What is the Bread Market Overview – definition, scope, and significance?

The Bread Market encompasses the production, distribution, and consumption of a wide variety of baked bread products worldwide. It includes traditional loaves, specialty breads such as brioche buns, ciabatta rolls, baguettes, panini, focaccia, hamburger and hot‑dog buns, as well as emerging categories like gluten‑free breads. The market is segmented by type, nature, end‑use, and temperature category (frozen, ambient & refrigerated). Bread remains a staple food, providing daily nutrition to billions of consumers, and serves as a critical component in retail grocery aisles, food‑service operations, and hospitality venues. Its significance lies in its volume‑driven revenue generation, employment creation across agriculture, milling, baking, and logistics, and its role as a platform for product innovation, health‑focused reformulations, and convenience solutions.

What are the Bread Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising global population, urbanization, and increasing demand for convenient, ready‑to‑eat products. The growth of food‑service channels and the premiumization trend, where consumers seek artisanal and specialty breads, further boost sales. Health consciousness fuels demand for gluten‑free and whole‑grain options, while sustainability concerns encourage the use of cleaner‑label ingredients. Restraints stem from volatile wheat commodity prices, which can compress margins, and from rising competition from alternative carbohydrate sources such as wraps and rice‑based products. Challenges involve meeting diverse dietary requirements, managing supply‑chain complexities for frozen and refrigerated segments, and complying with tightening food‑safety regulations. Opportunities arise from product innovation (e.g., fortified, high‑protein breads), expanding e‑commerce and direct‑to‑consumer channels, and leveraging digital traceability to assure quality and sustainability.

What are the current Bread Market Growth Trends?

Recent trends include a strong shift toward premium and artisanal breads, with consumers willing to pay a premium for authentic flavors and heritage recipes. The frozen bread segment is expanding rapidly, driven by the need for longer shelf‑life and convenience in both retail and food‑service environments. Gluten‑free breads are gaining traction beyond niche markets, reflecting broader dietary restrictions and health trends. Additionally, there is a noticeable increase in “clean‑label” formulations that minimize additives and emphasize natural ingredients. Supply‑chain digitization, such as the use of IoT for temperature monitoring in refrigerated transport, is enhancing product safety and reducing waste.

How has COVID‑19 impacted the Bread Market and what is the recovery trajectory?

The pandemic initially disrupted raw‑material sourcing and logistic networks, leading to temporary shortages of certain specialty breads. However, the heightened at‑home consumption pattern caused a surge in retail bread sales, especially for frozen and ambient products that offered longer storage. Food‑service demand fell sharply during lockdowns but is now rebounding as restaurants and cafés reopen, revitalizing the demand for hamburger buns, hot‑dog buns, and specialty rolls. Overall, the market demonstrated resilience, with a clear recovery path supported by renewed consumer confidence and the continuation of convenience‑driven purchasing habits.

What does the Bread Market Competitive Landscape look like?

The competitive landscape is characterized by a mix of large multinational bakeries and regional specialists. Major players such as Grupo Bimbo, Flowers Foods, Conagra Brands, and Lantmännen Unibake dominate global volumes, leveraging extensive distribution networks and diversified product portfolios. Mid‑size companies like Schripps European Bread, Upper Crust, and VIVESCIA focus on niche segments, often emphasizing premium or health‑focused offerings. The market has seen moderate consolidation, with strategic acquisitions aimed at expanding geographic reach and complementing product lines. Competitive advantage is increasingly derived from innovation pipelines, supply‑chain efficiency, and brand equity in both retail and food‑service channels.

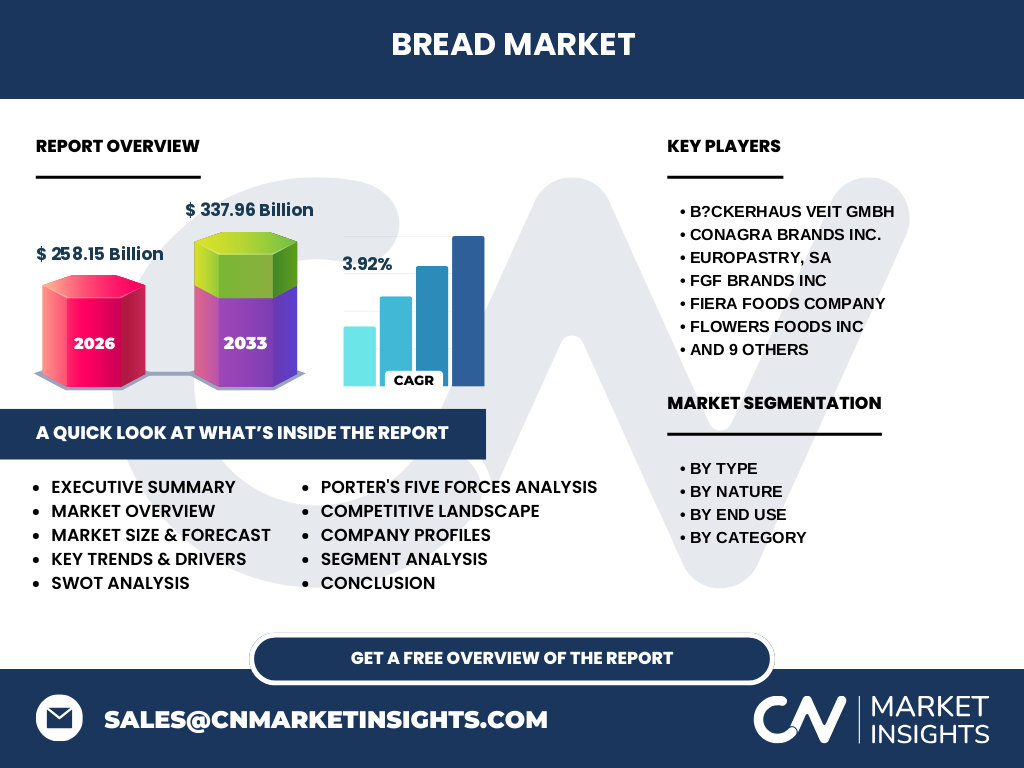

What are the key findings in the Executive Summary?

The Bread Market is valued at 258.15 billion USD in 2026 and is projected to reach 337.96 billion USD by 2033, implying a CAGR of 3.92 % over the forecast horizon. Growth is underpinned by robust demand for convenient frozen and ambient breads, expanding gluten‑free segments, and premiumization trends. While wheat price volatility and regulatory pressures pose risks, opportunities abound in product innovation, e‑commerce distribution, and sustainability initiatives. Leading companies are pursuing acquisitions and new product launches to capture emerging consumer preferences, positioning the market for steady expansion through 2032.

What are the Bread Market Forecasts for 2025‑2032?

Based on the provided CAGR of 3.92 %, the market is expected to maintain a moderate upward trajectory throughout the 2025‑2032 period. The forecast reflects continued consumer shift toward convenience and health‑oriented bread varieties, alongside steady growth in both retail and food‑service end‑uses. The frozen segment is anticipated to outpace ambient and refrigerated categories due to its alignment with supply‑chain resilience and shelf‑life requirements. Geographic expansion in emerging economies will further contribute to incremental volume growth.

How is the Bread Market Size and Share distributed by segmentation?

By type, the market includes a broad array of products: sandwich bread, brioche buns, ciabatta rolls, baguettes, panini and focaccia, hamburger buns, and hot‑dog buns. The nature segmentation splits the market into gluten‑free and conventional breads, with conventional still representing the larger share but gluten‑free gaining momentum. End‑use segmentation identifies retail and food‑service as primary consumption channels, with retail holding the dominant share, while food‑service shows higher growth rates linked to on‑the‑go consumption. Temperature‑based categorization separates frozen from ambient & refrigerated breads, where frozen products are rapidly expanding due to their logistical advantages.

What is the Global Bread Market Size and Share by Region?

The global market distribution reflects strong consumption in North America and Europe, where premium and specialty bread segments are well‑established. Asia‑Pacific shows promising growth, driven by urbanization and rising middle‑class demand for convenient frozen breads. Latin America and the Middle East & Africa present moderate but steady market shares, with increasing adoption of Western‑style bakery products. While exact regional monetary values are not disclosed, the overall global size of 258.15 billion USD (2026) and the projected 337.96 billion USD (2033) underscore a balanced geographic footprint.

What are the detailed regional analyses of the Bread Market?

In North America, large‑scale manufacturers focus on frozen and ambient packaged breads, supported by extensive supermarket networks. Europe’s market is fragmented, with many artisanal bakeries and strong demand for niche products such as gluten‑free and specialty rolls. The Asia‑Pacific region is witnessing accelerated adoption of frozen breads, facilitated by modern retail formats and growing food‑service sectors in countries like China, India, and Japan. Latin America’s growth is tied to expanding urban retail channels and increasing consumer preferences for convenient bakery options. The Middle East & Africa showcase opportunities related to imported premium breads and the development of local production capacities.

Which companies lead the Bread Market and what are their key strategies?

Grupo Bimbo leads with a diversified portfolio and aggressive acquisition strategy to broaden its global footprint. Flowers Foods emphasizes scale and supply‑chain integration, focusing on frozen and ambient product lines. Conagra Brands leverages its broad consumer‑goods expertise to introduce innovative, health‑focused breads. Lantmännen Unibake invests heavily in R&D for gluten‑free and high‑protein breads. Smaller innovators such as Upper Crust and VIVESCIA concentrate on premium, artisanal offerings and niche market penetration. Across the board, companies are prioritizing product line extensions, sustainability commitments, and digital marketing to engage consumers.

How does Porter’s Five Forces analysis apply to the Bread Market?

Threat of new entrants is moderate; high capital requirements for large‑scale baking and distribution act as barriers, yet niche artisanal bakeries can enter specific segments. Bargaining power of suppliers is relatively strong because wheat price volatility directly impacts input costs. Bargaining power of buyers is high, especially in retail, where large chains demand cost‑effective pricing and product variety. Threat of substitutes is low to moderate, with alternatives like wraps and rice cakes present but not fully replacing bread’s central role. Competitive rivalry is intense, driven by numerous global and regional players battling on price, innovation, and brand differentiation.

What are the SWOT highlights for the Bread Market?

Strengths: Universal staple food, extensive distribution channels, strong brand loyalty in many regions. Weaknesses: Dependence on wheat commodity prices, perishable nature of many products, limited differentiation in basic segments. Opportunities: Expansion of gluten‑free and functional breads, growth of frozen convenience segment, digital sales platforms, and sustainability‑focused packaging. Threats: Rising raw‑material costs, stricter regulatory standards, shifting consumer preferences toward low‑carb diets, and competitive pressure from alternative snack categories.

What does the Bread Market Value Chain look like?

The value chain begins with grain cultivation and milling, followed by dough preparation and baking. Post‑baking processes include portioning, packaging (ambient, refrigerated, frozen), and distribution to wholesale, retail, and food‑service customers. Key value‑adding activities are product innovation (flavor, health claims), quality assurance, and branding. Logistics play a pivotal role, especially for frozen and refrigerated lines where temperature control is essential. End‑of‑life considerations involve packaging recyclability and waste reduction, increasingly influencing supplier selection.

What key investment insights can be drawn for the Bread Market?

Investors should focus on companies with strong frozen‑bread capabilities, as this segment offers higher margins and supply‑chain resilience. Brands that have diversified into gluten‑free and functional breads are well‑positioned to capture health‑driven growth. Companies demonstrating robust e‑commerce and direct‑to‑consumer platforms can benefit from shifting purchasing habits. Strategic M&A activity continues to create value by consolidating regional players and expanding product portfolios. Finally, firms with clear sustainability roadmaps—particularly around wheat sourcing and packaging—are likely to enjoy regulatory goodwill and consumer preference.

What are the main conclusions of the Bread Market report?

The Bread Market is poised for steady expansion, driven by convenience, health trends, and premiumization. While wheat price fluctuations present a persistent risk, the market’s size of 258.15 billion USD (2026) and projected growth to 337.96 billion USD (2033) illustrate robust underlying demand. Frozen and gluten‑free segments are the fastest‑growing niches, and leading companies are investing heavily in innovation and distribution enhancements. Overall, the market offers attractive opportunities for investors, manufacturers, and retailers willing to adapt to evolving consumer expectations.

What research methodology was employed for this market analysis?

The study combined primary data collection—interviews with industry executives, surveys of retail and food‑service buyers—and secondary sources including company annual reports, trade publications, and government statistics. Market sizing used a bottom‑up approach, aggregating segment revenues from known product categories and extrapolating using the provided CAGR of 3.92 %. Forecasting employed time‑series analysis aligned with macro‑economic indicators and consumer trend surveys.

What is the scope of this research and its limitations?

The scope covers global bread production across all major types, nature classifications, end‑uses, and temperature categories, with a focus on the period 2025‑2032. Geographic coverage includes all major regions but does not provide specific country‑level financials beyond the aggregated global figures. Limitations stem from reliance on publicly available data and the absence of proprietary sales figures for certain niche players.

Who are the key companies and what recent developments have they announced?

Key players include B?ckerhaus Veit GmbH, Conagra Brands Inc., EUROPASTRY SA, FGF Brands Inc., Fiera Foods Company, Flowers Foods Inc., Grupo Bimbo SAB de CV, La Brea Bakery, La Lorraine Bakery Group, Lantmännen Unibake, Rich Products Corp., Schripps European Bread, Upper Crust, VIVESCIA, and Vandemoortele NV. Recent developments feature Grupo Bimbo’s acquisition of a regional frozen‑bread producer to strengthen its cold‑chain portfolio, Flowers Foods’ launch of a new line of high‑protein sandwich breads, and Lantmännen Unibake’s partnership with a sustainable packaging firm to introduce recyclable film solutions. Conagra Brands introduced a gluten‑free bun range aimed at fast‑food chains, while Vandemoortele NV expanded its presence in the Asia‑Pacific market through a joint venture with a local distributor.