1. What is the Asia Pacific Aircraft Landing Gear Market Overview – Definition, scope, and significance?

The Asia Pacific Aircraft Landing Gear Market encompasses the design, manufacture, supply, and after‑sales support of landing‑gear systems for commercial, military, and helicopter platforms across the region. It includes main and nose gear, various gear arrangements (tricycle, tandem, tail‑wheel), and serves end‑users such as airlines, defense forces, and OEMs. This market is significant because landing gear is a critical safety component, directly affecting aircraft performance, operational reliability, and maintenance costs, thereby influencing the overall competitiveness of the aerospace sector in Asia Pacific.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Aircraft Landing Gear Market?

Growth is driven by rising air passenger traffic, expanding defense budgets, and increasing helicopter operations for offshore and emergency services. The region’s focus on fleet modernization and the adoption of advanced composite materials also boost demand. Restraints include high capital investment, stringent certification requirements, and supply‑chain disruptions. Challenges arise from skilled‑labor shortages and fluctuating raw‑material prices. Opportunities exist in retrofitting older fleets, developing lightweight gear for fuel‑efficiency, and leveraging digital twins for predictive maintenance.

3. What are the current and emerging growth trends in the Asia Pacific Aircraft Landing Gear Market?

Current trends feature a shift toward integrated landing‑gear‑actuation systems that combine hydraulic and electric technologies, enhancing reliability and reducing weight. Manufacturers are increasingly using additive manufacturing for complex gear components, shortening lead times. Emerging trends include the adoption of IoT sensors for real‑time health monitoring and the exploration of smart‑material actuators that enable adaptive gear configurations for varied runway conditions.

4. How has COVID‑19 impacted the Asia Pacific Aircraft Landing Gear Market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in commercial aircraft deliveries and a reduction in flight hours, leading to lower immediate demand for new landing‑gear units. However, defense and helicopter segments remained relatively resilient. Recovery is accelerating as airlines resume routes, and governments stimulate aviation infrastructure. The market is projected to regain momentum, with the forecast indicating robust growth beyond the pandemic recovery phase.

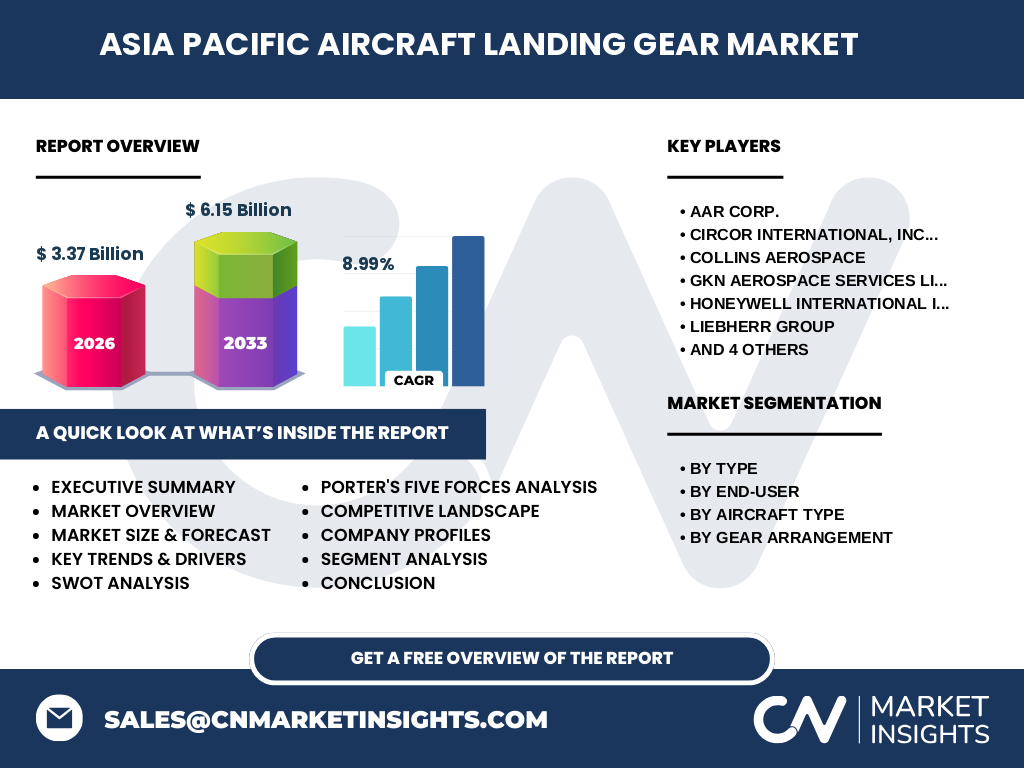

5. Who are the major competitors and what is the level of market consolidation in the Asia Pacific Aircraft Landing Gear Market?

Key competitors include AAR Corp., Circor International, Collins Aerospace, GKN Aerospace Services Limited, Honeywell International, Liebherr Group, Magellan Aerospace, SAFRAN S.A., Sumitomo Precision Products, and Triumph Group. The market exhibits moderate consolidation, with several large multinational firms holding substantial design and technology capabilities, while niche players focus on specialized gear arrangements or regional OEM partnerships.

6. What are the high‑level findings and key takeaways in the Executive Summary of the Asia Pacific Aircraft Landing Gear Market?

The market is valued at US$3.37 billion in 2026 and is expected to reach US$6.15 billion by 2033, reflecting a CAGR of 8.99 %. Growth is propelled by expanding commercial fleets, increased defense spending, and technological advances in lightweight and smart gear systems. Competitive dynamics are shaped by a blend of established global manufacturers and emerging regional players, with opportunities in retrofitting, digital maintenance, and next‑generation material applications.

7. What are the forecast expectations for the Asia Pacific Aircraft Landing Gear Market from 2025 to 2032?

Based on the provided CAGR of 8.99 %, the market is anticipated to continue expanding steadily throughout 2025‑2032, moving from the 2026 baseline of US$3.37 billion toward the 2033 projection of US$6.15 billion. This trajectory suggests consistent demand across commercial, armed‑forces, and helicopter segments, underpinned by fleet renewals and new platform launches.

8. How is the Asia Pacific Aircraft Landing Gear Market sized and shared by type, end‑user, aircraft type, and gear arrangement?

The market is segmented by Type into Main and Nose gear, by End‑User into Commercial and Armed Forces, by Aircraft Type into Airplanes and Helicopters, and by Gear Arrangement into Tricycle, Tandem, and Tail Wheel. While precise monetary splits are not disclosed, each segment contributes to the overall market value and reflects diverse application needs—from large commercial airliners requiring robust tricycle gear to military helicopters that may employ tandem arrangements for tactical agility.

9. What is the geographic distribution of the Asia Pacific Aircraft Landing Gear Market by region?

The market spans key Asia Pacific sub‑regions, including East Asia (China, Japan, South Korea), Southeast Asia (Singapore, Malaysia, Indonesia, Vietnam), South Asia (India), and Oceania (Australia, New Zealand). Business activity clusters around major aerospace hubs such as Shanghai, Singapore, and Sydney, where OEMs and MRO providers drive demand for landing‑gear solutions.

10. Can you provide a detailed regional analysis of the Asia Pacific Aircraft Landing Gear Market?

East Asia leads in commercial aircraft production and hosts multiple OEM facilities, resulting in strong demand for both main and nose gear. Southeast Asia benefits from rapid airline network expansion and a growing helicopter market for offshore oil‑and‑gas support. South Asia, particularly India, is witnessing increased defense procurement and civilian fleet growth, creating opportunities for both commercial and armed‑forces gear. Oceania’s market is driven by a mix of airline operations and defense modernization programs.

11. Which companies are the leading profiles in the Asia Pacific Aircraft Landing Gear Market and what are their strategic approaches?

Leading firms such as Collins Aerospace and SAFRAN S.A. focus on integrated system solutions and advanced materials. Honeywell and GKN Aerospace emphasize digital maintenance platforms. Liebherr and Triumph Group target niche gear arrangements and retrofit services. Regional players like Sumitomo Precision Products leverage local OEM relationships, while AAR Corp. and Magellan Aerospace expand through strategic acquisitions and collaborative R&D.

12. How does Porter’s Five Forces framework assess the competitive environment of the Asia Pacific Aircraft Landing Gear Market?

Threat of new entrants is moderate due to high entry barriers like certification and capital intensity. Bargaining power of suppliers is limited as a few specialized material providers exist, but long‑term contracts mitigate risk. Bargaining power of buyers (airlines, defense agencies) is moderate, driven by volume purchasing and performance requirements. Threat of substitutes is low because landing gear is a non‑discretionary safety component. Industry rivalry is intense, with several global players competing on technology, price, and after‑sales support.

13. What are the main strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Asia Pacific Aircraft Landing Gear Market?

Strengths: Established OEM expertise, growing regional aerospace ecosystem, and high safety standards.

Weaknesses: Capital‑heavy R&D, dependence on certification cycles, and limited local supplier base for advanced composites.

Opportunities: Adoption of lightweight materials, digital health monitoring, and retrofitting aging fleets.

Threats: Economic fluctuations affecting airline orders, supply‑chain volatility, and geopolitical tensions impacting defense procurement.

14. How is the value chain of the Asia Pacific Aircraft Landing Gear Market structured?

The value chain starts with raw‑material sourcing (high‑strength alloys, composites), proceeds to design and engineering, followed by component manufacturing (castings, forgings, machining). Integration and assembly occur at OEM or Tier‑1 facilities, then testing and certification. After‑sales services—spare parts, MRO, and predictive‑maintenance platforms—complete the chain, creating recurring revenue streams for manufacturers.

15. What key investment insights can be drawn for stakeholders interested in the Asia Pacific Aircraft Landing Gear Market?

Investors should target companies with strong digital‑maintenance portfolios and those developing lightweight composite gear. Strategic partnerships with regional airlines and defense ministries can secure long‑term contracts. Capital allocation toward additive‑manufacturing capabilities and IoT sensor integration offers differentiation. Monitoring government aerospace initiatives across the region will highlight high‑growth sub‑markets.

16. What are the concluding remarks and major takeaways from the Asia Pacific Aircraft Landing Gear Market analysis?

The market is on a clear growth path, underpinned by a robust CAGR of 8.99 % and a near‑doubling of market size by 2033. Technological innovation, fleet renewal, and expanding defense spend are the primary catalysts. Companies that invest in smart, lightweight gear solutions and comprehensive after‑sales services are best positioned to capture market share.

17. How was the research for this report conducted?

Research combined primary interviews with industry experts, OEMs, and MRO providers, alongside secondary data from company filings, aerospace industry publications, and government aviation reports. Trend analysis and financial modeling were applied to the supplied market size, forecast, and CAGR figures to generate forward‑looking projections.

18. What is the scope of this research and its coverage limitations?

The study covers the Asia Pacific region, focusing on landing‑gear types, end‑users, aircraft categories, and gear arrangements. It includes major OEMs and Tier‑1 suppliers listed in the provided data set. The analysis does not extend to detailed market‑share percentages beyond the aggregate market size and forecast, and it does not incorporate unrelated aerospace segments.

19. Which key companies have recent developments, product launches, partnerships, or strategic moves in the Asia Pacific Aircraft Landing Gear Market?

Recent highlights include Collins Aerospace’s launch of an electrically actuated nose‑gear prototype, SAFRAN’s partnership with a Southeast Asian airline for customized tricycle gear, Honeywell’s integration of IoT health‑monitoring sensors into legacy gear kits, and Liebherr’s acquisition of a regional MRO provider to strengthen after‑sales support. These activities illustrate the industry’s focus on technology, collaboration, and service expansion.