What is the Aircraft Computers Market Overview – definition, scope, and significance?

The Aircraft Computers Market comprises the design, development, production, and servicing of electronic computing systems that control and monitor flight operations, engine performance, navigation, mission functions, and passenger services. Its scope covers hardware and software solutions for fixed‑wing, rotary‑wing, and unmanned aerial vehicles, as well as line‑fit and retrofit installations. These systems are critical for aircraft safety, efficiency, and compliance with increasingly stringent avionics regulations, making the market a cornerstone of modern aerospace technology.

What are the key drivers, restraints, challenges, and opportunities shaping the Aircraft Computers Market?

Growth is driven by rising air traffic, the need for advanced flight‑control automation, and expanding demand for in‑flight entertainment and connectivity. Digital transformation and the shift toward software‑defined avionics create opportunities for higher‑margin services and upgrades. Restraints include high certification costs and supply‑chain volatility for semiconductor components. Challenges involve maintaining cybersecurity and integrating legacy hardware, while opportunities arise from retrofitting older fleets and the proliferation of unmanned aerial systems.

What are the current growth trends in the Aircraft Computers Market?

Emerging trends include the adoption of integrated modular avionics, increased use of AI for predictive maintenance, and the migration to solid‑state avionics that reduce weight and improve reliability. Manufacturers are also focusing on line‑fit solutions that enable faster delivery to OEMs, while retrofit programs are gaining traction to extend the service life of existing aircraft. The rise of UAVs adds a new platform segment with specific computing requirements.

How has COVID‑19 impacted the Aircraft Computers Market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in new aircraft deliveries and a pause in retrofit projects, reducing short‑term demand for avionics upgrades. However, once passenger volumes began to recover, airlines accelerated modernization plans to improve operational efficiency and passenger experience. The market is now on a clear upside path, supported by renewed investment in fleet renewal and the strengthening of cargo and UAV operations.

Who are the major competitors in the Aircraft Computers Market and what is the state of market consolidation?

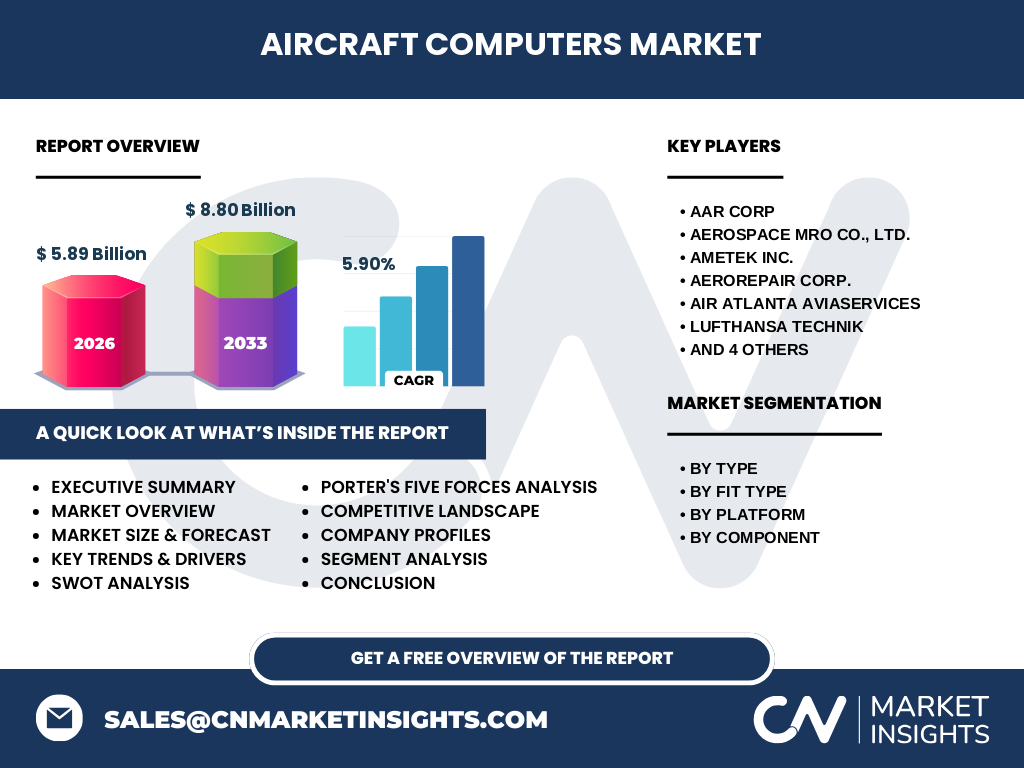

Key players include AAR Corp, AEROSPACE MRO Co., Ltd., AMETEK Inc., AeroRepair Corp., Air Atlanta Aviaservices, Lufthansa Technik, Râder Präzision GmbH, TP Aerospace, Technic Aviation, and World Aero. The competitive landscape features a mix of traditional aerospace firms and specialized avionics suppliers. Recent M&A activity has focused on acquiring niche software capabilities and expanding service networks, indicating gradual consolidation around integrated hardware‑software offerings.

What are the high‑level findings in the Executive Summary of the Aircraft Computers Market?

The market is valued at USD 5.89 billion in 2026 and is projected to reach USD 8.80 billion by 2033, reflecting a CAGR of 5.90 % over the forecast period. Growth is underpinned by strong demand for advanced flight‑control and mission computers across all aircraft platforms. Software innovation, retrofit momentum, and UAV expansion are identified as primary value drivers, while certification costs remain a notable barrier.

What is the forecast for the Aircraft Computers Market from 2025 to 2032?

Based on the given CAGR of 5.90 %, the market is expected to continue expanding steadily, moving from a 2026 base of USD 5.89 billion to around USD 8.80 billion by 2033. This trajectory suggests consistent annual growth, with the most pronounced increases likely in the UAV and retrofit segments, where demand for cost‑effective upgrades is accelerating.

How is the Aircraft Computers Market sized and shared by segmentation?

Segmentation by type includes Flight Controls, Utility Controls & IFE Systems, Engine Controls, Mission Computers, and Flight Management Computers. By fit type, the market is divided into Line Fit and Retrofit solutions. Platform segmentation covers Fixed‑Wing Aircraft, Rotary‑Wing Aircraft, and Unmanned Aerial Vehicles, while component segmentation separates Hardware from Software. Each segment contributes to the overall market value, with Flight Controls and Flight Management Computers representing the largest hardware categories, and Software driving higher margin growth.

What is the global Aircraft Computers Market size and share by region?

The market is distributed across major aerospace regions, including North America, Europe, Asia‑Pacific, and the Rest of the World. While specific regional dollar values are not disclosed, North America and Europe hold substantial shares due to mature OEM bases, whereas Asia‑Pacific is emerging rapidly thanks to expanding commercial fleets and UAV programs.

What does the regional analysis reveal about Aircraft Computers market performance?

North America continues to lead in high‑value line‑fit contracts and advanced mission‑computer deployments for defense platforms. Europe maintains strength through legacy retrofit programs and strong regulatory frameworks. Asia‑Pacific is experiencing the fastest growth, driven by new aircraft orders, rising low‑cost carrier activity, and government‑backed UAV initiatives. The Rest of the World shows modest but steady adoption, primarily in regional airline fleets.

Which companies lead the Aircraft Computers Market and what are their strategic approaches?

Leaders such as AAR Corp and Lufthansa Technik focus on full‑service life‑cycle support, combining hardware supply with aftermarket upgrades. AMETEK leverages its semiconductor expertise to provide high‑reliability processor modules. Regional specialists like TP Aerospace and World Aero concentrate on niche retrofit solutions for specific aircraft types. Across the board, firms are investing in software platforms, digital twins, and collaborative R&D to stay competitive.

How does Porter’s Five Forces model apply to the Aircraft Computers Market?

Threat of new entrants is moderate due to high certification barriers. Bargaining power of suppliers is high, especially for specialty semiconductors. Bargaining power of buyers is moderate; airlines and OEMs demand cost‑effective, reliable solutions but have limited alternatives. Threat of substitutes is low, as few technologies can replace dedicated avionics computers. Industry rivalry is intense, driven by innovation cycles and service differentiation.

What are the SWOT insights for the Aircraft Computers Market?

Strengths: Critical safety role, strong demand for upgrades, high entry barriers.

Weaknesses: Long development timelines, dependence on regulated certification.

Opportunities: UAV growth, software‑defined avionics, retrofit market expansion.

Threats: Supply chain disruptions, cybersecurity risks, escalating R&D costs.

How is the value chain structured in the Aircraft Computers Market?

The value chain begins with R&D and design, followed by component sourcing (semiconductors, sensors), system integration, testing, and certification. Production includes both hardware assembly and software development. Distribution occurs via OEM contracts or direct line‑fit sales, while aftermarket services—maintenance, upgrades, and retrofits—provide recurring revenue. Service providers and MRO firms add value through installation and lifecycle support.

What key investment insights can be drawn for the Aircraft Computers Market?

Investors should target companies with strong software portfolios and retrofit capabilities, as these segments promise higher margins and repeat business. Partnerships with UAV developers and participation in government‑funded digital‑avionics programs can accelerate growth. Monitoring semiconductor supply dynamics and cybersecurity certifications will be essential for risk management.

What is the overall conclusion of the Aircraft Computers Market analysis?

The Aircraft Computers Market is on a robust growth path, underpinned by a 5.90 % CAGR and a projected increase to USD 8.80 billion by 2033. Technological advancement, fleet modernization, and the rise of UAVs create a fertile environment for both hardware and software innovators. While certification and supply‑chain challenges persist, the market’s strategic importance to aviation safety and efficiency ensures sustained investment and expansion.

What research methodology was employed for this market study?

The study combined primary interviews with industry executives, secondary data from aerospace publications, and financial filings of key players. Trend analysis, CAGR calculations, and segmentation modeling were applied using the verified market size of USD 5.89 billion (2026) and the forecasted USD 8.80 billion (2033). Qualitative insights were cross‑validated through expert panels.

What is the scope of this Aircraft Computers Market research?

The research covers global aircraft computers across all major platforms—fixed‑wing, rotary‑wing, and UAVs—segmented by type, fit, platform, and component. It includes market size, forecast, competitive landscape, and strategic analyses. Geographic coverage spans North America, Europe, Asia‑Pacific, and the Rest of the World, focusing on commercial, military, and aftermarket segments.

Which key companies have recent developments in the Aircraft Computers Market?

Recent announcements include AAR Corp’s expansion of retrofit services for legacy fleets, AMETEK’s launch of a new radiation‑hardened processor, Lufthansa Technik’s partnership with a software firm to deliver AI‑based maintenance analytics, and TP Aerospace’s certification of a compact flight‑control computer for UAVs. These developments highlight ongoing innovation and strategic collaborations aimed at capturing emerging market opportunities.