What is the Metal Packaging Market overview including definition, scope, and significance?

The Metal Packaging Market encompasses the production, distribution, and utilization of packaging solutions manufactured from metal materials primarily aluminum and steel. This market serves as a critical component of global supply chains, providing durable, recyclable, and protective packaging for diverse end-use industries. The scope includes various product types such as bottles, cans, caps and closures, drums, and tubes. The market's significance lies in its ability to preserve product integrity, extend shelf life, and meet sustainability objectives through infinite recyclability. With a market size of 159.54 Billion in 2026, metal packaging remains a cornerstone of modern packaging solutions across food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, and automotive sectors.

What are the key drivers, restraints, challenges, and opportunities in the Metal Packaging Market?

Key drivers include growing demand for sustainable packaging solutions, increasing consumption of packaged food and beverages, and rising awareness about metal's infinite recyclability. The 3.23% CAGR reflects steady growth fueled by urbanization and changing consumer lifestyles. Restraints involve raw material price volatility, particularly for aluminum and steel, and high initial capital investment for manufacturing facilities. Challenges include competition from alternative packaging materials like plastics and glass, regulatory compliance across regions, and supply chain disruptions. Opportunities exist in lightweighting technologies, smart packaging integration, expanding applications in pharmaceuticals and personal care, and emerging markets where packaged goods consumption is accelerating rapidly.

What are the current and emerging growth trends shaping the Metal Packaging Market?

The Metal Packaging Market is witnessing several transformative trends. Lightweighting initiatives are reducing material usage while maintaining structural integrity across bottles, cans, and drums. Smart packaging technologies incorporating QR codes and NFC tags are enhancing consumer engagement and supply chain traceability. Sustainability-driven design focuses on increased recycled content and improved recyclability rates. The food & beverages segment continues dominating end-use applications, while personal care and pharmaceuticals show accelerated adoption of metal tubes and bottles for premium positioning. Customization and decorative finishing capabilities are expanding brand differentiation opportunities. Regional manufacturing localization is reducing logistics costs and carbon footprints across the value chain.

How did COVID-19 impact the Metal Packaging Market and what is the recovery trajectory?

The COVID-19 pandemic initially disrupted the Metal Packaging Market through supply chain interruptions, workforce limitations, and raw material procurement challenges. However, the market demonstrated resilience as essential industries like food & beverages and pharmaceuticals maintained steady demand for metal cans, bottles, and caps and closures. The pandemic accelerated e-commerce adoption, increasing demand for durable shipping packaging including drums and protective containers. Recovery trajectory shows normalization of operations with enhanced safety protocols. The market size progression from 159.54 Billion in 2026 toward 199.30 Billion by 2033 reflects post-pandemic stabilization and renewed growth momentum driven by sustained packaged goods consumption patterns established during lockdown periods.

What does the competitive landscape look like in the Metal Packaging Market?

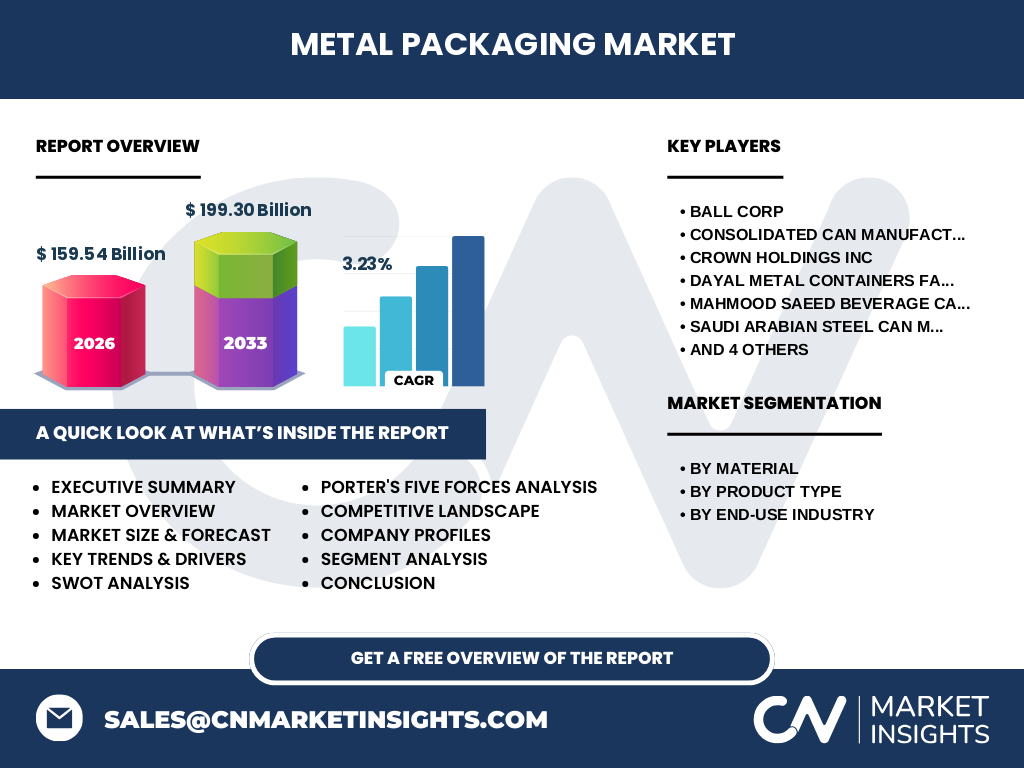

The Metal Packaging Market features a competitive landscape with established global players and regional specialists. Key companies include Ball Corp and Crown Holdings Inc as major international manufacturers, alongside regional leaders like Consolidated Can Manufacturing Co Ltd, Dayal Metal Containers Factory LLC, Mahmood Saeed Beverage Cans & Ends Industry Co Ltd, Saudi Arabian Steel Can Manufacturing Co, Saudi Can Co, Southern Can Making Co Ltd, Tengeh Noor Canvas Industry Co, and ZND Metal Cans. Competition centers on manufacturing capacity, technological innovation, geographic reach, and customer relationships across product segments including cans, bottles, caps and closures, drums, and tubes. Market consolidation trends show larger players expanding through strategic acquisitions and capacity expansions to strengthen positions in high-growth regions and end-use segments.

What are the key findings and high-level overview from the Metal Packaging Market executive summary?

The Metal Packaging Market demonstrates robust fundamentals with a 2026 market size of 159.54 Billion projected to reach 199.30 Billion by 2033 at a 3.23% CAGR. The market is segmented by material into aluminum and steel, by product type into bottles, cans, caps and closures, drums, and tubes, and by end-use industry spanning food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, and automotive. Key growth drivers include sustainability imperatives, packaged goods consumption growth, and technological advancements in manufacturing. The competitive landscape features both global leaders and regional specialists. Regional performance varies with mature markets showing steady growth while emerging economies present expansion opportunities. Investment potential exists across the value chain from raw material processing to finished packaging solutions.

What are the market forecast projections for the Metal Packaging Market from 2025-2032?

The Metal Packaging Market forecast indicates sustained growth trajectory with the market size expected to progress from 159.54 Billion in 2026 toward 199.30 Billion by 2033, representing a compound annual growth rate of 3.23%. This projection encompasses all material segments including aluminum and steel, product types covering bottles, cans, caps and closures, drums, and tubes, and end-use industries spanning food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, and automotive. The forecast period 2025-2032 captures the majority of this growth cycle, reflecting continued demand for sustainable packaging solutions, expanding applications in premium product segments, and geographic market penetration in developing regions where packaged goods consumption per capita is increasing.

What is the Metal Packaging Market size and share breakdown by segmentation including material, product type, and end-use industry?

The Metal Packaging Market segmentation reveals a diverse structure across three primary dimensions. By material, the market divides between aluminum and steel, each offering distinct properties for specific applications. By product type, the market encompasses bottles, cans, caps and closures, drums, and tubes, with cans traditionally representing the largest volume segment driven by food & beverages demand. By end-use industry, the market serves food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, and automotive sectors. Food & beverages typically commands the largest share due to high-volume consumption of canned products. The overall market size of 159.54 Billion in 2026 distributes across these segments with varying growth rates reflecting category-specific dynamics and regional preferences.

What is the global Metal Packaging Market size and share distribution by region?

The global Metal Packaging Market exhibits geographic diversity in market size and share distribution across key regions. While specific regional breakdowns are not provided in the available data, the market's 159.54 Billion valuation in 2026 and projected growth to 199.30 Billion by 2033 at 3.23% CAGR reflects contributions from mature markets in North America and Europe alongside rapidly expanding markets in Asia-Pacific, Middle East, and Latin America. The presence of regional players like Saudi Arabian Steel Can Manufacturing Co, Saudi Can Co, and Southern Can Making Co Ltd indicates significant Middle East market activity. Regional distribution correlates with manufacturing capacity, raw material availability, end-use industry concentration, and regulatory frameworks governing packaging standards and recycling requirements.

What does the detailed regional analysis reveal about Metal Packaging Market performance?

Regional analysis of the Metal Packaging Market reveals distinct performance characteristics across geographies. Mature markets in North America and Europe demonstrate steady growth driven by sustainability regulations, advanced recycling infrastructure, and premium packaging demand in personal care and pharmaceuticals. Asia-Pacific regions show accelerated expansion fueled by urbanization, rising disposable incomes, and growing packaged food consumption. The Middle East exhibits notable activity with multiple regional manufacturers including Saudi Arabian Steel Can Manufacturing Co, Saudi Can Co, and Southern Can Making Co Ltd serving local and export markets. Latin America and Africa present emerging opportunities as packaging penetration increases. Regional performance varies based on raw material access, labor costs, trade policies, and end-use industry development stages.

Who are the leading companies in the Metal Packaging Market and what are their strategies?

The Metal Packaging Market features prominent industry players pursuing diverse strategic approaches. Ball Corp and Crown Holdings Inc lead as global manufacturers with extensive product portfolios across cans, bottles, and caps and closures. Regional specialists include Consolidated Can Manufacturing Co Ltd, Dayal Metal Containers Factory LLC, Mahmood Saeed Beverage Cans & Ends Industry Co Ltd, Saudi Arabian Steel Can Manufacturing Co, Saudi Can Co, Southern Can Making Co Ltd, Tengeh Noor Canvas Industry Co, and ZND Metal Cans. Strategies encompass capacity expansion in high-growth markets, technological investment in lightweighting and decoration capabilities, sustainability initiatives increasing recycled content, geographic diversification through acquisitions and partnerships, and customer-centric innovation for specific end-use applications across food & beverages, personal care, pharmaceuticals, and industrial sectors.

What does Porter's Five Forces Analysis reveal about the Metal Packaging Market competitive forces?

Porter's Five Forces Analysis of the Metal Packaging Market indicates moderate to high competitive intensity. Threat of new entrants remains moderate due to high capital requirements for manufacturing facilities and established customer relationships of incumbents. Bargaining power of suppliers is significant given concentration in aluminum and steel raw material markets. Bargaining power of buyers varies by segment with large food & beverage companies wielding considerable influence while specialized pharmaceutical and personal care buyers have less leverage. Threat of substitutes is elevated from plastic, glass, and flexible packaging alternatives, though metal's recyclability and barrier properties provide defensive advantages. Competitive rivalry is intense among established players like Ball Corp, Crown Holdings Inc, and regional manufacturers competing on cost, innovation, and service across product types and geographies.

What are the strengths, weaknesses, opportunities, and threats in the Metal Packaging Market SWOT analysis?

SWOT analysis reveals key strategic factors for the Metal Packaging Market. Strengths include infinite recyclability, superior barrier properties, product protection capabilities, and established recycling infrastructure. Weaknesses encompass higher weight versus alternatives, energy-intensive production, raw material price volatility, and limited flexibility in shape customization compared to plastics. Opportunities exist in growing sustainability mandates, premium packaging demand in personal care and pharmaceuticals, lightweighting technology advancements, smart packaging integration, and emerging market penetration. Threats include aggressive competition from plastic and flexible packaging, regulatory cost increases, economic downturns reducing packaged goods consumption, supply chain disruptions affecting raw material availability, and potential substitution in traditional strongholds like beverage cans.

What does the Metal Packaging Market value chain analysis show about industry structure and value flow?

The Metal Packaging Market value chain encompasses multiple stages from raw material extraction to end-user delivery. Upstream begins with aluminum and steel production including mining, refining, and rolling processes. Midstream involves coating, printing, and forming operations converting flat sheets into bottles, cans, caps and closures, drums, and tubes through manufacturers like Ball Corp, Crown Holdings Inc, and regional players. Downstream includes filling operations across food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, and automotive sectors. Value flow distributes across material suppliers, packaging converters, brand owners, retailers, and recycling systems. Integration levels vary with some players operating across multiple stages while others specialize. The 159.54 Billion market size reflects cumulative value addition across this chain with recycling creating circular value recovery loops.

What are the key investment insights and strategic recommendations for the Metal Packaging Market?

Key investment insights for the Metal Packaging Market highlight several strategic priorities. Capacity expansion in emerging markets offers growth alignment with the 3.23% CAGR trajectory toward 199.30 Billion by 2033. Technology investments in lightweighting, advanced coatings, and digital printing enhance competitiveness across product types including cans, bottles, and caps and closures. Sustainability-focused investments in recycled content capabilities and closed-loop systems address regulatory and consumer demands. Geographic diversification reduces concentration risk with Middle East presence through players like Saudi Arabian Steel Can Manufacturing Co and Saudi Can Co demonstrating regional potential. End-use segment expansion into pharmaceuticals and personal care offers premium margins. M&A opportunities exist for scale attainment and technology acquisition. Risk mitigation requires raw material hedging strategies and supply chain resilience investments.

What are the summary and key takeaways from the Metal Packaging Market conclusion?

The Metal Packaging Market concludes with strong fundamentals supporting continued growth from 159.54 Billion in 2026 to 199.30 Billion by 2033 at 3.23% CAGR. The market's dual-material foundation rests on metal's unique sustainability proposition of infinite recyclability, superior product protection across bottles, cans, caps and closures, drums, and tubes, and established positions in critical end-use industries including food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, and automotive. Competitive dynamics feature global leaders Ball Corp and Crown Holdings Inc alongside regional specialists. Success factors include technological innovation in lightweighting and decoration, sustainability credential enhancement, geographic expansion in emerging markets, and customer intimacy in high-value segments. The market's resilience through COVID-19 demonstrates essential industry status with enduring demand characteristics.

What research methodology was used to conduct this Metal Packaging Market analysis?

The research methodology for this Metal Packaging Market analysis employs a comprehensive multi-source approach combining primary and secondary research techniques. Primary research includes interviews with industry executives from key companies such as Ball Corp, Crown Holdings Inc, Consolidated Can Manufacturing Co Ltd, and regional manufacturers. Secondary research encompasses company annual reports, industry association publications, government statistics, trade databases, and technical literature. Market sizing utilizes bottom-up and top-down approaches validated through triangulation. Segmentation analysis covers material types (aluminum, steel), product types (bottles, cans, caps and closures, drums, tubes), and end-use industries (food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, automotive). Forecast modeling incorporates macroeconomic indicators, industry trends, and company-specific guidance for the 2025-2032 projection period.

What is the research scope and coverage limitations for this Metal Packaging Market report?

The research scope for this Metal Packaging Market report encompasses global market analysis covering the forecast period 2025-2032 with base year 2026 valuation of 159.54 Billion and projected 199.30 Billion by 2033 at 3.23% CAGR. Coverage includes segmentation by material (aluminum, steel), product type (bottles, cans, caps and closures, drums, tubes), and end-use industry (food & beverages, personal care, consumer goods, pharmaceuticals, paints & coatings, automotive). Geographic scope spans global markets with regional analysis. Company coverage includes major players Ball Corp, Crown Holdings Inc, Consolidated Can Manufacturing Co Ltd, Dayal Metal Containers Factory LLC, Mahmood Saeed Beverage Cans & Ends Industry Co Ltd, Saudi Arabian Steel Can Manufacturing Co, Saudi Can Co, Southern Can Making Co Ltd, Tengeh Noor Canvas Industry Co, and ZND Metal Cans. Limitations include reliance on publicly available data, exclusion of niche applications, and forecast uncertainty inherent in long-range projections.

What are the key companies and their recent developments in the Metal Packaging Market?

The Metal Packaging Market features key companies driving industry developments through strategic initiatives. Ball Corp and Crown Holdings Inc continue leading global innovation in can manufacturing, lightweighting technologies, and sustainability programs. Regional manufacturers including Consolidated Can Manufacturing Co Ltd, Dayal Metal Containers Factory LLC, Mahmood Saeed Beverage Cans & Ends Industry Co Ltd, Saudi Arabian Steel Can Manufacturing Co, Saudi Can Co, Southern Can Making Co Ltd, Tengeh Noor Canvas Industry Co, and ZND Metal Cans are expanding capacities and enhancing product portfolios across bottles, cans, caps and closures, drums, and tubes. Recent industry developments focus on increased recycled content adoption, advanced decorative finishes for premium positioning in personal care and beverages, smart packaging integration for traceability, and geographic expansion into high-growth markets. Strategic partnerships across the value chain enhance circular economy initiatives and supply chain resilience.