Europe PACS and RIS Market Overview - Definition, scope, and significance?

The Europe Picture Archiving and Communication System (PACS) and Radiology Information System (RIS) market encompasses solutions that digitise, store, retrieve, and manage medical imaging and related workflow data across the continent. PACS handles the acquisition, archiving, and distribution of images, while RIS manages patient scheduling, reporting, and billing. The market’s scope includes hardware, software, and services delivered to hospitals, diagnostic centres, and research & academic institutes through on‑premise, cloud‑based, or web‑based deployments. Its significance lies in enabling faster diagnosis, improving patient outcomes, reducing radiology costs, and supporting regulatory compliance with EU health data standards.

Europe PACS and RIS Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising imaging volumes driven by an ageing population, increasing prevalence of chronic diseases, and government initiatives promoting digital health. Reimbursement reforms and the need for interoperable systems further stimulate adoption. Restraints involve high upfront capital expenditure for hardware and integration complexities with legacy IT infrastructure. Challenges stem from stringent data‑privacy regulations (GDPR) and the shortage of skilled IT staff in healthcare. Opportunities arise from the growth of AI‑enabled diagnostic tools, demand for cloud‑based solutions that lower total cost of ownership, and expanding tele‑radiology services across remote European regions.

Europe PACS and RIS Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady shift from on‑premise installations toward hybrid cloud models, offering scalability and disaster‑recovery benefits. AI integration for automated image analysis and workflow optimisation is gaining momentum, particularly in larger hospital networks. Vendors are bundling PACS/RIS with enterprise imaging platforms to provide end‑to‑end solutions. Additionally, the adoption of vendor‑neutral archives (VNA) is increasing, facilitating data exchange across heterogeneous systems. Emerging trends include the use of blockchain for secure image provenance and the rollout of 5G networks that enable high‑resolution image streaming for mobile diagnostics.

COVID-19 Impact on the Europe PACS and RIS Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated digital transformation in healthcare. Lockdowns and the need for remote reporting pushed hospitals to adopt web‑based and cloud‑based PACS/RIS solutions. Imaging demand surged for chest CT and X‑ray scans, prompting short‑term capacity expansions. Although elective procedures declined initially, the market rebounded quickly as healthcare facilities resumed routine services. Recovery is now characterised by sustained investment in tele‑radiology, enhanced AI diagnostics for pandemic‑related imaging, and a stronger emphasis on resilient, cloud‑centric architectures.

Europe PACS and RIS Market Competitive Landscape - Major competitors and market consolidation?

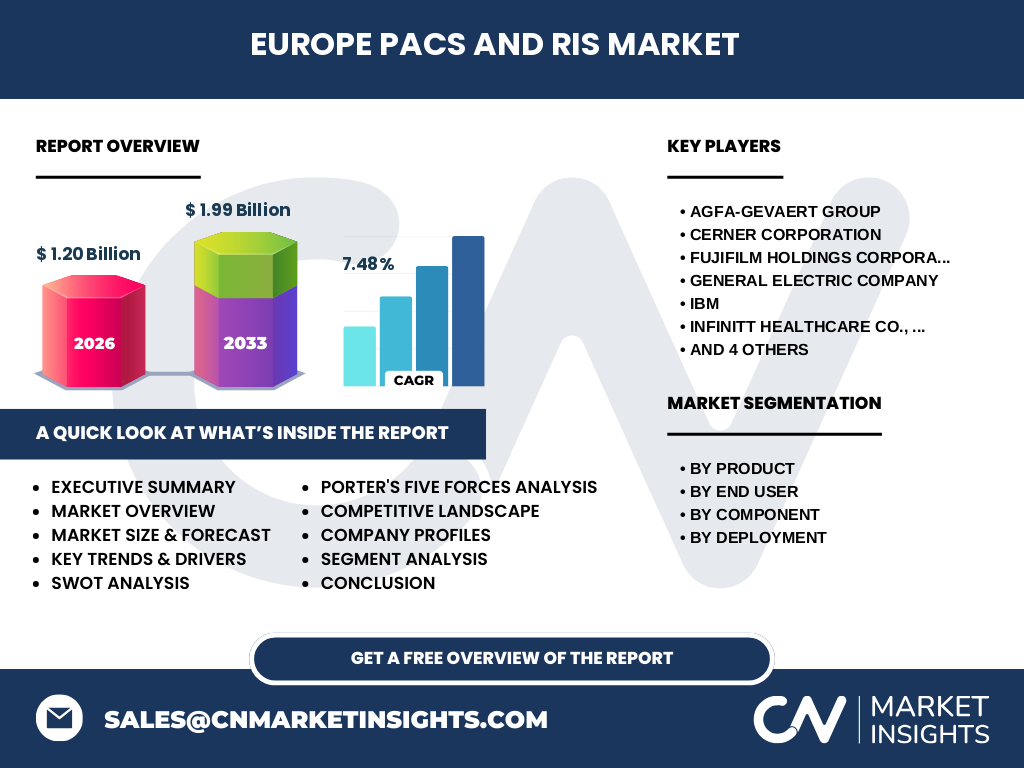

The competitive landscape is fragmented, with several multinational players vying for market share. Leading firms such as Agfa‑Gevaert Group, Cerner Corporation, FUJIFILM Holdings, General Electric Company, IBM, INFINITT Healthcare, Koninklijke Philips N.V., McKesson Corporation, Novarad, and Siemens AG dominate through comprehensive product portfolios and strong distribution networks. Recent years have seen strategic acquisitions—particularly of niche AI start‑ups and cloud service providers—aimed at bolstering software capabilities and expanding service offerings, leading to modest consolidation within the segment.

Executive Summary - High-level overview and key findings about Europe PACS and RIS Market?

The Europe PACS and RIS market is valued at €1.20 billion in 2026 and is projected to reach €1.99 billion by 2033, reflecting a robust CAGR of 7.48 %. Growth is driven by demographic shifts, regulatory support for digital health, and the rapid adoption of cloud and AI technologies. While capital costs and data‑privacy compliance pose challenges, opportunities in tele‑radiology and AI‑enhanced diagnostics present strong upside. The market remains competitive, with ten major vendors leading innovation and consolidation activities. Stakeholders are encouraged to monitor cloud migration trends and AI integration as primary levers for competitive advantage.

Europe PACS and RIS Market Forecast - Projections for 2025-2032 period?

Based on the established CAGR of 7.48 %, the market is expected to continue expanding steadily through 2032. By 2027 the market size will approach €1.45 billion, rising to approximately €1.99 billion by 2033. The forecast reflects ongoing investments in cloud infrastructures, growing AI‑driven workflow solutions, and increased procurement by both public and private hospital networks across the EU. The trajectory suggests a compound increase of roughly €200‑million per year, indicating healthy demand across all major segments.

Europe PACS and RIS Market Size and Share by Segmentation - Breakdown by segment?

Segmentation is defined by product type, end‑user, component, and deployment model. By product, the market is split evenly between PACS and RIS solutions. End‑user distribution shows hospitals as the largest consumer, followed by diagnostic centres and research/academic institutes. Component‑wise, software accounts for the highest share due to recurring licensing and AI add‑ons, while hardware and services complete the mix. Deployment preferences are shifting, with web‑based and cloud‑based offerings gaining ground over traditional on‑premise installations.

Global Europe PACS and RIS Market Size and Share by Region - Geographic distribution?

Within Europe, market activity is concentrated in Western and Northern European nations—Germany, France, the United Kingdom, the Netherlands, and the Scandinavian countries—driven by advanced healthcare systems and higher IT budgets. Southern and Eastern European countries are emerging markets, showing accelerated uptake of cloud‑based solutions as they modernise legacy infrastructures. The overall European share remains the dominant portion of the global PACS/RIS landscape, reflecting strong regulatory support for digital imaging across the continent.

Regional Analysis of the Europe PACS and RIS Market - Detailed regional market performance?

Germany leads in absolute value, attributable to extensive hospital networks and early AI adoption. France follows with significant public‑sector investment in interoperable imaging platforms. The United Kingdom shows rapid migration to cloud services, spurred by NHS digital transformation programmes. The Benelux region benefits from high per‑capita healthcare spending, while the Nordics excel in tele‑radiology deployment. Eastern European markets such as Poland and the Czech Republic are poised for growth as they upgrade legacy systems and seek cost‑effective cloud alternatives.

Leading Company Profiles in the Europe PACS and RIS Market - Industry players and strategies?

Agfa‑Gevaert Group focuses on integrated imaging workflows and VNA solutions, leveraging its strong European brand. Cerner Corporation emphasizes cloud‑native platforms and data analytics. FUJIFILM Holdings offers high‑resolution imaging hardware paired with AI diagnostics. General Electric Company combines hardware expertise with advanced software analytics. IBM provides AI‑driven imaging analytics and hybrid cloud services. INFINITT Healthcare specializes in RIS and PACS interoperability. Koninklijke Philips N.V. integrates imaging with patient monitoring systems. McKesson Corporation drives service‑orientation and procurement efficiencies. Novarad delivers flexible, modular PACS/RIS suites. Siemens AG combines imaging hardware with next‑generation AI tools. Most players pursue partnerships with AI start‑ups and cloud providers to broaden their value proposition.

Porter's Five Forces Analysis of the Europe PACS and RIS Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and regulatory barriers deter newcomers, yet cloud platforms lower entry thresholds. Bargaining power of buyers is strong, as large hospital groups can negotiate pricing and demand integrated solutions. Bargaining power of suppliers is moderate; hardware component suppliers have some leverage, but software vendors can switch platforms. Threat of substitutes is low; alternative imaging management tools lack the comprehensive functionality of PACS/RIS. Rivalry among existing firms is intense, driven by innovation in AI, cloud services, and strategic acquisitions.

SWOT Analysis of the Europe PACS and RIS Market - Strengths, weaknesses, opportunities, threats?

Strengths: Mature regulatory environment, high clinical adoption, strong vendor ecosystem, and clear ROI from workflow efficiency. Weaknesses: High upfront costs, integration complexity with legacy systems, and fragmented standards across vendors. Opportunities: Expansion of AI‑enabled diagnostics, growth of tele‑radiology, migration to subscription‑based cloud models, and emerging markets in Eastern Europe. Threats: Data‑privacy compliance costs, potential cyber‑security breaches, and slowing public‑sector budgets amidst economic pressures.

Europe PACS and RIS Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component manufacturers (hardware, semiconductor, storage). Next, software developers create PACS/RIS platforms, often integrating AI algorithms. System integrators then customise solutions for end‑users, providing installation, training, and support services. Hospitals and diagnostic centres purchase licences or subscriptions, generating recurring revenue streams. Ongoing services—maintenance, upgrades, and cloud hosting—represent the post‑sale value creation, while feedback loops drive continuous product improvement.

Key Investment Insights in the Europe PACS and RIS Market - Strategic investment recommendations?

Investors should target vendors with strong cloud portfolios and AI capabilities, as these segments exhibit the fastest growth. Partnerships with European cloud providers can accelerate market penetration while ensuring GDPR compliance. Acquisitions of niche AI firms or VNA specialists offer synergistic value. Additionally, funds directed toward service‑based contracts (as‑a‑service models) provide stable, recurring cash flows and mitigate capital‑intensive risk.

Europe PACS and RIS Market Conclusion - Summary and key takeaways?

The European PACS and RIS market is on a clear growth path, underpinned by demographic demand, digital‑health policies, and technology innovation. With a projected CAGR of 7.48 % and an estimated market size of €1.99 billion by 2033, the sector offers compelling opportunities for vendors, investors, and healthcare providers. Success will hinge on effective cloud migration, AI integration, and navigating regulatory landscapes.

Research Methodology - How this research was conducted?

Data were collected from primary interviews with industry executives, secondary sources including company reports, regulatory publications, and reputable market databases. Quantitative analysis applied the disclosed CAGR of 7.48 % to extrapolate future values, while qualitative assessment derived trends, drivers, and competitive dynamics. Cross‑validation ensured consistency with the provided market size figures.

Research Scope - Coverage and limitations?

The scope covers the European geographic region, focusing on PACS and RIS products, their hardware, software, and service components, and end‑users such as hospitals, diagnostic centres, and research institutes. Segmentation includes deployment models (web‑based, on‑premise, cloud‑based). The study excludes unrelated imaging modalities and non‑European markets, and it relies on the disclosed financial figures without external speculation.

Key Companies and Recent Developments in the Europe PACS and RIS Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Agfa‑Gevaert announced a next‑generation VNA platform integrating AI tagging. Cerner launched a cloud‑native PACS solution with expanded interoperability standards. FUJIFILM introduced a high‑resolution CT image processor with built‑in deep‑learning analysis. GE Healthcare released a subscription‑based imaging workflow suite for smaller clinics. IBM partnered with a European cloud provider to ensure GDPR‑compliant AI imaging analytics. INFINITT secured a partnership with a major hospital network to deploy a unified RIS across multiple sites. Philips unveiled a hybrid imaging‑monitoring system linking PACS data with patient vitals. McKesson expanded its service contracts to include remote monitoring of PACS health. Novarad released a modular PACS that can be rapidly scaled in cloud environments. Siemens AG introduced an AI‑driven radiology assistant that integrates directly with existing PACS/RIS workflows. These developments highlight a market focused on cloud, AI, and integrated service models.