What is the Rugged Handheld Devices Market Overview – definition, scope, and significance?

The rugged handheld devices market encompasses portable computing equipment engineered to withstand harsh environmental conditions such as extreme temperatures, moisture, dust, and shock. The scope includes semi‑rugged, fully‑rugged, and ultra‑rugged categories across mobile computers, tablets, and phones serving industrial, commercial, military, and government sectors. Its significance lies in enabling reliable data capture, communication, and workflow automation in field operations where standard consumer devices would fail, driving productivity and safety across critical industries.

What are the key drivers, restraints, challenges, and opportunities in the Rugged Handheld Devices Market?

Primary drivers include rising demand for real‑time data in logistics, manufacturing, and defense, alongside increasing adoption of IoT and Industry 4.0 initiatives. Restraints involve high upfront costs and limited consumer awareness in emerging regions. Challenges center on rapid technology obsolescence and stringent certification requirements. Opportunities arise from expanding 5G connectivity, growing need for contactless solutions post‑pandemic, and untapped markets in Asia‑Pacific and South America where infrastructure modernization is accelerating.

What current and emerging growth trends are shaping the Rugged Handheld Devices Market?

Trends include a shift toward fully‑rugged and ultra‑rugged form factors to meet stricter MIL‑STD standards, integration of advanced barcode scanning, RFID, and biometric authentication, and the convergence of rugged smartphones with enterprise‑grade mobile computers. Cloud‑based device management platforms and AI‑enabled analytics are gaining traction, while sustainability initiatives push manufacturers toward longer product lifecycles and modular designs that reduce e‑waste.

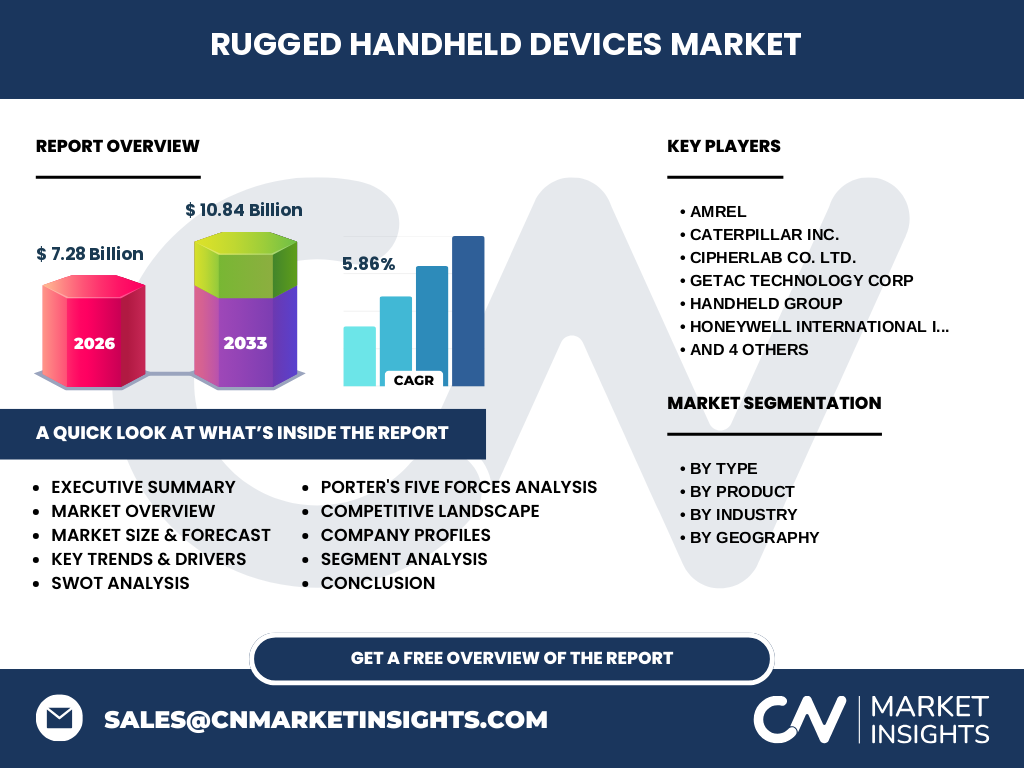

How did COVID‑19 impact the Rugged Handheld Devices Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed procurement, especially in commercial and industrial segments. However, heightened focus on contactless operations, remote asset tracking, and field service continuity accelerated demand for rugged tablets and mobile computers in healthcare, logistics, and public safety. Recovery has been robust, with the market reaching a 2026 size of 7.28 Billion and a projected forecast of 10.84 Billion by 2033, reflecting a CAGR of 5.86 % as organizations prioritize resilient hardware investments.

What does the competitive landscape of the Rugged Handheld Devices Market look like?

The market is moderately consolidated with leading players such as Zebra Technologies Corporation, Honeywell International Inc., Panasonic Corporation, Getac Technology Corp, and Caterpillar Inc. dominating revenue share. These firms compete on ruggedness certifications, software ecosystems, and global service networks. Mid‑size specialists like CipherLab Co. Ltd., Handheld Group, Kyocera Corporation, AMREL, and TouchStar Technologies Ltd. differentiate through niche vertical solutions and regional channel strength, fostering a dynamic competitive environment.

What are the key findings in the Executive Summary of the Rugged Handheld Devices Market report?

The executive summary highlights a 2026 market valuation of 7.28 Billion, forecasting growth to 10.84 Billion by 2033 at a 5.86 % CAGR. Fully‑rugged and ultra‑rugged segments lead revenue, driven by industrial and military procurement. North America and Europe remain the largest regional markets, while Asia‑Pacific shows the fastest growth. Strategic investments in 5G, AI analytics, and modular designs are identified as pivotal for sustained competitive advantage.

What are the market forecast projections for the Rugged Handheld Devices Market for the 2025‑2032 period?

Although the provided data specifies a 2026 base of 7.28 Billion and a 2027‑2033 forecast of 10.84 Billion, the implied trajectory for 2025‑2032 aligns with a consistent 5.86 % CAGR. The market is expected to surpass 9 Billion by 2029 and approach the 10.84 Billion mark before 2033, reflecting steady demand across all product types and industry verticals throughout the forecast horizon.

How is the Rugged Handheld Devices Market sized and shared by segmentation?

Segmentation analysis breaks the market into three type categories – semi‑rugged, fully‑rugged, and ultra‑rugged – with fully‑rugged and ultra‑rugged capturing the majority of revenue due to stringent defense and industrial standards. By product, mobile computers lead, followed by tablets and phones. Industry segmentation shows industrial and military sectors as primary contributors, while commercial and government segments grow steadily. Geographic split covers North America, Europe, Asia‑Pacific, South and Central America, and Middle East & Africa.

What is the global Rugged Handheld Devices Market size and share by region?

The global market, valued at 7.28 Billion in 2026, is distributed across five key regions. North America and Europe together account for the largest share, driven by mature industrial bases and defense budgets. Asia‑Pacific is the fastest‑growing region, propelled by manufacturing expansion and government modernization programs. South and Central America and the Middle East & Africa represent emerging opportunities with increasing infrastructure investments.

What does the regional analysis reveal about the Rugged Handheld Devices Market performance?

Regional analysis indicates North America leads in technology adoption and high‑value procurement, especially for ultra‑rugged devices in military and public safety. Europe follows with strong demand in automotive and logistics. Asia‑Pacific exhibits double‑digit growth rates as countries like China, India, and Japan ramp up smart factory initiatives. South and Central America and the Middle East & Africa show gradual uptake, supported by oil & gas, mining, and government digitization projects.

Who are the leading company profiles in the Rugged Handheld Devices Market and what are their strategies?

Key players include Zebra Technologies Corporation, Honeywell International Inc., Panasonic Corporation, Getac Technology Corp, Caterpillar Inc., CipherLab Co. Ltd., Handheld Group, Kyocera Corporation, AMREL, and TouchStar Technologies Ltd. Strategies focus on expanding ruggedness certifications, integrating 5G and AI capabilities, broadening software ecosystems, and strengthening global service and support networks. Partnerships with cloud providers and vertical‑specific solution bundles are common to deepen customer lock‑in.

What does Porter’s Five Forces analysis indicate for the Rugged Handheld Devices Market?

Porter’s analysis shows moderate threat of new entrants due to high R&D and certification barriers. Supplier power is low as component sources are diversified. Buyer power is moderate; large enterprise and government buyers negotiate volume discounts but require specialized features. Threat of substitutes is limited because consumer devices cannot meet rugged standards. Competitive rivalry is high among established vendors competing on durability, software, and total cost of ownership.

What are the strengths, weaknesses, opportunities, and threats (SWOT) for the Rugged Handheld Devices Market?

Strengths include proven reliability in mission‑critical environments and strong brand loyalty among enterprise users. Weaknesses involve higher price points and longer product development cycles. Opportunities lie in 5G rollout, IoT integration, and expanding into emerging markets. Threats encompass economic downturns reducing capital expenditure, rapid consumer tech advances blurring rugged definitions, and potential regulatory changes affecting defense procurement.

How does the value chain operate in the Rugged Handheld Devices Market?

The value chain begins with raw material and component suppliers (processors, displays, rugged enclosures), followed by OEM design and engineering, contract manufacturing, and rigorous testing for MIL‑STD and IP certifications. Finished devices move through distribution channels – value‑added resellers, system integrators, and direct sales – to end users in industrial, commercial, military, and government sectors. Post‑sale services such as device management, repair, and software updates complete the loop, adding recurring revenue streams.

What are the key investment insights for the Rugged Handheld Devices Market?

Investors should target companies with strong portfolios in fully‑rugged and ultra‑rugged segments, robust software ecosystems, and established government contracts. Growth vectors include 5G‑enabled devices, AI‑driven analytics platforms, and modular hardware that extends product lifecycles. Geographic focus on Asia‑Pacific and Latin America offers higher CAGR potential. Risk mitigation involves monitoring component supply constraints and evolving defense budget cycles.

What conclusions and key takeaways can be drawn from the Rugged Handheld Devices Market analysis?

The market is on a steady growth path, reaching 7.28 Billion in 2026 and projected to hit 10.84 Billion by 2033 at a 5.86 % CAGR. Fully‑rugged and ultra‑rugged devices dominate, driven by industrial automation and defense modernization. Regional dynamics favor North America and Europe for revenue, while Asia‑Pacific leads growth. Strategic emphasis on connectivity, software integration, and sustainability will shape competitive success.

What research methodology was used to compile the Rugged Handheld Devices Market report?

The report employs a mixed‑methods approach combining primary research – interviews with OEM executives, channel partners, and end‑user procurement officers – with secondary research from industry publications, financial filings, government procurement databases, and market intelligence platforms. Data triangulation ensures accuracy, while bottom‑up modeling validates market size, segmentation, and forecast assumptions.

What is the research scope and coverage limitations of the Rugged Handheld Devices Market study?

The study covers the global market for rugged handheld devices across three ruggedness tiers, three product categories, four industry verticals, and five geographic regions. The forecast horizon extends to 2033 with a 2026 baseline. Limitations include reliance on publicly available financial data for private companies, exclusion of consumer‑grade rugged phones, and potential variance in regional certification standards not fully captured.

Who are the key companies and what recent developments have they announced in the Rugged Handheld Devices Market?

Major companies include Zebra Technologies Corporation, Honeywell International Inc., Panasonic Corporation, Getac Technology Corp, Caterpillar Inc., CipherLab Co. Ltd., Handheld Group, Kyocera Corporation, AMREL, and TouchStar Technologies Ltd. Recent activity highlights Zebra’s launch of 5G‑enabled ultra‑rugged tablets, Honeywell’s AI‑powered mobile computer suite, Panasonic’s expanded MIL‑STD‑810H certified lineup, Getac’s strategic partnership with a cloud analytics provider, and Caterpillar’s new rugged phone targeting mining operations.