What is the definition, scope, and significance of the North America Music Streaming Market?

The North America Music Streaming Market encompasses digital platforms that deliver audio and video music content to end users via live or on‑demand streaming. It serves both individual consumers and commercial entities such as businesses and public venues. The market is significant because it reflects shifting consumption habits, drives revenue for record labels and artists, and fuels innovation in content delivery, personalization, and monetization across the region.

What are the key drivers, restraints, challenges, and opportunities shaping the North America Music Streaming Market?

Drivers include widespread smartphone adoption, high‑speed internet penetration, and growing preference for on‑demand content. Restraints involve licensing complexities, royalty disputes, and market saturation in mature segments. Challenges center on maintaining subscriber growth amid intense competition and evolving consumer expectations. Opportunities arise from expanding podcast integration, AI‑driven recommendation engines, and emerging revenue models such as live virtual concerts and direct artist‑fan monetization.

What current and emerging trends are influencing the North America Music Streaming Market?

Trends include the rise of hybrid audio‑video streaming, increased focus on exclusive content and artist collaborations, and the integration of social features like shared playlists. Personalization powered by machine learning, expansion into high‑fidelity lossless audio, and the growth of user‑generated content platforms are reshaping engagement. Additionally, bundling with telecom and hardware subscriptions is accelerating subscriber acquisition.

How did COVID‑19 impact the North America Music Streaming Market and what is the recovery trajectory?

The pandemic accelerated digital adoption as live events were cancelled, driving a surge in streaming hours and new subscriber sign‑ups. While initial lockdowns boosted usage, the market has stabilized with sustained higher baseline engagement. Recovery is marked by continued investment in exclusive live‑streamed performances and podcast content, reinforcing long‑term growth beyond the pandemic spike.

What does the competitive landscape look like for the North America Music Streaming Market?

The market is highly consolidated around major players including Amazon.com, Inc., Apple, Inc., Deezer, Google LLC, Pandora Media, LLC, SoundCloud, Spotify Technology S.A., Tidal, and iHeartMedia Inc. These companies compete on content breadth, pricing tiers, platform ecosystem integration, and exclusive partnerships. Strategic acquisitions, podcast investments, and technology enhancements are common tactics to defend and expand market share.

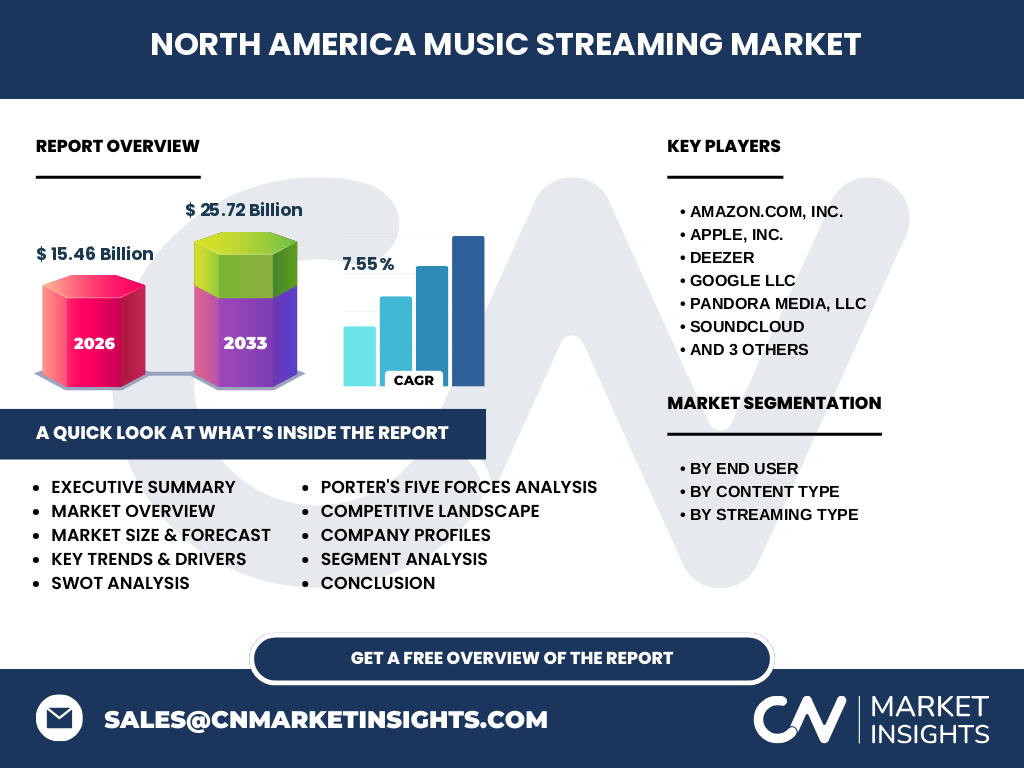

What are the key findings and high‑level overview of the North America Music Streaming Market?

The North America Music Streaming Market was valued at 15.46 billion in 2026 and is projected to reach 25.72 billion by 2033, growing at a CAGR of 7.55%. Growth is fueled by individual and commercial demand across audio and video streaming, with on‑demand and live formats both expanding. Leading platforms continue to innovate in content curation, monetization, and user experience to capture evolving listener preferences.

What are the market projections for the 2025‑2032 period?

Based on the available forecast covering 2027‑2033, the market is expected to grow from 15.46 billion in 2026 to 25.72 billion by 2033, reflecting a 7.55% CAGR. While the specific 2025‑2032 window is not separately quantified, the trajectory indicates steady expansion driven by subscriber growth, content diversification, and emerging revenue streams across all defined segments.

How is the North America Music Streaming Market segmented by end user, content type, and streaming type?

The market is segmented by end user into Commercial and Individual categories. By content type, it divides into Audio Streaming and Video Streaming. By streaming type, it splits into Live Streaming and On‑demand Streaming. Each segment addresses distinct usage patterns: individuals favor on‑demand audio, while commercial venues often leverage live and video streams for ambient and event‑driven experiences.

What is the geographic distribution of the North America Music Streaming Market across regions?

The market is predominantly concentrated in the United States, which accounts for the largest share of subscribers and revenue, followed by Canada and Mexico. Urban centers with robust broadband infrastructure drive higher penetration rates. Regional variations reflect differences in disposable income, cultural preferences, and regulatory environments affecting licensing and content availability.

What are the detailed regional performance dynamics within the North America Music Streaming Market?

In the United States, high smartphone penetration and a mature digital ecosystem sustain strong growth across all segments. Canada shows increasing adoption of high‑fidelity audio and podcast integration. Mexico exhibits rapid mobile‑first adoption, with growing demand for localized content and affordable subscription tiers. Each region presents unique opportunities for tailored content strategies and partnership models.

Who are the leading companies in the North America Music Streaming Market and what are their strategies?

Key players include Amazon.com, Inc., Apple, Inc., Deezer, Google LLC, Pandora Media, LLC, SoundCloud, Spotify Technology S.A., Tidal, and iHeartMedia Inc. Strategies focus on exclusive content acquisition, podcast ecosystem expansion, AI‑driven personalization, hardware bundling, and international licensing agreements. Investments in live‑streaming technology and direct artist monetization tools further differentiate their offerings.

How does Porter’s Five Forces analysis apply to the North America Music Streaming Market?

The threat of new entrants is moderate due to high licensing barriers and network effects. Supplier power is significant as major record labels control essential catalogs. Buyer power is high with low switching costs and multiple alternatives. Competitive rivalry is intense among established platforms. The threat of substitutes includes free ad‑supported services, radio, and user‑generated content platforms.

What are the strengths, weaknesses, opportunities, and threats (SWOT) for the North America Music Streaming Market?

Strengths include large addressable audiences, advanced technology infrastructure, and diverse monetization models. Weaknesses involve high royalty costs, dependency on third‑party content, and churn risk. Opportunities lie in podcast growth, AI personalization, emerging markets within North America, and new revenue streams like virtual concerts. Threats encompass regulatory changes, economic downturns, and disruptive technologies.

What does the value chain analysis reveal about the North America Music Streaming Market?

The value chain begins with content creators and rights holders, moves through licensing aggregators and streaming platforms, and ends with distribution to end users via apps and devices. Platforms add value through curation, recommendation algorithms, and user experience design. Revenue flows back through subscription fees, advertising, and partnership deals, supporting ongoing content acquisition and platform innovation.

What are the key investment insights for stakeholders in the North America Music Streaming Market?

Investors should focus on platforms with strong exclusive content pipelines, robust podcast strategies, and scalable technology stacks. Opportunities exist in companies leveraging AI for personalization, expanding into live‑streamed events, and developing direct‑to‑artist monetization tools. Diversification across audio, video, and commercial segments mitigates risk and captures multiple revenue streams.

What are the concluding takeaways for the North America Music Streaming Market?

The market demonstrates sustained growth driven by evolving consumer habits, technological advancements, and strategic content investments. With a 2026 valuation of 15.46 billion and a forecast of 25.72 billion by 2033 at a 7.55% CAGR, stakeholders should prioritize innovation in user experience, content exclusivity, and flexible monetization to maintain competitive advantage.

What research methodology was used to analyze the North America Music Streaming Market?

The analysis combines primary research, including interviews with industry executives and surveys of streaming subscribers, with secondary research from financial reports, regulatory filings, and reputable market databases. Quantitative modeling uses historical trends, segment breakdowns, and macroeconomic indicators to project market size, share, and growth rates across the forecast horizon.

What is the scope and coverage of this research on the North America Music Streaming Market?

The research covers the period 2026‑2033, focusing on the North America region including the United States, Canada, and Mexico. It examines market size, segmentation by end user, content type, and streaming type, competitive landscape, and strategic insights for key companies. Limitations include reliance on publicly available data and exclusion of non‑streaming music revenue sources.

What are the recent developments and announcements from the top companies in the North America Music Streaming Market?

Recent developments include Spotify Technology S.A. expanding its podcast studio partnerships, Apple, Inc. launching lossless audio tiers, Amazon.com, Inc. integrating live‑streamed concert features, Google LLC enhancing YouTube Music with AI recommendations, and Tidal introducing direct artist payment tools. Deezer, Pandora Media, LLC, SoundCloud, and iHeartMedia Inc. have also announced new content deals and platform upgrades to boost engagement.