Europe Data Center Construction Market Overview - Definition, scope, and significance

The Europe Data Center Construction Market encompasses the design, development, and building of facilities that house critical IT infrastructure, including servers, storage systems, networking equipment, and supporting infrastructure. This market covers all aspects of data center construction, from site selection and architectural design to electrical systems, mechanical infrastructure, and general construction services. The significance of this market has grown exponentially as digital transformation accelerates across Europe, with businesses increasingly relying on data centers to support cloud computing, big data analytics, artificial intelligence, and the Internet of Things. The construction of data centers involves complex engineering challenges, including power distribution, cooling systems, security infrastructure, and redundancy requirements, making it a specialized segment within the broader construction industry.

Europe Data Center Construction Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Europe Data Center Construction Market is driven by several key factors, including the rapid adoption of cloud computing services, the proliferation of digital services, and the increasing demand for data storage and processing capabilities. The COVID-19 pandemic has accelerated digital transformation initiatives, creating additional demand for data center infrastructure. However, the market faces restraints such as high capital investment requirements, stringent environmental regulations, and the complexity of construction projects. Challenges include the shortage of skilled labor, rising material costs, and the need to meet strict energy efficiency standards. Opportunities exist in the development of sustainable data centers, the expansion of edge computing facilities, and the integration of renewable energy sources. The market also presents opportunities for innovation in modular construction techniques and the implementation of advanced cooling technologies to improve energy efficiency.

Europe Data Center Construction Market Growth Trends - Current and emerging trends shaping the market

The Europe Data Center Construction Market is experiencing several notable growth trends that are reshaping the industry landscape. One prominent trend is the increasing focus on sustainability and energy efficiency, with data center operators seeking to reduce their carbon footprint through the use of renewable energy sources and innovative cooling technologies. Another significant trend is the rise of edge computing, which is driving the construction of smaller, distributed data centers closer to end-users to reduce latency and improve performance. The market is also witnessing a shift towards modular and prefabricated construction methods, which offer faster deployment times and greater flexibility. Additionally, there is a growing emphasis on data center resilience and security, with Tier 4 facilities becoming increasingly popular among hyperscale operators and enterprise clients. The integration of artificial intelligence and machine learning in data center operations is also influencing construction designs to accommodate advanced monitoring and automation systems.

COVID-19 Impact on the Europe Data Center Construction Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a significant impact on the Europe Data Center Construction Market, initially causing disruptions in supply chains and construction timelines due to lockdowns and social distancing measures. However, the pandemic has ultimately accelerated the demand for data center infrastructure as businesses rapidly shifted to remote work models and increased their reliance on digital services. This unexpected surge in demand has led to a faster recovery trajectory for the market, with many operators fast-tracking their expansion plans to meet the growing need for data processing and storage capabilities. The pandemic has also highlighted the critical importance of data center resilience and redundancy, prompting investments in more robust and geographically diverse infrastructure. As a result, the market is expected to see continued growth in the post-pandemic period, driven by the sustained digital transformation across industries and the increasing adoption of cloud services and edge computing solutions.

Europe Data Center Construction Market Competitive Landscape - Major competitors and market consolidation

The Europe Data Center Construction Market features a diverse competitive landscape with a mix of global construction giants, specialized data center builders, and local contractors. Major players in the market include established construction companies such as STO Building Group Inc and DPR Construction Inc, which have leveraged their extensive experience in large-scale projects to capture significant market share. Specialized data center construction firms like Datalec Precision Installations Ltd and blu-3 (UK) Ltd have carved out niches by focusing exclusively on data center projects, offering deep expertise in the unique requirements of these facilities. The market has also seen increased consolidation, with larger companies acquiring specialized firms to expand their capabilities and geographic reach. This trend towards consolidation is expected to continue as the market matures and competition intensifies. Additionally, technology companies such as Schneider Electric SE are playing an increasingly important role by providing integrated solutions that combine construction services with advanced power and cooling technologies.

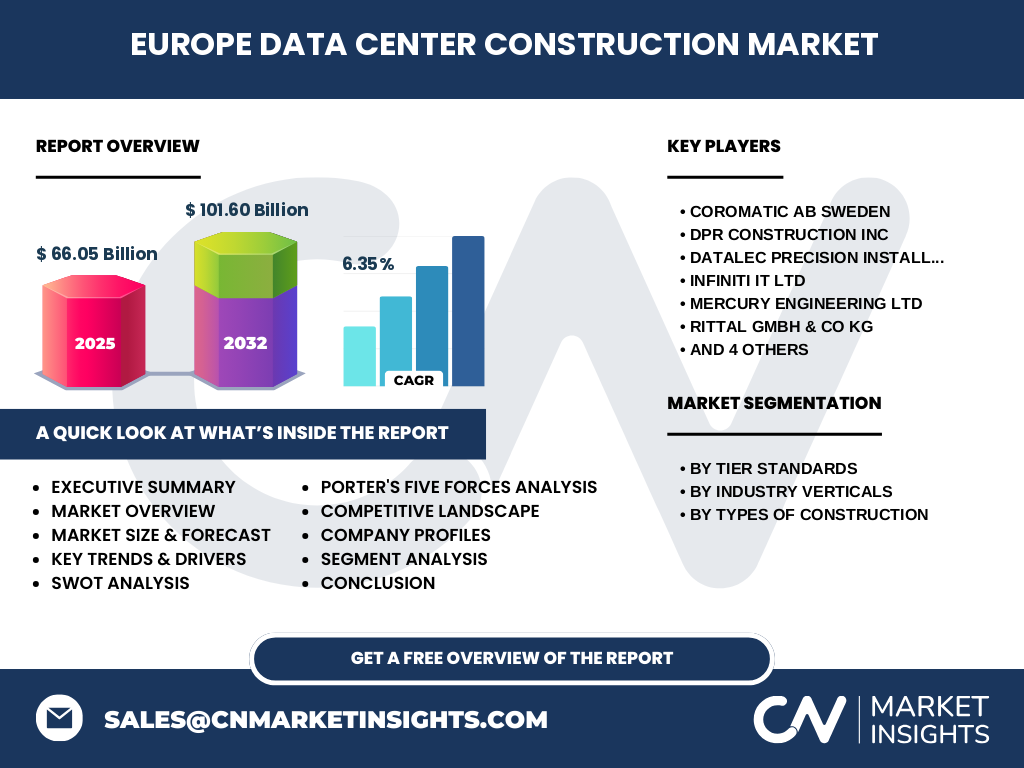

Executive Summary - High-level overview and key findings about Europe Data Center Construction Market

The Europe Data Center Construction Market is experiencing robust growth, driven by the increasing demand for data storage and processing capabilities across various industries. With a market size of €66.05 billion in 2025 and a projected growth to €101.60 billion by 2032, representing a CAGR of 6.35%, the market presents significant opportunities for construction companies and technology providers. The market is segmented by tier standards, industry verticals, and types of construction, offering diverse opportunities for specialized service providers. Key trends shaping the market include the focus on sustainability, the rise of edge computing, and the adoption of modular construction techniques. The competitive landscape is characterized by a mix of global construction giants and specialized data center builders, with ongoing consolidation as the market matures. Despite challenges such as high capital requirements and regulatory complexities, the market's growth trajectory remains strong, driven by the continued digital transformation across Europe and the increasing adoption of cloud services and advanced technologies.

Europe Data Center Construction Market Forecast - Projections for 2025-2032 period

The Europe Data Center Construction Market is poised for significant growth over the forecast period from 2025 to 2032, with projections indicating a substantial increase in market value from €66.05 billion to €101.60 billion. This growth represents a compound annual growth rate (CAGR) of 6.35%, reflecting the strong demand for data center infrastructure across Europe. The forecast period is expected to be characterized by continued investment in both large-scale hyperscale facilities and smaller edge data centers to support the growing needs of cloud service providers, enterprises, and emerging technologies such as 5G and Internet of Things (IoT) applications. The market is likely to see increased focus on sustainability and energy efficiency, driving innovation in construction techniques and technologies. Additionally, the forecast period may witness further consolidation in the industry as larger players seek to expand their capabilities and geographic presence. Regional variations in growth rates are expected, with Western European countries leading in terms of market size, while Eastern European countries may experience faster growth rates due to increasing digitalization and foreign investment in data center infrastructure.

Europe Data Center Construction Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe Data Center Construction Market is segmented by tier standards, industry verticals, and types of construction, each contributing differently to the overall market size and share. In terms of tier standards, Tier 3 data centers, known for their concurrent maintainability and high availability, are expected to dominate the market due to their balance of reliability and cost-effectiveness. However, Tier 4 facilities, offering the highest level of redundancy and fault tolerance, are likely to see increased adoption among hyperscale operators and critical applications. By industry verticals, the IT & Telecommunication sector is projected to hold the largest market share, driven by the rapid expansion of cloud services and telecommunications infrastructure. The BFSI (Banking, Financial Services, and Insurance) sector is also expected to be a significant contributor, given the critical nature of data storage and processing in financial services. In terms of types of construction, electrical construction is likely to account for a substantial portion of the market due to the complex power distribution requirements of modern data centers. Mechanical construction, including cooling systems and HVAC, is also expected to be a significant segment, reflecting the importance of energy efficiency and thermal management in data center design.

Global Europe Data Center Construction Market Size and Share by Region - Geographic distribution

The Europe Data Center Construction Market exhibits significant regional variations in terms of size and share, reflecting the diverse economic landscapes and digital maturity across European countries. Western European countries, particularly the United Kingdom, Germany, France, and the Netherlands, are expected to dominate the market due to their advanced digital infrastructure, high concentration of data center operators, and favorable business environments. These countries are likely to account for the largest share of the market, driven by strong demand from hyperscale cloud providers and enterprise customers. Northern European countries, including Sweden and Finland, are also emerging as significant players in the market, leveraging their cool climates and access to renewable energy sources to attract data center investments. Southern European countries, while currently representing a smaller share of the market, are expected to see increased activity as digital transformation initiatives gain momentum and foreign investment flows into the region. Eastern European countries, such as Poland and Hungary, are projected to experience the fastest growth rates, driven by increasing digitalization, favorable regulatory environments, and lower operational costs compared to Western Europe.

Regional Analysis of the Europe Data Center Construction Market - Detailed regional market performance

The Europe Data Center Construction Market exhibits distinct regional characteristics and performance metrics across different European countries and regions. In Northern Europe, countries like Sweden and Finland are experiencing strong growth in data center construction, driven by their access to renewable energy sources, cool climates that reduce cooling costs, and supportive government policies. These countries are particularly attractive for large-scale, energy-intensive data center projects. Western Europe, led by the United Kingdom, Germany, and the Netherlands, continues to be the dominant region in terms of market size and investment. The presence of major cloud service providers, robust digital infrastructure, and high demand for colocation services contribute to the strong performance in this region. Southern Europe, including countries like Spain and Italy, is seeing increased activity in data center construction as digital transformation initiatives gain traction and foreign investment increases. The region offers advantages such as lower operational costs and strategic geographic positioning for serving Mediterranean and African markets. Eastern Europe, particularly Poland and Hungary, is emerging as a high-growth region for data center construction, driven by increasing digitalization, favorable regulatory environments, and lower costs compared to Western Europe. These countries are attracting significant foreign investment and are becoming important hubs for data center operations serving both local and international markets.

Leading Company Profiles in the Europe Data Center Construction Market - Industry players and strategies

The Europe Data Center Construction Market is characterized by the presence of several leading companies, each employing distinct strategies to capture market share and drive growth. Coromatic AB Sweden has established itself as a key player in the Nordic region, leveraging its expertise in electrical infrastructure and energy solutions to deliver comprehensive data center projects. The company's strategy focuses on providing end-to-end services, from design and construction to operation and maintenance, with a strong emphasis on sustainability and energy efficiency. DPR Construction Inc, a global construction giant, has made significant inroads in the European market by leveraging its extensive experience in complex, mission-critical projects. The company's strategy revolves around innovation and collaboration, utilizing advanced technologies such as Building Information Modeling (BIM) and virtual reality to enhance project delivery and client engagement. Datalec Precision Installations Ltd has carved out a niche as a specialist data center construction firm, focusing on high-density, high-efficiency facilities. Their strategy emphasizes precision engineering and rapid deployment, catering to the needs of hyperscale operators and colocation providers. INFINITI IT Ltd has differentiated itself through its expertise in modular data center solutions, offering flexible and scalable options for clients with varying requirements. The company's strategy centers on providing cost-effective, rapidly deployable solutions that can be easily expanded or relocated as needed. Mercury Engineering Ltd has established a strong presence across Europe through its comprehensive approach to data center construction, offering services ranging from electrical and mechanical installations to building management systems. Their strategy focuses on delivering integrated solutions that optimize performance and energy efficiency. Rittal GmbH & Co KG, while primarily known for its enclosure systems, has expanded its offerings to include complete data center solutions. The company's strategy leverages its expertise in thermal management and infrastructure to provide holistic data center designs. STO Building Group Inc has strengthened its position in the European market through strategic acquisitions and partnerships, expanding its capabilities and geographic reach. Their strategy emphasizes collaboration with technology partners to deliver cutting-edge data center solutions. Schneider Electric SE, a global leader in energy management and automation, has positioned itself as a key player in the data center construction market by offering integrated power, cooling, and software solutions. The company's strategy focuses on sustainability and digital transformation, helping clients optimize their data center operations. Winthrop Technologies Ltd has gained recognition for its expertise in hyperscale data center projects, particularly in the areas of power distribution and critical infrastructure. Their strategy revolves around delivering large-scale, complex projects with a focus on reliability and efficiency. blu-3 (UK) Ltd has established itself as a specialist in precision data center installations, offering services ranging from structured cabling to technical cleaning. The company's strategy emphasizes attention to detail and adherence to strict quality standards, catering to clients with demanding requirements for their data center facilities.

Porter's Five Forces Analysis of the Europe Data Center Construction Market - Competitive forces assessment

The Europe Data Center Construction Market is influenced by several competitive forces as analyzed through Porter's Five Forces framework. The threat of new entrants is moderate, as the market requires significant capital investment, specialized expertise, and established relationships with key clients and suppliers. However, the growing demand for data center infrastructure and the potential for high returns may attract new players, particularly those with strong financial backing or innovative approaches to construction. The bargaining power of buyers is relatively high, given the large-scale nature of data center projects and the availability of multiple construction companies and technology providers. Clients, especially large hyperscale operators, can negotiate favorable terms and push for competitive pricing and innovative solutions. The bargaining power of suppliers is moderate, as the market relies on specialized equipment and materials. While there are several suppliers in the market, the unique requirements of data center construction can limit options and potentially increase supplier power. The threat of substitute products or services is low, as data centers are critical infrastructure with few alternatives for housing IT equipment and supporting digital operations. However, technological advancements in edge computing and modular data centers may present alternative approaches to traditional data center construction. The intensity of competitive rivalry is high, with numerous established players and specialized firms competing for market share. This competition is driving innovation, cost optimization, and the development of unique value propositions among market participants.

SWOT Analysis of the Europe Data Center Construction Market - Strengths, weaknesses, opportunities, threats

The Europe Data Center Construction Market exhibits several strengths, weaknesses, opportunities, and threats as analyzed through a SWOT framework. Strengths of the market include the growing demand for data center infrastructure driven by digital transformation, the presence of established construction companies with specialized expertise, and the increasing focus on sustainability and energy efficiency. The market also benefits from strong government support for digital infrastructure development and the availability of skilled labor in many European countries. However, the market faces weaknesses such as high capital requirements for large-scale projects, complex regulatory environments across different European countries, and potential supply chain disruptions. Opportunities in the market are abundant, including the expansion of edge computing facilities, the integration of renewable energy sources, and the development of innovative construction techniques such as modular and prefabricated solutions. The market also presents opportunities for growth in emerging European markets and the potential for partnerships with technology companies to deliver integrated solutions. Threats to the market include economic uncertainties, geopolitical tensions that may impact cross-border investments, and the potential for rapid technological changes that could render existing infrastructure obsolete. Additionally, the market faces threats from increasing competition, both from established players and new entrants, as well as potential environmental regulations that could increase construction costs and complexity.

Europe Data Center Construction Market Value Chain Analysis - Industry structure and value flow

The Europe Data Center Construction Market value chain encompasses a complex network of activities and stakeholders involved in the design, construction, and operation of data center facilities. At the beginning of the value chain, site selection and feasibility studies are conducted by specialized consultants and engineering firms to identify optimal locations for data center development. This is followed by the architectural and engineering design phase, where detailed plans are created to meet the specific requirements of data center operations, including power distribution, cooling systems, and security infrastructure. The construction phase involves multiple stakeholders, including general contractors, electrical and mechanical subcontractors, and specialized data center builders who bring the designs to life. Throughout the construction process, project management firms play a crucial role in coordinating activities and ensuring timely delivery. The value chain also includes the procurement of specialized equipment and materials from suppliers of servers, networking equipment, power distribution units, and cooling systems. Technology providers, such as Schneider Electric SE, contribute to the value chain by offering integrated solutions that combine hardware and software for data center infrastructure management. Once construction is complete, commissioning and testing services ensure that the facility meets all operational requirements before handover to the client. The value chain extends beyond construction to include ongoing maintenance and support services, which are often provided by the original construction firms or specialized service providers. Additionally, the value chain incorporates sustainability consultants and energy efficiency experts who help optimize the environmental performance of data centers throughout their lifecycle.

Key Investment Insights in the Europe Data Center Construction Market - Strategic investment recommendations

The Europe Data Center Construction Market presents several key investment insights and strategic recommendations for stakeholders looking to capitalize on the growing demand for data center infrastructure. One primary recommendation is to focus on sustainable and energy-efficient construction practices, as environmental concerns and regulatory pressures continue to shape the industry. Investors should consider allocating resources to develop expertise in green building techniques, renewable energy integration, and innovative cooling technologies to meet the evolving needs of environmentally conscious clients. Another strategic insight is the growing importance of edge computing, which presents opportunities for investment in smaller, distributed data center facilities closer to end-users. Investors should consider diversifying their portfolios to include both large-scale hyperscale projects and edge data center developments to capture the full spectrum of market demand. The market also offers opportunities for investment in modular and prefabricated construction techniques, which can significantly reduce deployment times and costs while offering greater flexibility to clients. Strategic partnerships with technology companies and equipment manufacturers can provide a competitive advantage by offering integrated solutions that combine construction expertise with advanced data center technologies. Investors should also consider the potential of emerging European markets, particularly in Eastern Europe, where rapid digitalization and favorable investment climates present significant growth opportunities. Finally, investments in digital tools and technologies, such as Building Information Modeling (BIM) and advanced project management software, can enhance operational efficiency and provide a competitive edge in project delivery and client engagement.

Europe Data Center Construction Market Conclusion - Summary and key takeaways

The Europe Data Center Construction Market is experiencing robust growth, driven by the increasing demand for data storage and processing capabilities across various industries. With a market size of €66.05 billion in 2025 and a projected growth to €101.60 billion by 2032, representing a CAGR of 6.35%, the market presents significant opportunities for construction companies, technology providers, and investors. The market is characterized by a diverse competitive landscape, with a mix of global construction giants and specialized data center builders competing for market share. Key trends shaping the market include the focus on sustainability and energy efficiency, the rise of edge computing, and the adoption of modular construction techniques. The market is segmented by tier standards, industry verticals, and types of construction, offering diverse opportunities for specialized service providers. Despite challenges such as high capital requirements and complex regulatory environments, the market's growth trajectory remains strong, driven by the continued digital transformation across Europe and the increasing adoption of cloud services and advanced technologies. Strategic investments in sustainable construction practices, edge computing facilities, and emerging European markets are likely to yield significant returns as the market continues to evolve and expand.

Research Methodology - How this research was conducted

The research for this Europe Data Center Construction Market report was conducted using a comprehensive methodology that combines primary and secondary research techniques to ensure accuracy and reliability of the findings. Primary research involved interviews with key industry stakeholders, including data center operators, construction companies, technology providers, and industry experts. These interviews provided valuable insights into market trends, challenges, and opportunities, as well as validation of secondary research findings. Secondary research encompassed a thorough analysis of company annual reports, industry publications, market databases, and government statistics to gather quantitative and qualitative data on market size, growth rates, and competitive landscape. The research also included a review of relevant patents, technical papers, and industry forums to identify emerging technologies and innovative construction techniques. Data triangulation was employed to cross-verify information from multiple sources and ensure consistency in the findings. The market size and forecast were derived using a combination of top-down and bottom-up approaches, considering factors such as data center capacity additions, construction costs, and regional demand patterns. The research methodology also incorporated Porter's Five Forces analysis and SWOT analysis to provide a comprehensive understanding of the market dynamics and competitive landscape.

Research Scope - Coverage and limitations

The research scope for this Europe Data Center Construction Market report encompasses a comprehensive analysis of the market across various dimensions, including market size and forecast, segmentation by tier standards, industry verticals, and types of construction, as well as regional analysis covering Western, Northern, Southern, and Eastern Europe. The report covers key market trends, drivers, restraints, challenges, and opportunities, providing insights into the factors shaping the market's growth trajectory. The competitive landscape section profiles major players in the market, offering insights into their strategies and market positioning. The research also includes an analysis of the value chain, investment insights, and strategic recommendations for stakeholders. However, it is important to note certain limitations in the research scope. The report focuses primarily on new construction and major renovation projects, excluding minor upgrades and maintenance activities. Additionally, while the research provides a comprehensive overview of the European market, it may not capture all regional nuances and country-specific regulations in exhaustive detail. The report also does not cover the operational aspects of data centers post-construction, focusing instead on the construction phase and related services. Furthermore, the research is based on available public information and expert opinions, and may not reflect the most recent developments or confidential industry data that may not be publicly accessible.

Key Companies and Recent Developments in the Europe Data Center Construction Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Europe Data Center Construction Market features several key companies that have made significant contributions to the industry through their innovative approaches and strategic developments. Coromatic AB Sweden has recently announced the expansion of its data center construction services to include advanced energy management solutions, leveraging its expertise in electrical infrastructure to offer integrated power and cooling systems. The company has also formed a strategic partnership with a leading renewable energy provider to develop sustainable data center projects across Scandinavia. DPR Construction Inc has made headlines with the launch of its new modular data center construction division, aimed at accelerating deployment times and reducing costs for clients. The company has also announced several high-profile projects in the UK and Germany, solidifying its position as a major player in the European market. Datalec Precision Installations Ltd has recently unveiled its next-generation precision installation techniques, incorporating advanced robotics and AI-driven quality control systems to enhance accuracy and efficiency in data center construction. The company has also expanded its service offerings to include comprehensive testing and commissioning services, providing clients with end-to-end solutions. INFINITI IT Ltd has introduced a new line of modular data center solutions designed for edge computing applications, featuring compact designs and rapid deployment capabilities. The company has also announced a strategic alliance with a major cloud service provider to develop a network of edge data centers across Europe. Mercury Engineering Ltd has recently completed several large-scale hyperscale data center projects in Ireland and the Netherlands, showcasing its expertise in complex, mission-critical infrastructure. The company has also launched a new sustainability initiative aimed at reducing the carbon footprint of its construction projects through the use of renewable energy and energy-efficient technologies. Rittal GmbH & Co KG has introduced an innovative data center cooling solution that combines direct-to-chip liquid cooling with advanced airflow management, significantly improving energy efficiency. The company has also expanded its manufacturing capabilities in Eastern Europe to better serve the growing demand in the region. STO Building Group Inc has announced the acquisition of a specialized data center construction firm in the UK, expanding its capabilities and geographic presence in the European market. The company has also launched a new digital platform for project management and collaboration, enhancing its ability to deliver complex data center projects. Schneider Electric SE has unveiled its latest EcoStruxure for Data Centers solution, integrating power, cooling, and software management systems to optimize data center performance and efficiency. The company has also formed a strategic partnership with a leading AI technology provider to develop intelligent data center management systems. Winthrop Technologies Ltd has recently completed a major hyperscale data center project in Poland, marking its entry into the rapidly growing Eastern European market. The company has also announced plans to expand its operations across Central and Eastern Europe, capitalizing on the region's increasing demand for data center infrastructure. blu-3 (UK) Ltd has introduced a new range of precision installation services for high-density computing environments, incorporating advanced cable management and airflow optimization techniques. The company has also expanded its technical cleaning services to include decontamination and sanitization solutions, addressing the growing need for enhanced data center hygiene in the post-pandemic era.