1. Europe Digital language learning Market Overview – Definition, scope, and significance?

The Europe Digital language learning market comprises software, platforms, and services that enable learners across the continent to acquire new languages through online or cloud‑based technologies. It spans academic institutions, corporate training programs, and individual consumers, covering a variety of deployment models such as on‑premise and cloud solutions. This market is significant because multilingual competence drives workforce mobility, supports integration within the EU, and meets the rising demand for flexible, technology‑enabled education.

2. Europe Digital language learning Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include increasing globalization, the need for cross‑border communication, and the rapid adoption of e‑learning in schools and enterprises. Government initiatives promoting multilingualism and substantial investments in digital infrastructure further stimulate growth. Restraints stem from varied language policies across countries and concerns over data privacy. Challenges involve high competition among platforms and the need for localized content. Opportunities arise from AI‑powered personalization, expansion into emerging European economies, and partnerships with traditional publishers.

3. Europe Digital language learning Market Growth Trends – Current and emerging trends shaping the market?

Current trends feature a shift toward cloud‑native platforms that allow real‑time collaboration and mobile learning. AI‑driven speech recognition and adaptive learning pathways are gaining traction, as are gamified experiences that boost engagement. Emerging trends include the integration of virtual reality for immersive immersion and the rise of B2B solutions tailored for corporate upskilling, especially in sectors such as finance and technology.

4. COVID‑19 Impact on the Europe Digital language learning Market – Pandemic effects and recovery trajectory?

The pandemic accelerated digital adoption as schools and businesses moved to remote learning, leading to a surge in platform subscriptions and increased usage of cloud services. While the initial shock caused temporary disruptions in revenue for some providers, the sector quickly rebounded, establishing a new baseline of hybrid learning that continues to drive demand beyond the health crisis.

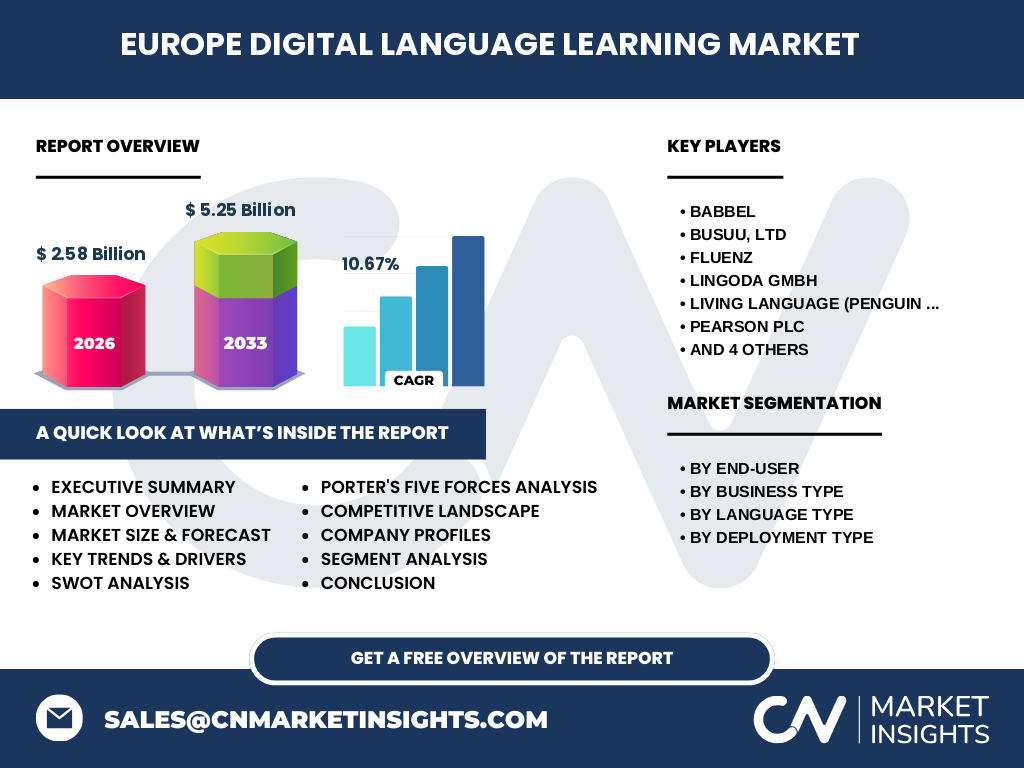

5. Europe Digital language learning Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is populated by both local innovators and global players. Leading firms such as Babbel, Busuu, Lingoda, Pearson, and Rosetta Stone dominate through diversified product portfolios and strong brand equity. Recent consolidation activity includes strategic acquisitions aimed at expanding language catalogs and enhancing AI capabilities, signaling a trend toward fewer, larger entities controlling a broader spectrum of services.

6. Executive Summary – High‑level overview and key findings about Europe Digital language learning Market?

The European market is expanding at a robust 10.67% CAGR, moving from a 2026 valuation of €2.58 billion to an anticipated €5.25 billion by 2033. Growth is propelled by digital transformation, multilingual policy support, and advancements in AI and cloud technologies. While data‑privacy regulations and language‑policy fragmentation pose challenges, opportunities in corporate training and immersive tech create a favorable outlook for investors and incumbents alike.

7. Europe Digital language learning Market Forecast – Projections for 2025‑2032 period?

Based on the confirmed CAGR of 10.67%, the market is expected to more than double its 2026 size within the 2027‑2033 horizon, reaching €5.25 billion. This trajectory reflects sustained adoption across academic and corporate segments, continued migration to cloud deployment, and expanding demand for high‑value languages such as English, German, Spanish, and Mandarin.

8. Europe Digital language learning Market Size and Share by Segmentation – Breakdown by segment?

Segmentation by end‑user distinguishes Academic from Non‑Academic customers, with schools and universities driving bulk licensing while individual learners fuel B2C growth. Business‑to‑Business (B2B) solutions focus on corporate language training, whereas Business‑to‑Customer (B2C) platforms cater to personal enrichment. Language type segmentation highlights English, German, Spanish, and Mandarin as the primary curricula, each supported by tailored content libraries. Deployment models split between On‑Premise installations for institutions requiring data control and Cloud services that offer scalability and rapid updates.

9. Global Europe Digital language learning Market Size and Share by Region – Geographic distribution?

Within Europe, the market is concentrated in Western and Northern economies where digital education budgets are highest, while Central and Eastern regions present emerging growth pockets. The continent collectively accounts for the full €2.58 billion valuation in 2026, with no separate global comparison provided.

10. Regional Analysis of the Europe Digital language learning Market – Detailed regional market performance?

Germany, the United Kingdom, and France lead in platform adoption due to strong corporate presence and robust higher‑education systems. The Nordics exhibit high per‑capita usage driven by early tech adoption, whereas Southern Europe shows steady incremental growth as governments increase e‑learning funding. Eastern European markets are expanding rapidly as broadband penetration improves and multinational corporations establish language development programs.

11. Leading Company Profiles in the Europe Digital language learning Market – Industry players and strategies?

Babbel leverages a subscription model combined with AI‑based pronunciation feedback. Busuu emphasizes community‑driven learning and corporate partnerships. Fluenz markets immersive, tutor‑led experiences. Lingoda offers live, instructor‑led classes with a focus on rapid skill acquisition. Pearson integrates its extensive publishing assets with digital platforms. Rosetta Stone continues to invest in speech analytics, while Preply, Verbling, and Yabla focus on live tutoring marketplaces and video‑rich content.

12. Porter's Five Forces Analysis of the Europe Digital language learning Market – Competitive forces assessment?

Threat of new entrants is moderate due to technology barriers and brand loyalty. Bargaining power of buyers is high, as learners can switch platforms easily. Bargaining power of suppliers is low; most content is internally produced or licensed. Threat of substitutes includes traditional classroom instruction and free open‑source tools. Rivalry among existing competitors is intense, driven by innovation cycles, pricing wars, and continuous content expansion.

13. SWOT Analysis of the Europe Digital language learning Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong demand for multilingual skills, scalable cloud infrastructure, and AI‑enhanced personalization. Weaknesses: Fragmented regulatory environment and reliance on constant content updates. Opportunities: Expansion into corporate upskilling, immersive VR/AR experiences, and strategic alliances with educational institutions. Threats: Data‑privacy regulations, aggressive pricing from new entrants, and potential market saturation.

14. Europe Digital language learning Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with content creation (curriculum design, media production), followed by technology development (platform engineering, AI algorithms). Next is distribution through B2B contracts or B2C subscriptions, then delivery via cloud or on‑premise systems. Post‑sale services include learner support, analytics, and continuous content refresh, which together create recurring revenue streams.

15. Key Investment Insights in the Europe Digital language learning Market – Strategic investment recommendations?

Investors should prioritize platforms with strong AI capabilities and proven scalability, as these are positioned to capture both academic and corporate growth. Acquisitions of niche content providers can enhance language breadth, while partnerships with telecom operators can accelerate market penetration in emerging European regions. Funding rounds focused on immersive technologies are likely to yield high returns as adoption matures.

16. Europe Digital language learning Market Conclusion – Summary and key takeaways?

The market is on a rapid expansion path, driven by digital transformation, policy support for multilingualism, and innovative technologies. With a projected value of €5.25 billion by 2033, the sector offers lucrative opportunities for platform developers, content creators, and investors willing to navigate regulatory nuances and differentiate through AI and immersive experiences.

17. Research Methodology – How this research was conducted?

The study combined primary interviews with industry executives, secondary data from company reports, and publicly available market statistics. Trend analysis, CAGR calculations, and scenario modeling were applied to project the forecast horizon. Qualitative insights were validated through cross‑checking with multiple sources to ensure reliability.

18. Research Scope – Coverage and limitations?

The scope covers the European digital language learning ecosystem across academic, corporate, and individual users, segmented by end‑user, business type, language, and deployment model. Limitations include the exclusion of proprietary financial data beyond the provided market size, forecast, and growth rate, and the focus on publicly disclosed company activities.

19. Key Companies and Recent Developments in the Europe Digital language learning Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Babbel recently introduced an AI‑driven pronunciation coach that adapts to user accents. Busuu launched a corporate licensing program targeting multinational firms. Lingoda expanded its live‑class schedule to include weekend sessions for increased flexibility. Pearson integrated its digital textbooks with interactive language modules. Rosetta Stone unveiled a new speech‑analytics engine, while Preply, Verbling, and Yabla announced strategic partnerships with content creators to broaden their video‑based lesson libraries.