1. North America Vendor Management Software Market Overview - Definition, scope, and significance?

The North America Vendor Management Software (VMS) market encompasses solutions that help organizations automate procurement, onboarding, performance tracking, risk assessment, and contract compliance of third‑party suppliers. The scope includes cloud‑based and on‑premise platforms catering to large enterprises and SMEs across key verticals such as retail, manufacturing, BFSI, and IT/telecom. Its significance lies in enabling businesses to reduce supply‑chain costs, mitigate vendor‑related risks, and achieve greater strategic sourcing efficiency in a highly competitive regional economy.

2. North America Vendor Management Software Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include heightened regulatory scrutiny, the need for digital transformation, and pressure to improve supplier transparency. Opportunities arise from the growing adoption of AI‑enabled analytics and the expansion of cloud deployment models. Primary restraints are legacy system integration complexities and concerns over data security in multi‑tenant environments. Challenges include talent shortages for VMS implementation and fragmented vendor ecosystems that demand robust integration capabilities.

3. North America Vendor Management Software Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a rapid shift toward cloud‑first VMS solutions, driven by scalability and lower total cost of ownership. Emerging trends feature AI‑driven risk scoring, blockchain‑based contract verification, and the convergence of VMS with broader spend‑management suites. Additionally, subscription‑based pricing models and modular architecture are gaining traction, allowing organizations to tailor functionality to specific procurement maturity levels.

4. COVID-19 Impact on the North America Vendor Management Software Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated digital procurement initiatives as remote work forced enterprises to adopt cloud VMS platforms for uninterrupted supplier collaboration. Short‑term disruptions in supply chains heightened the need for real‑time visibility, boosting software adoption. Recovery has been strong, with organizations continuing to invest in resilient vendor management capabilities, positioning the market on a sustained growth path beyond the immediate pandemic aftermath.

5. North America Vendor Management Software Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape features a mix of established technology giants and niche specialists. Prominent players include Coupa Software Inc., IBM Corporation, SAP SE, and LogicManager, Inc., each leveraging extensive enterprise portfolios. Smaller but focused firms such as Gatekeeper (Cinergy Technology Limited), HICX Solutions Ltd., and Ncontracts contribute innovative functionalities. Recent consolidation activity is modest, with strategic partnerships and acquisitions aimed at enhancing AI and analytics capabilities rather than large‑scale mergers.

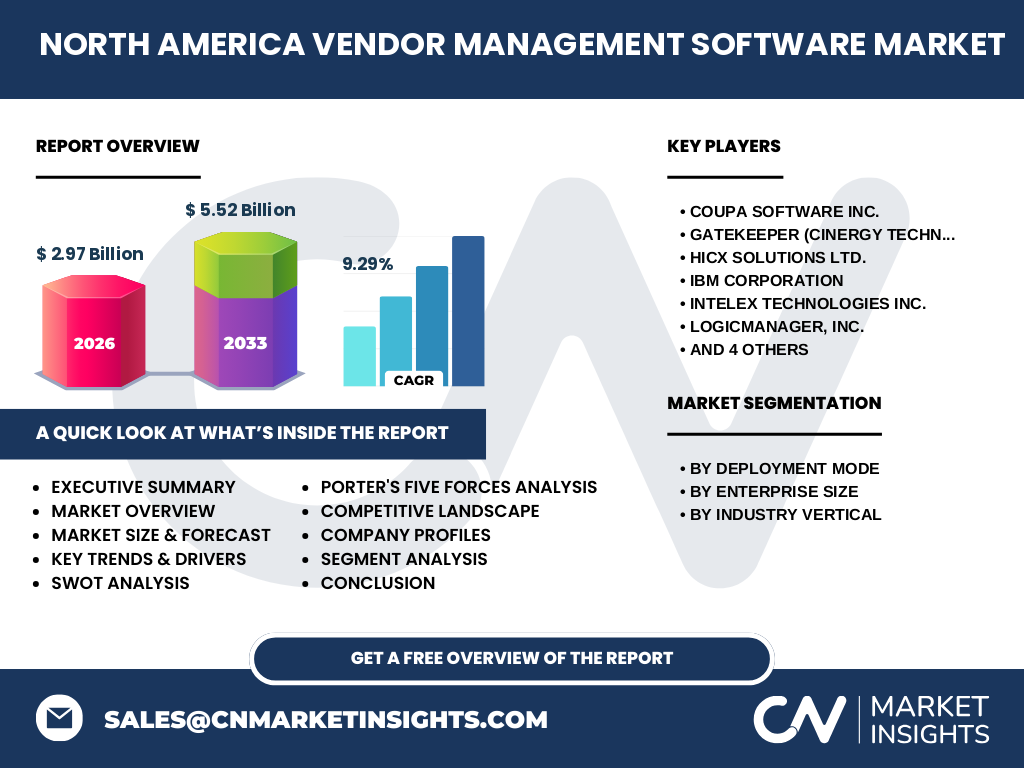

6. Executive Summary - High-level overview and key findings about North America Vendor Management Software Market?

The North America VMS market is valued at $2.97 billion in 2026 and is projected to reach $5.52 billion by 2033, reflecting a robust CAGR of 9.29 %. Growth is driven by digital procurement mandates, regulatory pressure, and the shift toward cloud deployments. While data security and integration of legacy systems pose challenges, AI‑enhanced analytics and modular cloud solutions create significant upside. The market remains fragmented with strong competitive dynamics among both global and specialized vendors.

7. North America Vendor Management Software Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 9.29 %, the market is expected to maintain a steady upward trajectory from 2025 through 2032. The forecasted value of $5.52 billion for 2033 indicates that by 2032 the market will be approaching $5 billion, underscoring consistent demand across all enterprise sizes and verticals. This growth reflects continued cloud adoption, heightened risk management needs, and expanding use of advanced analytics in vendor oversight.

8. North America Vendor Management Software Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by deployment mode shows a near‑even split between cloud and on‑premise solutions, with cloud gaining incremental share due to lower upfront costs. By enterprise size, large enterprises dominate the market because of complex supplier networks, while SMEs are rapidly adopting scalable cloud VMS offerings. Industry verticals reveal retail and manufacturing as the largest adopters, followed by BFSI and IT/telecom, each seeking compliance and cost‑control benefits.

9. Global North America Vendor Management Software Market Size and Share by Region - Geographic distribution?

Within the global context, North America holds a leading position, accounting for the majority of the market’s $2.97 billion valuation in 2026. The region’s advanced regulatory environment, high technology adoption rates, and concentration of large enterprises drive this share. While specific percentages are not disclosed, the market’s growth outlook suggests that North America will continue to outpace other regions through 2033.

10. Regional Analysis of the North America Vendor Management Software Market - Detailed regional market performance?

The United States is the primary contributor, driven by extensive enterprise software spending and stringent supply‑chain regulations. Canada shows steady growth, benefiting from cross‑border trade and increasing digitalization in manufacturing. Both markets exhibit strong demand for cloud VMS, with the U.S. leading in AI‑enabled risk management adoption, while Canadian firms emphasize data sovereignty, favoring hybrid deployment models.

11. Leading Company Profiles in the North America Vendor Management Software Market - Industry players and strategies?

Coupa Software Inc. focuses on integrated spend management with a strong cloud ecosystem. IBM Corporation leverages its AI Watson capabilities to enhance risk analytics. SAP SE offers end‑to‑end supplier relationship modules within its broader ERP suite. LogicManager, Inc. specializes in governance, risk, and compliance (GRC) integration. Gatekeeper (Cinergy Technology Limited) and HICX Solutions Ltd. target niche verticals with customizable onboarding workflows. These companies pursue strategies such as platform extensibility, strategic alliances, and continuous AI feature rollout.

12. Porter's Five Forces Analysis of the North America Vendor Management Software Market - Competitive forces assessment?

Threat of New Entrants: Moderate, as cloud infrastructure lowers entry barriers, but brand reputation and integration expertise act as deterrents. Bargaining Power of Buyers: High, due to abundant vendor options and price sensitivity, especially among SMEs. Bargaining Power of Suppliers: Low, because the primary inputs (software development talent, cloud services) are widely available. Threat of Substitutes: Limited, as alternative manual processes lack scalability and compliance. Industry Rivalry: Intense, driven by innovation in AI, analytics, and modular pricing.

13. SWOT Analysis of the North America Vendor Management Software Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong demand for risk mitigation, mature cloud ecosystem, and high enterprise IT budgets. Weaknesses: Integration challenges with legacy systems and data security concerns. Opportunities: Expansion of AI‑driven risk scoring, blockchain contract verification, and vertical‑specific solutions. Threats: Escalating cyber‑risk landscape, potential regulatory changes that could increase compliance costs, and aggressive pricing wars among vendors.

14. North America Vendor Management Software Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with software development firms creating core VMS platforms, followed by cloud service providers delivering hosting infrastructure. System integrators add customization and integration services for large enterprises. Resellers and VARs distribute the solutions, especially to SMEs. Post‑sale, managed services and support teams ensure ongoing compliance, upgrades, and analytics reporting, completing the cycle from development to sustained customer value.

15. Key Investment Insights in the North America Vendor Management Software Market - Strategic investment recommendations?

Investors should target companies with strong AI and risk‑analytics capabilities, as these differentiate offerings and command premium pricing. Cloud‑first vendors present scalable growth and recurring revenue models. Partnerships with system integrators can accelerate market penetration among large enterprises. Additionally, focusing on vertical‑specific modules for retail and manufacturing can capture niche demand, while maintaining a flexible licensing structure to attract SMEs.

16. North America Vendor Management Software Market Conclusion - Summary and key takeaways?

The market demonstrates robust growth, propelled by digital procurement imperatives and a 9.29 % CAGR leading to a $5.52 billion valuation by 2033. Cloud adoption, AI‑enhanced risk management, and vertical customization are central to future expansion. While integration and security remain challenges, the competitive landscape offers ample opportunities for innovators and investors seeking to capitalize on the region’s leadership in vendor management technology.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with industry executives, technology partners, and procurement leaders, alongside secondary analysis of company filings, market reports, and reputable databases. Quantitative data were validated through cross‑referencing multiple sources, and qualitative insights were synthesized to identify trends, drivers, and strategic implications. Forecasting employed a compound annual growth rate model anchored to the provided 9.29 % CAGR.

18. Research Scope - Coverage and limitations?

The research covers the North America VMS market across deployment modes, enterprise sizes, and four primary industry verticals. It includes competitive profiling of the ten listed key companies and evaluates market dynamics through 2033. Limitations stem from proprietary data restrictions; therefore, exact market shares and granular regional percentages are not disclosed, focusing instead on trend analysis and strategic insight.

19. Key Companies and Recent Developments in the North America Vendor Management Software Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Coupa Software Inc. recently launched an AI‑powered supplier risk module integrated with its spend‑management suite. IBM Corporation announced a partnership with a leading cybersecurity firm to embed enhanced threat detection within its VMS offering. SAP SE introduced a cloud‑native extension for real‑time contract compliance. LogicManager, Inc. unveiled a low‑code GRC add‑on targeting SMEs. Gatekeeper (Cinergy Technology Limited) secured a strategic alliance with a major retail consortium to streamline onboarding workflows. HICX Solutions Ltd. released a blockchain‑based verification tool for high‑value contracts. These developments reflect a market emphasis on intelligence, security, and industry‑specific adaptation.