North America Data Center Construction Market Overview - Definition, scope, and significance

The North America Data Center Construction Market encompasses the planning, design, and physical construction of facilities that house critical IT infrastructure, servers, networking equipment, and storage systems. This market includes all construction activities related to building new data centers as well as expanding or retrofitting existing facilities to meet growing digital demands. The scope covers various construction types including general construction, electrical design, and mechanical design, serving multiple industry verticals such as BFSI, government, education, manufacturing, retail, transportation, and media & entertainment. The significance of this market lies in its fundamental role in supporting the digital economy, cloud computing, artificial intelligence, and the increasing reliance on data-driven technologies across all sectors of the North American economy.

North America Data Center Construction Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the North America Data Center Construction Market include the exponential growth of data consumption, increasing adoption of cloud services, and the proliferation of Internet of Things (IoT) devices. The shift toward digital transformation across industries, coupled with the need for edge computing infrastructure, continues to fuel demand for new data center facilities. However, the market faces several restraints including high capital expenditure requirements, complex regulatory compliance issues, and significant energy consumption concerns. Challenges include skilled labor shortages, supply chain disruptions, and the need for sustainable construction practices. Despite these obstacles, substantial opportunities exist in developing energy-efficient designs, implementing modular construction approaches, and creating specialized facilities for emerging technologies such as 5G networks and artificial intelligence applications.

North America Data Center Construction Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the North America Data Center Construction Market are characterized by the increasing demand for higher-tier facilities, with a notable shift toward Tier 3 and Tier 4 constructions that offer enhanced reliability and redundancy. The market is witnessing a significant trend toward hyperscale data centers, driven by major cloud service providers expanding their infrastructure footprint. Sustainable construction practices are becoming increasingly important, with a focus on energy-efficient designs, renewable energy integration, and achieving carbon neutrality. The adoption of modular and prefabricated construction methods is gaining traction, offering faster deployment times and cost efficiencies. Additionally, the market is experiencing growth in edge data center construction to support low-latency applications and 5G network deployments across urban and suburban areas.

COVID-19 Impact on the North America Data Center Construction Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the North America Data Center Construction Market, initially causing temporary disruptions in supply chains, labor availability, and project timelines. However, the pandemic simultaneously accelerated digital transformation initiatives across all sectors, leading to increased demand for data center capacity to support remote work, online services, and digital commerce. The recovery trajectory has been robust, with the market experiencing renewed momentum as organizations prioritize digital infrastructure investments. The pandemic highlighted the critical importance of resilient and scalable data center infrastructure, leading to increased investment in both new construction and expansion projects. The market has demonstrated strong resilience, with construction activities rebounding and adapting to new health and safety protocols while maintaining project momentum.

North America Data Center Construction Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of the North America Data Center Construction Market is characterized by a mix of large multinational construction firms and specialized data center contractors. Major players such as AECOM, DPR Construction, Inc., and Turner Construction dominate the market with their extensive experience and comprehensive service offerings. The market is witnessing increasing consolidation as larger firms acquire specialized data center construction companies to expand their capabilities and market share. Competition is intensifying based on factors such as technical expertise, project delivery speed, sustainability credentials, and the ability to handle complex, large-scale projects. Companies are differentiating themselves through innovative construction methodologies, advanced design capabilities, and strong partnerships with technology providers and data center operators.

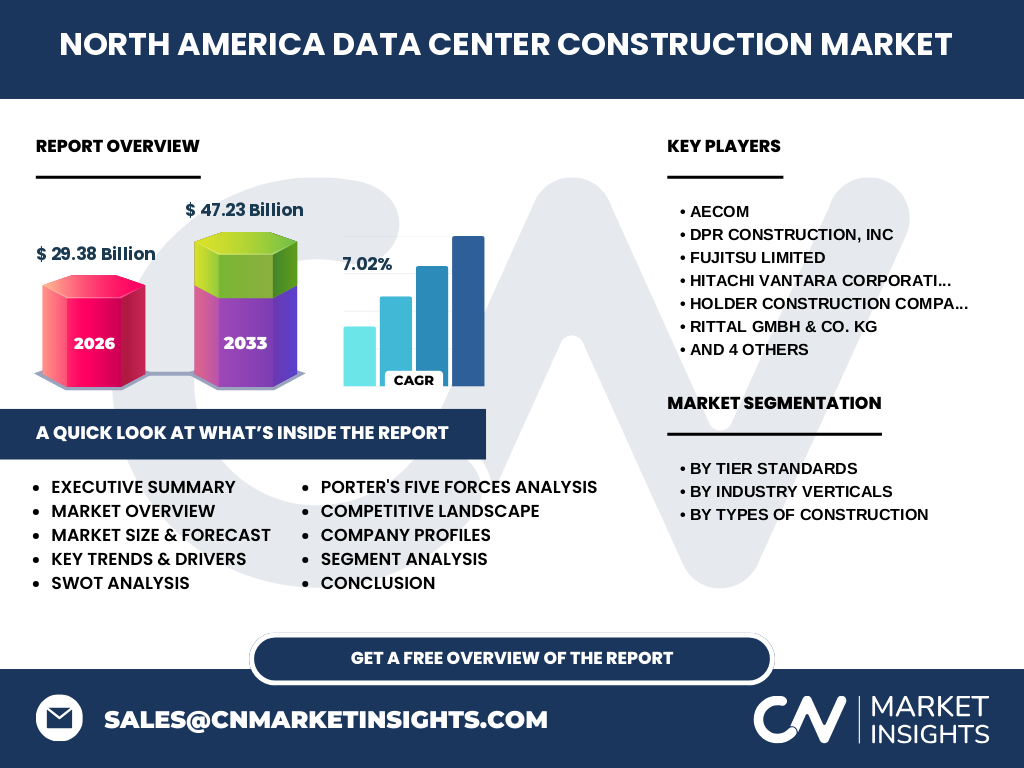

Executive Summary - High-level overview and key findings about North America Data Center Construction Market

The North America Data Center Construction Market is experiencing significant growth, driven by the region's position as a global technology hub and the increasing demand for digital infrastructure. The market is projected to grow from USD 29.38 Billion in 2026 to USD 47.23 Billion by 2033, representing a CAGR of 7.02%. This growth is fueled by the expansion of cloud computing services, the proliferation of data-intensive applications, and the increasing adoption of edge computing solutions. The market is segmented by tier standards, industry verticals, and types of construction, with Tier 3 and Tier 4 facilities, BFSI sector, and general construction leading the demand. Key players are focusing on sustainable construction practices, modular designs, and innovative technologies to maintain their competitive edge in this rapidly evolving market.

North America Data Center Construction Market Forecast - Projections for 2025-2032 period

The North America Data Center Construction Market is projected to experience steady growth throughout the forecast period of 2025-2032, with the market size expected to increase from USD 29.38 Billion in 2026 to USD 47.23 Billion by 2033, representing a compound annual growth rate (CAGR) of 7.02%. This growth trajectory reflects the increasing demand for data center infrastructure driven by cloud adoption, digital transformation initiatives, and the proliferation of data-intensive technologies. The forecast period will likely see continued investment in hyperscale facilities, edge computing infrastructure, and sustainable construction practices. Regional variations in growth rates are expected, with major technology hubs and emerging markets showing particularly strong performance. The market is anticipated to benefit from technological advancements in construction methodologies and increasing focus on energy efficiency and sustainability.

North America Data Center Construction Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America Data Center Construction Market is segmented by tier standards, industry verticals, and types of construction. By tier standards, the market includes Tier 1 and Tier 2, Tier 3, and Tier 4 facilities, with Tier 3 and Tier 4 constructions commanding larger market shares due to their higher reliability and redundancy requirements. In terms of industry verticals, the BFSI sector leads the market, followed by government, education, manufacturing, retail, transportation, and media & entertainment segments. By types of construction, general construction represents the largest segment, followed by electrical design and mechanical design services. This segmentation reflects the diverse requirements of different industries and the varying complexity levels of data center constructions across North America.

Global North America Data Center Construction Market Size and Share by Region - Geographic distribution

The North America Data Center Construction Market exhibits distinct geographic patterns, with the United States dominating the regional market due to its concentration of technology companies, cloud service providers, and major data center hubs. Key states such as Virginia, Texas, and California lead in data center construction activity, driven by favorable business environments, existing infrastructure, and access to renewable energy sources. Canada represents a significant portion of the market, with growth driven by its cold climate advantages for cooling and increasing demand for data center services. Mexico is emerging as an important market, particularly in northern regions, due to its strategic location and growing digital economy. The regional distribution reflects the varying levels of digital maturity, energy costs, and regulatory environments across North America.

Regional Analysis of the North America Data Center Construction Market - Detailed regional market performance

The North America Data Center Construction Market shows varying performance across different regions, with the United States leading in terms of construction activity and investment. The U.S. market is characterized by intense competition among major technology hubs, with regions like Northern Virginia, Silicon Valley, and Dallas-Fort Worth experiencing the highest concentration of data center construction projects. Canada's market is growing steadily, with provinces like Ontario and Quebec attracting significant investment due to their favorable climate conditions and renewable energy resources. The Mexican market, while smaller, is showing promising growth, particularly in regions close to the U.S. border, driven by increasing digital adoption and foreign investment. Regional variations in construction costs, energy prices, and regulatory frameworks significantly influence market dynamics and project feasibility across North America.

Leading Company Profiles in the North America Data Center Construction Market - Industry players and strategies

The North America Data Center Construction Market is served by several prominent companies, each bringing unique strengths and capabilities to the industry. AECOM stands out for its comprehensive engineering and construction services, with a strong focus on sustainable design and innovative construction methodologies. DPR Construction, Inc. is known for its technical expertise in complex data center projects and its commitment to lean construction practices. Fujitsu Limited brings advanced technological solutions and integration capabilities, while Hitachi Vantara Corporation offers expertise in data infrastructure and smart technologies. Holder Construction Company is recognized for its large-scale project management capabilities, and Rittal GmbH & Co. KG specializes in innovative enclosure and infrastructure solutions. Schneider Electric SE leads in energy management and automation solutions, while The Whiting-Turner Contracting Company is known for its extensive experience in mission-critical facilities. Tripp Lite and Turner Construction round out the competitive landscape with their specialized offerings in power protection and comprehensive construction services, respectively.

Porter's Five Forces Analysis of the North America Data Center Construction Market - Competitive forces assessment

The North America Data Center Construction Market exhibits a moderate level of competitive intensity when analyzed through Porter's Five Forces framework. The threat of new entrants is relatively low due to the high capital requirements, technical expertise needed, and established relationships with key clients. However, the bargaining power of buyers is significant, as large technology companies and cloud service providers have substantial influence over pricing and project specifications. The bargaining power of suppliers is moderate, with some specialized equipment and technology providers holding stronger positions. The threat of substitute products or services is low, as data centers are essential infrastructure with no direct alternatives. Competitive rivalry is high among established players, driving innovation in construction methods, sustainability practices, and project delivery efficiency. The market's growth potential and technological complexity continue to shape the competitive dynamics among industry participants.

SWOT Analysis of the North America Data Center Construction Market - Strengths, weaknesses, opportunities, threats

The North America Data Center Construction Market demonstrates several key strengths, including advanced technological capabilities, a robust ecosystem of suppliers and service providers, and strong demand from diverse industry verticals. The region's leadership in cloud computing and digital innovation provides a solid foundation for market growth. However, weaknesses exist in the form of high construction costs, complex regulatory environments, and challenges in sourcing skilled labor. Significant opportunities are present in the form of growing demand for edge computing facilities, increasing focus on sustainable construction practices, and the potential for modular and prefabricated construction methods. Threats to the market include potential economic downturns, supply chain disruptions, and increasing competition from international markets. The market's ability to address these factors while capitalizing on emerging trends will be crucial for sustained growth and success.

North America Data Center Construction Market Value Chain Analysis - Industry structure and value flow

The value chain in the North America Data Center Construction Market is complex and multifaceted, involving various stakeholders from initial planning through project completion and ongoing maintenance. The chain begins with technology providers and consultants who assess client needs and develop project specifications. This is followed by architectural and engineering firms that design the facilities, taking into account technical requirements, sustainability goals, and local regulations. Construction companies then execute the building phase, coordinating with specialized subcontractors for electrical, mechanical, and networking installations. Equipment manufacturers and suppliers provide critical components such as servers, cooling systems, and power distribution units. Throughout this process, project management firms and general contractors oversee the integration of various elements. The value flow continues post-construction with maintenance and upgrade services, creating ongoing revenue streams and long-term client relationships.

Key Investment Insights in the North America Data Center Construction Market - Strategic investment recommendations

Strategic investment in the North America Data Center Construction Market should focus on several key areas to maximize returns and capitalize on market growth. Investors should consider opportunities in sustainable construction technologies and energy-efficient designs, as environmental concerns and operational costs continue to drive industry priorities. The growing demand for edge computing infrastructure presents significant investment potential, particularly in underserved markets and regions with high data consumption. Modular and prefabricated construction methods offer opportunities for cost reduction and faster project delivery, making them attractive investment targets. Additionally, investments in advanced cooling technologies, renewable energy integration, and smart building management systems are likely to yield strong returns as the industry prioritizes efficiency and sustainability. Partnerships with established construction firms and technology providers can provide strategic advantages and access to key markets and expertise.

North America Data Center Construction Market Conclusion - Summary and key takeaways

The North America Data Center Construction Market is positioned for substantial growth, driven by the region's digital transformation, increasing data consumption, and the proliferation of cloud services and edge computing. The market's projected growth from USD 29.38 Billion in 2026 to USD 47.23 Billion by 2033, at a CAGR of 7.02%, reflects the critical importance of data center infrastructure in supporting the modern digital economy. Key trends such as the shift toward higher-tier facilities, sustainable construction practices, and modular design approaches are shaping the market's evolution. While challenges exist in terms of costs, regulations, and skilled labor, the opportunities presented by emerging technologies and increasing demand across various industry verticals provide a strong foundation for continued market expansion. Success in this market will depend on companies' ability to innovate, adapt to changing technologies, and address sustainability concerns while meeting the growing demand for reliable and efficient data center infrastructure.

Research Methodology - How this research was conducted

The research methodology for this North America Data Center Construction Market analysis involved a comprehensive approach combining primary and secondary research techniques. Primary research included interviews with industry experts, construction companies, data center operators, and technology providers to gather firsthand insights into market trends, challenges, and opportunities. Secondary research encompassed extensive review of industry reports, company financial statements, regulatory documents, and trade publications to validate and supplement primary findings. Market size and forecast calculations were derived using both top-down and bottom-up approaches, considering factors such as construction spending, industry vertical growth rates, and technological adoption trends. Data triangulation was employed to ensure accuracy and reliability of the findings. The research also incorporated analysis of historical market performance, current market dynamics, and future growth projections to provide a comprehensive view of the North America Data Center Construction Market.

Research Scope - Coverage and limitations

The research scope for this North America Data Center Construction Market report encompasses the entire North American region, including the United States, Canada, and Mexico. The analysis covers various aspects of the market, including construction types, tier standards, industry verticals, and geographic distribution. The timeframe considered includes historical data, current market conditions, and future projections up to 2033. However, the research has certain limitations, primarily related to the availability of granular data at the country level within North America and the rapidly evolving nature of technology and construction methodologies in the data center industry. Additionally, the impact of unforeseen global events or regulatory changes may affect market dynamics in ways that are difficult to predict. Despite these limitations, the research provides a comprehensive overview of the market, supported by extensive data analysis and expert insights.

Key Companies and Recent Developments in the North America Data Center Construction Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North America Data Center Construction Market is characterized by active participation from key industry players who are continuously innovating and expanding their capabilities. AECOM has recently announced several large-scale data center projects, focusing on sustainable design and modular construction approaches. DPR Construction, Inc. has launched new initiatives in lean construction methodologies and has formed strategic partnerships with major cloud service providers to enhance its market position. Fujitsu Limited has introduced advanced cooling solutions and energy-efficient technologies for data center applications, while Hitachi Vantara Corporation has expanded its portfolio of smart data center solutions through recent acquisitions and product launches. Holder Construction Company has announced several hyperscale data center projects, emphasizing rapid deployment capabilities. Rittal GmbH & Co. KG has introduced innovative enclosure systems designed for high-density computing environments. Schneider Electric SE has launched new energy management solutions and formed partnerships to advance sustainable data center practices. The Whiting-Turner Contracting Company has expanded its presence in key data center markets through strategic acquisitions. Tripp Lite has introduced new power protection solutions, and Turner Construction has announced several large-scale data center projects focusing on advanced cooling and energy efficiency technologies.