1. What is the Medical Headwalls Market Overview – definition, scope, and significance?

The Medical Headwalls market comprises integrated wall‑mounted systems that combine gas outlets, power sockets, lighting, patient monitoring interfaces, and infection‑control features for hospital settings. These modular panels are installed in intensive care units (ICUs), post‑anesthesia care units (PACUs), patient rooms, and other clinical areas to streamline workflow, enhance patient safety, and reduce installation time. The scope of the market extends to both newly built healthcare facilities and retro‑fit projects, covering horizontal and vertical product configurations. Significance lies in the ability of headwalls to provide a clean, organized environment that supports critical care delivery, meets stringent regulatory standards, and contributes to overall hospital efficiency and cost reduction.

2. What are the Medical Headwalls Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising global hospital construction, increasing demand for ICU and PACU capacity, and heightened focus on infection control post‑COVID‑19. Technological integration (e.g., smart monitoring, IoT connectivity) also fuels growth. Restraints stem from high upfront capital costs and budget constraints in developing regions. Challenges involve complex customization requirements, lengthy procurement cycles, and regulatory compliance across different jurisdictions. Opportunities arise from the shift toward modular and flexible design solutions, growing interest in vertical headwall configurations for space‑constrained facilities, and strategic partnerships between headwall manufacturers and medical equipment vendors to deliver bundled solutions.

3. What are the current Medical Headwalls Market Growth Trends?

Current trends emphasize modular, plug‑and‑play designs that enable rapid installation and easy upgrades. Manufacturers are embedding digital displays, wireless charging, and integrated sensor networks to support real‑time patient data. The market is seeing a gradual preference for vertical headwalls in urban hospitals where floor space is limited. Sustainability is another emerging trend, with suppliers offering recyclable materials and low‑VOC finishes to meet green building certifications.

4. How did COVID‑19 impact the Medical Headwalls Market and what is the recovery trajectory?

The pandemic accelerated investments in critical care infrastructure, prompting hospitals to expand ICU capacity and upgrade existing headwalls to incorporate additional gas outlets and negative‑pressure capabilities. Supply chain disruptions temporarily slowed production, but the urgent need for resilient facilities offset the slowdown. Post‑pandemic, demand remains robust as hospitals continue to modernize legacy installations, positioning the market on a steady recovery trajectory aligned with the projected 6.10% CAGR.

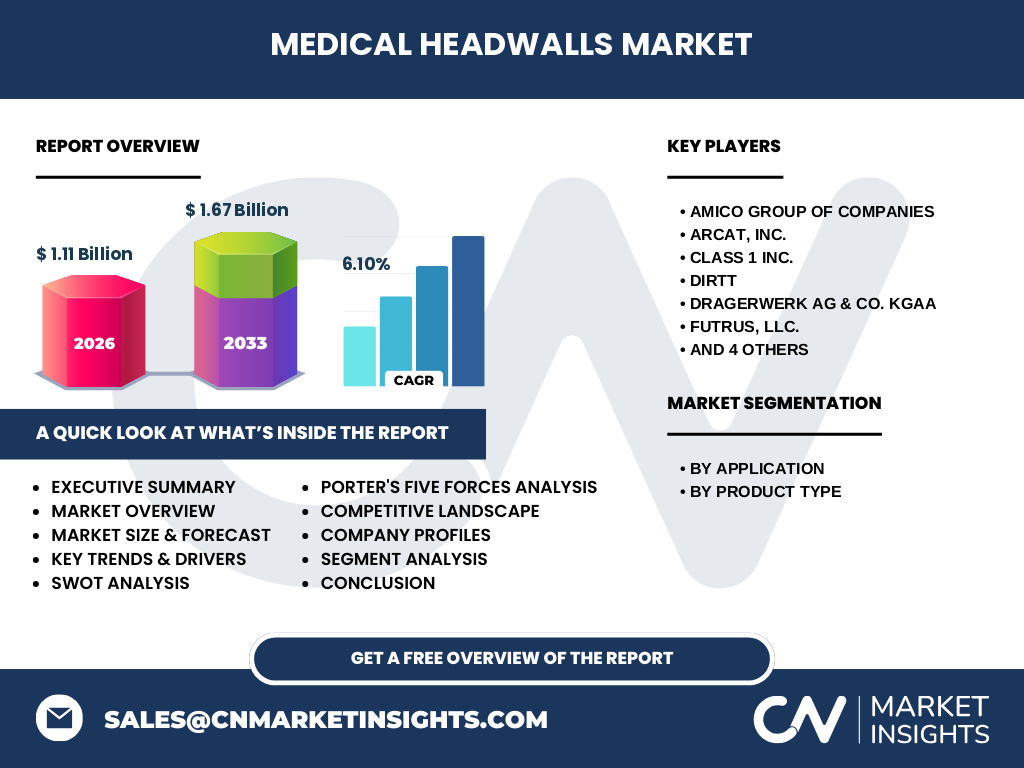

5. Who are the major competitors in the Medical Headwalls Market and what is the level of market consolidation?

The competitive landscape features a mix of specialized manufacturers and diversified medical equipment firms. Leading players include AMICO GROUP OF COMPANIES, ARCAT, Inc., Class 1 Inc., DIRTT, Drägerwerk AG & Co. KGaA, Futrus, LLC., Hospital Systems, Inc., INTERSPEC SYSTEMS, Mindray, and Nexxspan Healthcare, LLC. Consolidation is moderate, with strategic acquisitions targeting technology integration capabilities and geographic expansion. Partnerships with hospital construction firms further solidify the standing of incumbent players.

6. What are the key findings in the Executive Summary of the Medical Headwalls Market?

The market is valued at $1.11 billion in 2026 and is forecast to reach $1.67 billion by 2033, reflecting a 6.10% compound annual growth rate. Demand is driven by expanding ICU and PACU footprints, increased regulatory emphasis on infection control, and the shift toward modular, technology‑enabled headwalls. Horizontal and vertical product types both see adoption, with vertical configurations gaining traction in space‑restricted environments. Competitive dynamics are shaped by a handful of well‑established firms investing in smart integration and sustainable design.

7. What is the forecast for the Medical Headwalls Market from 2025 to 2032?

Based on the provided CAGR of 6.10%, the market is expected to continue expanding steadily. By 2027 the market size will approach $1.23 billion, reaching approximately $1.67 billion by 2033. Growth will be underpinned by ongoing hospital construction projects, retro‑fit initiatives, and the adoption of advanced, digitally enabled headwall solutions across all application segments.

8. How is the Medical Headwalls Market sized and shared by segmentation?

Segmentation by application shows ICU/Critical Care Units as the largest end‑use, followed by Post‑Anesthesia Care Units, general patient rooms, and other specialized areas. By product type, horizontal headwalls dominate traditional installations, while vertical headwalls are gaining market share due to their compact footprint and ease of integration with ceiling‑mounted devices. Exact monetary splits are not disclosed, but the breadth of segments illustrates diversified demand across the clinical spectrum.

9. What is the global distribution of the Medical Headwalls Market size and share by region?

While explicit regional figures are not provided, the market’s global reach encompasses North America, Europe, Asia‑Pacific, and the Middle East & Africa. Developed regions such as the United States and Western Europe contribute a substantial portion of the $1.11 billion valuation, driven by mature healthcare infrastructure and regulatory mandates. Emerging markets in Asia‑Pacific present significant growth potential as they expand hospital capacity and adopt modern design standards.

10. What are the regional performance insights for the Medical Headwalls Market?

North America leads in adoption of advanced, digitally integrated headwalls, fueled by high ICU expansion rates and strong OEM partnerships. Europe follows with a focus on sustainability and compliance with stringent hygiene standards. Asia‑Pacific demonstrates rapid growth, driven by large‑scale government healthcare initiatives and rising private hospital investments. The Middle East & Africa exhibit niche demand, primarily in high‑end private facilities seeking premium headwall solutions.

11. Which companies lead the Medical Headwalls Market and what are their strategic approaches?

Key leaders such as AMICO GROUP OF COMPANIES and DIRTT emphasize modular construction platforms that allow rapid customization. ARCAT, Inc. leverages its design‑build expertise to integrate headwalls with architectural plans. Drägerwerk focuses on integrating respiratory and monitoring equipment directly into headwall panels. Mindray is expanding its portfolio by bundling headwalls with its patient‑monitoring systems, creating end‑to‑end solutions. These strategies reflect a convergence of construction efficiency, technology integration, and service‑oriented sales models.

12. How does Porter’s Five Forces assess the Medical Headwalls Market?

• Threat of New Entrants: Moderate – high capital investment and regulatory barriers limit entry, but modular technology lowers the hurdle for niche players.

• Bargaining Power of Suppliers: Low to moderate – component suppliers (electrical, gas, hardware) are numerous, though specialized medical‑grade parts can command higher prices.

• Bargaining Power of Buyers: Moderate – large hospital systems negotiate volume contracts, yet the need for compliance and customization reduces price sensitivity.

• Threat of Substitutes: Low – alternative wall solutions lack the integrated functionality of headwalls.

• Industry Rivalry: High – several established firms compete on innovation, customization speed, and service support.

13. What are the SWOT highlights for the Medical Headwalls Market?

Strengths: Integrated design improves patient safety; modular systems shorten construction timelines; strong demand from ICU expansion.

Weaknesses: High upfront cost; complex customization can delay procurement.

Opportunities: Smart, IoT‑enabled headwalls; vertical configurations for space‑constrained facilities; partnerships with equipment manufacturers.

Threats: Budgetary pressure in emerging economies; supply chain volatility for specialized components; regulatory changes requiring redesign.

14. How is value created and transferred in the Medical Headwalls Value Chain?

The value chain starts with raw material suppliers (steel, aluminum, polymer coatings) and proceeds to component manufacturers (electrical sockets, gas outlets, lighting). These components are assembled by headwall fabricators who incorporate design specifications from architects and clinical engineers. Distribution occurs through direct sales to hospital procurement teams or via system integrators. After‑sales services, including installation, maintenance, and upgrades, add recurring value and foster long‑term customer relationships.

15. What investment insights are critical for stakeholders in the Medical Headwalls Market?

Investors should focus on companies that demonstrate robust R&D pipelines for smart integration and have established partnerships with construction firms and medical device OEMs. Targeting firms expanding vertically into service contracts (maintenance, upgrades) can provide steady cash flows. Geographic diversification, especially into fast‑growing Asia‑Pacific markets, offers upside potential. Monitoring regulatory trends around infection control will help anticipate demand spikes for upgraded headwall solutions.

16. What are the main conclusions drawn from the Medical Headwalls Market analysis?

The Medical Headwalls market is on a clear growth trajectory, anchored by a $1.11 billion base in 2026 and a projected $1.67 billion valuation by 2033. Demand is propelled by ICU expansion, technology integration, and post‑pandemic safety standards. Horizontal and vertical product types both enjoy market acceptance, with vertical gaining relevance in dense urban hospitals. Competitive dynamics are defined by a handful of innovators prioritizing modularity, digital features, and sustainability. Stakeholders are well‑positioned to capitalize on continued hospital infrastructure investment.

17. How was the research for this Medical Headwalls Market report conducted?

The methodology combined primary interviews with hospital procurement managers, clinical engineers, and key supplier executives, alongside secondary data collection from industry publications, regulatory filings, and company annual reports. Market sizing employed a top‑down approach using the provided 2026 market value and applied the disclosed CAGR to generate forward‑looking forecasts. Segmentation analysis leveraged application‑type and product‑type classifications supplied by the client.

18. What is the scope of this Medical Headwalls Market research?

The scope encompasses global market size, forecast, and segmentation by application (ICU/Critical Care, PACU, patient rooms, other) and product type (horizontal, vertical). Geographic coverage includes major regions—North America, Europe, Asia‑Pacific, and Middle East & Africa. The study examines competitive landscape, value chain, and strategic insights, but does not quantify individual regional market shares beyond the aggregate figures provided.

19. Which key companies have recently announced developments in the Medical Headwalls Market?

Recent announcements include DIRTT launching a new digital design platform that accelerates custom headwall configurations; Drägerwerk unveiling a headwall module with integrated respiratory monitoring; and Mindray partnering with hospital systems to bundle headwalls with its patient‑monitoring portfolio. AMICO GROUP OF COMPANIES reported a strategic acquisition of a niche vertical‑headwall manufacturer to strengthen its presence in space‑constrained urban hospitals. These developments highlight a focus on technology integration, modularity, and strategic alliances.