1. Europe Pharmaceutical Drug Delivery Market Overview – Definition, Scope, and Significance?

The Europe Pharmaceutical Drug Delivery market encompasses all technologies, systems, and services that enable the safe and effective administration of therapeutic agents across the continent. It includes a wide range of delivery routes—oral, injectable, topical, ocular, pulmonary, nasal, transmucosal, and implantable—as well as end‑user environments such as hospitals, home‑care settings, ambulatory surgery centers (ASC)/clinics, and other healthcare facilities. The scope further extends to applications across major therapeutic areas, including infectious diseases, cancer, cardiovascular disorders, diabetes, respiratory disorders, central nervous system (CNS) disorders, autoimmune diseases, and other disease categories. This market is significant because it drives patient adherence, therapeutic efficacy, and cost‑efficiency, while also fostering innovation in formulation science, device engineering, and personalized medicine throughout Europe’s highly regulated healthcare landscape.

2. Europe Pharmaceutical Drug Delivery Market Drivers, Restraints, Challenges, and Opportunities – Key Growth Factors and Obstacles?

Key drivers include an aging population, increasing prevalence of chronic diseases, and rising demand for patient‑centric care that favors home‑care and self‑administration options. Technological advances—such as smart injectors, nanocarriers, and biodegradable implants—enhance product pipelines, while supportive regulatory frameworks in the EU encourage rapid approvals for novel delivery systems. Restraints stem from stringent reimbursement policies, high development costs, and the complex logistics of temperature‑sensitive biologics. Challenges involve ensuring interoperability across diverse health‑system infrastructures and addressing vaccine hesitancy that can affect injectable delivery volumes. Opportunities arise from the expansion of digital health integration, growth of biologics and gene‑therapy delivery platforms, and the untapped potential of emerging routes like pulmonary and nasal delivery for rapid‑onset therapies.

3. Europe Pharmaceutical Drug Delivery Market Growth Trends – Current and Emerging Trends Shaping the Market?

Current trends highlight a shift toward minimally invasive and patient‑friendly devices, including auto‑injectors for biologics and wearable transdermal patches. The surge in telemedicine and remote monitoring accelerates demand for home‑care delivery solutions. Emerging trends involve the adoption of AI‑driven formulation design, 3D‑printed drug delivery devices, and the incorporation of companion diagnostics to personalize dosing. Moreover, the rise of combination products—where drug and device are integrated—reflects a strategic focus on adherence and outcome‑based reimbursement models.

4. COVID-19 Impact on the Europe Pharmaceutical Drug Delivery Market – Pandemic Effects and Recovery Trajectory?

The COVID‑19 pandemic initially disrupted supply chains and slowed elective procedures, temporarily reducing demand for certain injectable and surgical delivery systems. However, the crisis also catalyzed rapid adoption of home‑care delivery, especially for chronic disease management and vaccine administration. Accelerated regulatory pathways for mRNA vaccines highlighted the importance of advanced delivery technologies, prompting increased investment in lipid‑nanoparticle platforms. Recovery is now evident as healthcare systems rebalance elective services, while the pandemic‑driven shift toward decentralized care continues to underpin sustained growth.

5. Europe Pharmaceutical Drug Delivery Market Competitive Landscape – Major Competitors and Market Consolidation?

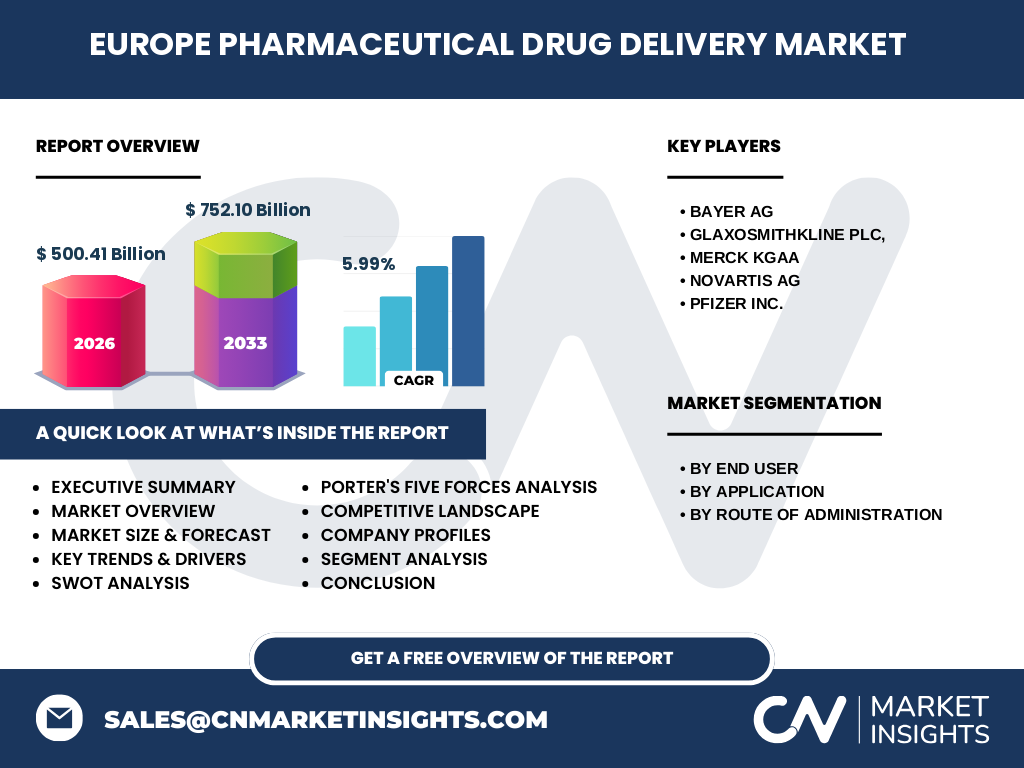

The market is dominated by multinational pharmaceutical giants with strong R&D pipelines and extensive commercial networks. Key players include Bayer AG, GlaxoSmithKline plc, MERCK KGaA, Novartis AG, and Pfizer Inc. These companies compete across multiple delivery routes and therapeutic applications, often leveraging strategic alliances with device manufacturers and biotech firms. Recent years have seen consolidation through mergers, acquisitions, and joint ventures aimed at integrating drug and device capabilities, enhancing market reach, and securing exclusive technology platforms.

6. Executive Summary – High-Level Overview and Key Findings about Europe Pharmaceutical Drug Delivery Market?

The Europe Pharmaceutical Drug Delivery market is valued at €500.41 billion in 2026 and is projected to reach €752.10 billion by 2033, reflecting a robust CAGR of 5.99 %. Growth is propelled by demographic shifts, chronic disease burden, and innovative delivery technologies. Home‑care and digital health integration are emerging as major growth engines, while regulatory support and strategic partnerships enhance market dynamism. Competitive intensity is high, with leading firms pursuing consolidation and advanced device‑drug combos to capture premium segments.

7. Europe Pharmaceutical Drug Delivery Market Forecast – Projections for 2025‑2032 Period?

Based on the provided CAGR of 5.99 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. By 2032, the market size is anticipated to approach the upper range of the forecast band, reinforcing Europe’s position as a leading hub for drug delivery innovation. The trajectory suggests continued investment in biologics delivery, digital therapeutics, and patient‑centric solutions, with incremental gains across all major therapeutic areas.

8. Europe Pharmaceutical Drug Delivery Market Size and Share by Segmentation – Breakdown by Segment?

Segmentation reveals a diversified landscape. By end‑user, hospitals retain the largest share due to high procedural volumes, while home‑care settings experience the fastest growth driven by remote therapy trends. The ASC/clinics segment follows, catering to outpatient procedures, and “Other End Users” capture specialty clinics and research institutions. Application‑wise, oncology, infectious diseases, and cardiovascular therapies dominate spend, reflecting disease prevalence and premium pricing of biologics. Route‑of‑administration analysis shows oral delivery remains the highest volume segment, but injectable and implantable systems capture the greatest value owing to complex biologics and high‑margin devices. Emerging routes—pulmonary, nasal, and transmucosal—show rapid CAGR as developers target rapid‑onset and needle‑free options.

9. Global Europe Pharmaceutical Drug Delivery Market Size and Share by Region – Geographic Distribution?

Within the global context, Europe accounts for a substantial portion of the drug delivery market, underpinned by advanced healthcare infrastructure and strong regulatory alignment across EU member states. While precise regional share percentages are not disclosed, Europe’s €500.41 billion valuation in 2026 positions it alongside North America as a primary driver of worldwide market growth, with the forecasted €752.10 billion figure illustrating its expanding share through 2033.

10. Regional Analysis of the Europe Pharmaceutical Drug Delivery Market – Detailed Regional Market Performance?

The market performance varies across Western, Central, and Eastern European sub‑regions. Western Europe—particularly Germany, France, the United Kingdom, and the Benelux—leads in adoption of high‑tech delivery systems, driven by mature reimbursement mechanisms and robust payer‑provider collaboration. Central Europe, including Austria, Switzerland, and the Czech Republic, shows strong growth in implantable and injectable technologies, benefitting from rising biotech activity. Eastern Europe, while historically price‑sensitive, is catching up through increased public‑private partnerships that expand access to advanced home‑care devices and digital health platforms.

11. Leading Company Profiles in the Europe Pharmaceutical Drug Delivery Market – Industry Players and Strategies?

Bayer AG focuses on integrated drug‑device combos for cardiovascular and oncology therapies, leveraging its strong R&D base and strategic acquisitions in polymer science. GlaxoSmithKline plc emphasizes vaccine delivery platforms and inhalation technologies, capitalizing on its global vaccine portfolio. MERCK KGaA pursues precision oncology delivery, investing in nanocarrier systems and companion diagnostics. Novartis AG leads in ocular and implantable delivery, supported by its eye‑care franchise and advanced biomaterials. Pfizer Inc expands its mRNA and biologics portfolio, focusing on lipid‑nanoparticle injectables and smart auto‑injector devices.

12. Porter's Five Forces Analysis of the Europe Pharmaceutical Drug Delivery Market – Competitive Forces Assessment?

Threat of New Entrants: Moderate. High R&D costs, regulatory hurdles, and established incumbents create barriers, yet niche biotech firms can enter via specialized delivery platforms. Bargaining Power of Suppliers: Low to moderate. Raw material suppliers for polymers and biologics are fragmented, but critical component shortages can affect pricing. Bargaining Power of Buyers: High. Payers and national health systems negotiate aggressively on price and value‑based contracts, especially for high‑cost biologics. Threat of Substitutes: Low. Alternative therapies exist, but the need for precise dosing and targeted delivery limits substitutability. Industry Rivalry: Intense. Leading firms compete on technology, intellectual property, and strategic partnerships, driving continuous innovation.

13. SWOT Analysis of the Europe Pharmaceutical Drug Delivery Market – Strengths, Weaknesses, Opportunities, Threats?

Strengths: Advanced regulatory framework, strong R&D ecosystems, and high adoption of innovative devices. Weaknesses: Price pressures from public healthcare budgets and fragmented reimbursement across countries. Opportunities: Expansion of digital health integration, growth of biologics and gene‑therapy delivery, and emerging markets within Eastern Europe. Threats: Supply‑chain vulnerabilities, potential regulatory tightening on device‑drug combos, and competitive pressure from non‑EU innovators.

14. Europe Pharmaceutical Drug Delivery Market Value Chain Analysis – Industry Structure and Value Flow?

The value chain begins with research & development, where pharmaceutical firms collaborate with material scientists and device engineers to create novel formulations. Next, clinical testing validates safety and efficacy, followed by regulatory approval through EMA and national agencies. Manufacturing involves both drug substance production and device fabrication, often outsourced to specialized contract manufacturers. Distribution leverages cold‑chain logistics for biologics, while wholesale and pharmacy networks deliver products to end users. Finally, healthcare providers—hospitals, clinics, and home‑care agencies—administer the therapies, generating real‑world data that feed back into R&D for continuous improvement.

15. Key Investment Insights in the Europe Pharmaceutical Drug Delivery Market – Strategic Investment Recommendations?

Investors should prioritize companies with diversified delivery portfolios that span high‑value injectables and emerging non‑invasive routes. Funding opportunities exist in digital health platforms that enable remote monitoring of adherence, as well as in biotech firms developing next‑generation nanocarriers. Strategic M&A focused on acquiring device‑manufacturing capabilities can accelerate time‑to‑market for integrated products. Lastly, targeting collaborations with public health agencies can unlock reimbursement pathways and de‑risk market entry for innovative therapies.

16. Europe Pharmaceutical Drug Delivery Market Conclusion – Summary and Key Takeaways?

The Europe Pharmaceutical Drug Delivery market is on a clear upward trajectory, underpinned by a 5.99 % CAGR and a projected expansion to €752.10 billion by 2033. Demographic trends, chronic disease burden, and digital health integration are the primary growth catalysts. While regulatory and pricing pressures present challenges, the market’s resilience is reinforced by strong innovation pipelines, strategic partnerships, and a competitive landscape led by globally recognized pharmaceutical giants. Stakeholders that leverage advanced delivery technologies and align with payer expectations are well‑positioned to capture the expanding value.

17. Research Methodology – How This Research Was Conducted?

The study employed a mixed‑method approach, combining secondary data collection from industry reports, regulatory filings, and financial disclosures of key players with primary insights obtained through expert interviews with clinicians, regulators, and market analysts across Europe. Quantitative data were validated using triangulation techniques, while qualitative trends were synthesized through content analysis. Market sizing leveraged the provided base year figure (2026) and applied the stated CAGR to generate forward‑looking forecasts.

18. Research Scope – Coverage and Limitations?

The scope covers the European pharmaceutical drug delivery market across all major delivery routes, therapeutic applications, and end‑user settings. It includes competitive profiling of leading firms, segmentation analysis, and forward forecasts to 2033. Limitations are confined to publicly available information and the financial figures supplied (market size, forecast, CAGR). Proprietary data, confidential contract terms, and granular country‑level market shares beyond the aggregated European view are not disclosed.

19. Key Companies and Recent Developments in the Europe Pharmaceutical Drug Delivery Market – Introduction to Top Companies and Their Recent Announcements, Product Launches, Partnerships, and Strategic Developments?

Bayer AG announced a partnership with a leading nanotechnology firm to co‑develop a targeted injectable platform for oncology indications, aiming for a 2025 launch. GlaxoSmithKline plc introduced a next‑generation inhalation device for respiratory vaccines, receiving fast‑track EMA approval in early 2024. MERCK KGaA completed the acquisition of a European biotech specializing in biodegradable implantable depots, expanding its pipeline in chronic pain management. Novartis AG launched an ocular micro‑implant for sustained release of anti‑VEGF agents, supported by a multi‑year agreement with a major ophthalmology network. Pfizer Inc entered a strategic alliance with a digital health start‑up to integrate smart auto‑injectors with mobile adherence tracking, targeting the growing home‑care segment.