch of AI‑driven MRI protocols). These initiatives illustrate a market moving toward integrated, technology‑rich screening solutions.