What is the Asia Pacific Touch Panel Market overview including definition, scope, and significance?

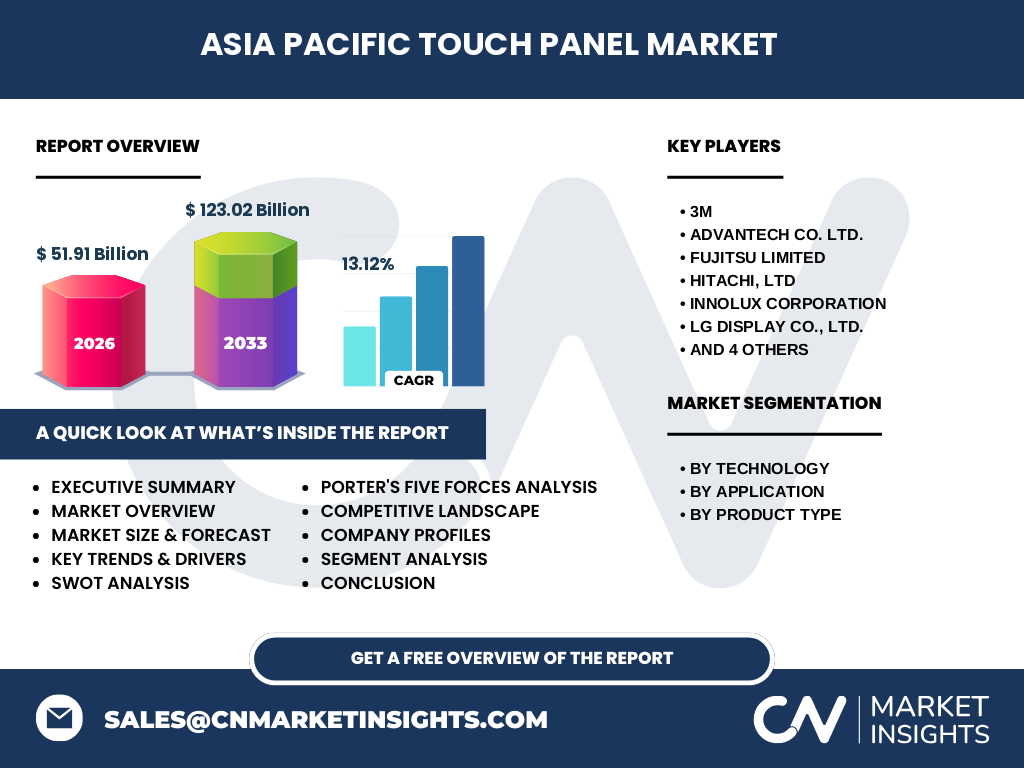

The Asia Pacific Touch Panel Market encompasses the development, manufacturing, and deployment of interactive display technologies across the region. This market includes resistive, capacitive, and infrared touch technologies serving consumer electronics, medical devices, retail systems, and industrial applications. The market's significance stems from Asia Pacific's position as the global manufacturing hub for display technologies, with countries like China, Japan, South Korea, and Taiwan driving innovation. The market valuation reached 51.91 Billion in 2026, reflecting the region's dominance in touch panel production and consumption across smartphones, tablets, automotive displays, and industrial control systems.

What are the key drivers, restraints, challenges, and opportunities in the Asia Pacific Touch Panel Market?

Key drivers include increasing smartphone penetration, growing demand for interactive displays in retail and healthcare, and automotive industry adoption of touch interfaces. The 13.12% CAGR reflects strong growth momentum. Restraints involve raw material price volatility and technical complexities in large-format touch panel manufacturing. Challenges include intense competition among established players like Samsung and LG Display, intellectual property disputes, and supply chain disruptions. Opportunities emerge from foldable display technologies, automotive touch integration, medical device modernization, and industrial automation requiring ruggedized touch solutions across the region's diverse economies.

What are the current and emerging growth trends shaping the Asia Pacific Touch Panel Market?

Current trends include the transition from resistive to capacitive technology dominance, increasing adoption of in-cell and on-cell touch integration, and growing demand for flexible and foldable display panels. Emerging trends feature automotive-grade touch panels with haptic feedback, antimicrobial coatings for medical applications, and large-format interactive displays for retail and education. The market shows strong movement toward energy-efficient touch controllers and integration with 5G-enabled devices. Regional manufacturers are investing heavily in next-generation oxide TFT backplanes and micro-LED touch integration to maintain competitive advantages.

How did COVID-19 impact the Asia Pacific Touch Panel Market and what is the recovery trajectory?

COVID-19 initially disrupted supply chains across China, Taiwan, and South Korea, causing production delays and logistics challenges. However, the pandemic accelerated digital transformation, boosting demand for touch-enabled devices in remote work, e-learning, and contactless retail solutions. Medical applications saw increased touch panel adoption for diagnostic equipment and patient monitoring systems. The recovery trajectory has been strong, with the market projected to grow from 51.91 Billion in 2026 to 123.02 Billion by 2033, indicating robust post-pandemic recovery driven by pent-up demand and accelerated technology adoption across all application segments.

What is the competitive landscape of the Asia Pacific Touch Panel Market including major competitors and market consolidation?

The competitive landscape features established global leaders including Samsung, LG Display Co. Ltd., Innolux Corporation, and FUJITSU LIMITED alongside specialized players like 3M, Advantech Co. Ltd., Hitachi Ltd., Planar, Renesas Electronics Corporation, and Xenarc Technologies Corporation. Market consolidation is evident through strategic partnerships, technology licensing agreements, and vertical integration initiatives. Major players compete on manufacturing scale, technology innovation, and cost optimization. Korean and Taiwanese manufacturers dominate large-format panels, while Japanese firms excel in automotive and industrial applications. Chinese manufacturers are rapidly expanding capacity across all technology segments.

What are the key findings and high-level overview of the Asia Pacific Touch Panel Market?

The Asia Pacific Touch Panel Market demonstrates exceptional growth potential with a projected expansion from 51.91 Billion in 2026 to 123.02 Billion by 2033 at a 13.12% CAGR. The region maintains global leadership in touch panel manufacturing and innovation across resistive, capacitive, and infrared technologies. Key applications span consumer electronics, medical devices, retail systems, and industrial automation. Competitive dynamics favor vertically integrated manufacturers with strong R&D capabilities. The market benefits from robust electronics ecosystems in China, Japan, South Korea, and Taiwan, supported by government initiatives promoting advanced display manufacturing and domestic technology self-sufficiency.

What are the market projections for the Asia Pacific Touch Panel Market from 2025-2032?

The Asia Pacific Touch Panel Market is forecast to reach 123.02 Billion by 2033, growing from 51.91 Billion in 2026 at a compound annual growth rate of 13.12%. This growth trajectory reflects sustained demand across all technology segments and applications. The forecast period 2025-2032 will see continued expansion driven by automotive touch integration, foldable smartphone adoption, medical device modernization, and industrial automation upgrades. Capacitive technology is expected to maintain dominant market share while infrared solutions gain traction in large-format commercial displays. Regional manufacturing capacity expansions in China, Vietnam, and India will support volume growth.

What is the market size and share breakdown by technology, application, and product type segments?

The market segmentation reveals three primary technology categories: resistive, capacitive, and infrared touch panels, each serving distinct application requirements. Applications span consumer electronics, medical devices, retail systems, and industrial automation with varying technology preferences. Product types divide into consumer-grade and commercial/industrial-grade panels reflecting durability and performance specifications. Capacitive technology leads in consumer applications due to multi-touch capability and optical clarity. Resistive panels maintain relevance in industrial and medical environments requiring glove compatibility. Infrared solutions dominate large-format retail and commercial displays. The commercial and industrial segment commands premium pricing for ruggedized specifications.

What is the global market size and geographic distribution of the Asia Pacific Touch Panel Market?

The Asia Pacific region represents the dominant global market for touch panel technologies, accounting for the substantial majority of worldwide production and consumption. The regional market valuation of 51.91 Billion in 2026 underscores this leadership position. Key manufacturing hubs include China, Japan, South Korea, and Taiwan, each specializing in different technology segments and application areas. The geographic distribution reflects established electronics supply chains, skilled workforce availability, and government support for advanced manufacturing. Regional trade flows show significant intra-Asia component exchange with final assembly concentrated in China and Vietnam for global export markets.

How does regional performance vary across the Asia Pacific Touch Panel Market?

Regional performance varies significantly across Asia Pacific with distinct specialization patterns. China leads in volume manufacturing across all technology types, supported by massive domestic demand and export capabilities. South Korea excels in premium capacitive panels for smartphones and automotive applications through Samsung and LG Display. Japan maintains strength in automotive-grade and industrial touch technologies with companies like FUJITSU and Hitachi. Taiwan specializes in panel manufacturing services through Innolux and other foundries. Southeast Asian nations including Vietnam and Thailand are emerging as alternative manufacturing bases, attracting investment for supply chain diversification.

Who are the leading companies in the Asia Pacific Touch Panel Market and what are their strategies?

Leading companies include Samsung and LG Display Co. Ltd. dominating premium capacitive technologies, Innolux Corporation as a major panel manufacturer, and FUJITSU LIMITED with Hitachi Ltd. leading automotive and industrial segments. 3M and Advantech Co. Ltd. specialize in commercial and industrial touch solutions. Planar and Xenarc Technologies Corporation focus on ruggedized and specialized displays. Renesas Electronics Corporation provides touch controller ICs. Strategies emphasize vertical integration, R&D investment in flexible displays, automotive qualification programs, and geographic expansion. Partnerships with smartphone OEMs and automotive Tier 1 suppliers secure long-term demand visibility.

What does Porter's Five Forces analysis reveal about the Asia Pacific Touch Panel Market?

Porter's Five Forces analysis indicates high competitive rivalry among established manufacturers like Samsung, LG Display, and Innolux driving technology innovation and cost reduction. Supplier power is moderate with specialized material suppliers for ITO, cover glass, and controller ICs. Buyer power is significant for large OEMs like smartphone and automotive manufacturers who dictate specifications and pricing. Threat of substitutes remains low as touch interfaces are integral to modern device designs, though voice and gesture control represent emerging alternatives. Barriers to entry are high due to capital intensity, technology complexity, and customer qualification requirements, protecting incumbent positions.

What are the strengths, weaknesses, opportunities, and threats in the Asia Pacific Touch Panel Market SWOT analysis?

Strengths include established manufacturing ecosystems, skilled workforce, strong R&D capabilities, and domestic demand scale. Weaknesses involve overcapacity risks in certain segments, dependence on key raw materials, and intellectual property concentration. Opportunities encompass automotive touch expansion, foldable device proliferation, medical device modernization, and industrial automation growth supporting the 13.12% CAGR trajectory. Threats include geopolitical trade tensions, supply chain vulnerabilities, technology obsolescence risks, and emerging competition from alternative interface technologies. The forecast growth to 123.02 Billion by 2033 reflects net positive opportunity assessment.

How does the value chain operate in the Asia Pacific Touch Panel Market?

The value chain flows from upstream material suppliers providing ITO films, cover glass, adhesives, and controller ICs to panel manufacturers performing sensor patterning, lamination, and module assembly. Midstream includes touch module integrators and display manufacturers incorporating touch functionality. Downstream encompasses device OEMs in smartphones, automotive, medical, retail, and industrial sectors. Regional value chains are highly integrated with China, Taiwan, South Korea, and Japan each hosting multiple value chain stages. Vertical integration trends see panel manufacturers expanding into controller IC design and module assembly to capture additional value and control quality.

What are the key investment insights for the Asia Pacific Touch Panel Market?

Strategic investment opportunities align with the projected growth from 51.91 Billion to 123.02 Billion at 13.12% CAGR. Priority areas include capacitive touch capacity for automotive and foldable applications, next-generation oxide TFT manufacturing, and micro-LED touch integration. Investment in domestic supply chain resilience for critical materials reduces geopolitical risk. R&D investments in haptic feedback, antimicrobial coatings, and energy-efficient controllers address emerging application requirements. Geographic diversification into Vietnam, India, and Southeast Asia mitigates concentration risk. Partnerships with automotive OEMs and medical device manufacturers provide stable long-term demand visibility.

What are the summary conclusions and key takeaways for the Asia Pacific Touch Panel Market?

The Asia Pacific Touch Panel Market represents a high-growth technology sector with robust fundamentals supporting expansion from 51.91 Billion to 123.02 Billion by 2033. Regional manufacturing dominance, technology leadership across resistive, capacitive, and infrared segments, and diverse application penetration create sustainable competitive advantages. Key success factors include automotive qualification capabilities, flexible display manufacturing expertise, and supply chain integration. The market's 13.12% CAGR reflects structural demand drivers across consumer, medical, retail, and industrial applications. Continued investment in advanced manufacturing and technology innovation will maintain Asia Pacific's global leadership position.

What research methodology was used to analyze the Asia Pacific Touch Panel Market?

The research methodology combines primary and secondary research approaches for comprehensive market analysis. Primary research includes interviews with industry executives, technology experts, and key opinion leaders across the value chain. Secondary research encompasses financial reports, patent analyses, government publications, trade association data, and technical literature from major manufacturers including Samsung, LG Display, Innolux, and FUJITSU. Market modeling uses bottom-up approaches based on production capacity, technology adoption rates, and application penetration metrics. Forecast validation employs scenario analysis and expert review to ensure projection reliability for the 2025-2032 period.

What is the research scope and coverage limitations for the Asia Pacific Touch Panel Market analysis?

The research scope covers the Asia Pacific Touch Panel Market across all major technology types including resistive, capacitive, and infrared touch panels. Application coverage spans consumer electronics, medical devices, retail systems, and industrial automation. Product type analysis includes both consumer and commercial/industrial grade segments. Geographic coverage encompasses all major Asia Pacific economies with manufacturing or consumption activity. The analysis period extends from historical data through 2026 baseline to 2033 forecasts. Coverage includes the ten identified key companies and their competitive positioning within the regional market ecosystem.

What are the key companies and recent developments in the Asia Pacific Touch Panel Market?

Key companies driving market development include Samsung and LG Display Co. Ltd. advancing foldable and automotive touch technologies, Innolux Corporation expanding manufacturing capacity, and FUJITSU LIMITED with Hitachi Ltd. strengthening automotive and industrial portfolios. 3M and Advantech Co. Ltd. focus on commercial touch solutions while Planar and Xenarc Technologies Corporation develop ruggedized displays. Renesas Electronics Corporation innovates in touch controller ICs. Recent developments center on flexible display manufacturing, automotive touch qualification, antimicrobial coating technologies, and supply chain localization initiatives. Strategic partnerships between panel makers and device OEMs accelerate technology adoption across all application segments.