What is the Hemophilia Treatment Market Overview - Definition, scope, and significance?

The Hemophilia Treatment Market comprises products and therapies designed to manage bleeding disorders, primarily hemophilia A, B, and the rarer C type. It includes plasma‑derived and recombinant coagulation factor concentrates, desmopressin, antifibrinolytics, and emerging modalities such as gene and antibody therapies. The market’s significance stems from the life‑long treatment needs of patients, high clinical stakes of bleeding events, and substantial healthcare spending, positioning it as a critical segment of the global specialty pharmaceuticals industry.

What are the Hemophilia Treatment Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the growing prevalence of hemophilia, increased diagnosis rates, and the shift toward prophylactic and personalized regimens. Technological advances in gene therapy and recombinant production further boost growth. Restraints involve high product costs, reimbursement hurdles, and strict regulatory pathways. Challenges arise from inhibitor development in patients and limited access in low‑income regions. Opportunities exist in biosimilar entry, tele‑health monitoring, and expanding indications for novel antibody and gene‑editing therapies.

What are the current Hemophilia Treatment Market Growth Trends?

Current trends feature a rapid uptake of extended‑half‑life recombinant factors, a surge in clinical trials for gene therapy delivering potentially curative outcomes, and an increasing preference for prophylactic over on‑demand treatment. Digital adherence platforms and home infusion services are emerging, enhancing patient convenience. Additionally, collaborations between biotech firms and large pharmaceutical companies are accelerating pipeline development and market entry.

How has COVID‑19 impacted the Hemophilia Treatment Market and what is the recovery trajectory?

The pandemic disrupted supply chains for plasma‑derived products and limited patient visits for routine infusions, temporarily reducing market volume. However, heightened awareness of home‑based care accelerated telemedicine adoption and self‑administration technologies. Post‑2022, the market has rebounded, with demand aligning to pre‑pandemic levels, and the recovery is supported by resumed clinical trials and renewed investment in gene‑therapy programs.

What does the Hemophilia Treatment Market Competitive Landscape look like?

The market is dominated by a mix of legacy biotech firms and diversified pharmaceutical giants. Major players such as Baxter International, Bayer AG, CSL Limited, Roche, and Pfizer command significant shares across plasma‑derived and recombinant segments. Recent consolidation includes strategic acquisitions of niche gene‑therapy companies and partnership agreements aimed at expanding product portfolios and geographic reach.

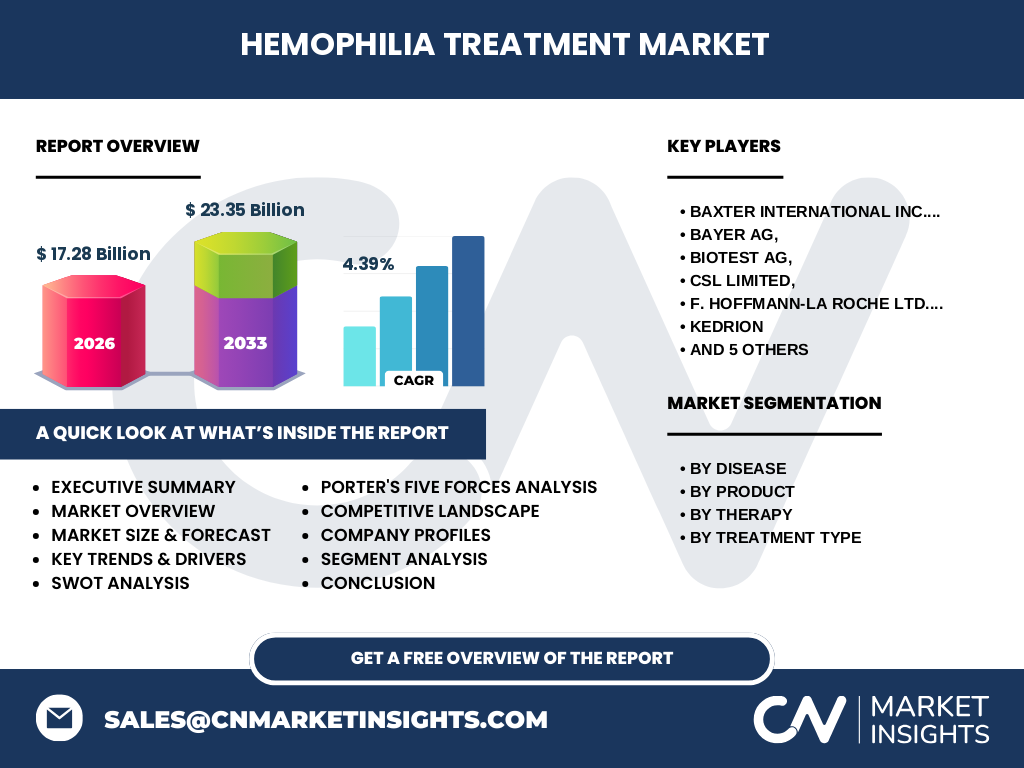

Can you provide an Executive Summary of the Hemophilia Treatment Market?

The Hemophilia Treatment Market was valued at $17.28 billion in 2026 and is projected to reach $23.35 billion by 2033, reflecting a CAGR of 4.39 %. Growth is propelled by expanding patient populations, innovative therapies—including gene and antibody approaches—and a shift toward prophylaxis. While cost pressures and inhibitor complications pose challenges, the market remains attractive due to strong pipeline activity and ongoing consolidation among leading firms.

What are the Hemophilia Treatment Market Forecasts for 2025‑2032?

Based on the stated CAGR of 4.39 %, the market is expected to maintain steady expansion through 2032. The forecast anticipates continued rise in premium recombinant and gene‑therapy products, while plasma‑derived segments experience modest growth. Emerging markets will contribute incremental volume as reimbursement frameworks evolve, supporting a sustained upward trajectory toward the $23.35 billion mark projected for 2033.

How is the Hemophilia Treatment Market Size and Share distributed by segmentation?

Segmentation by disease highlights hemophilia A as the largest contributor, followed by hemophilia B; hemophilia C represents a minimal share due to its rarity. By product, recombinant coagulation factor concentrates dominate, with plasma‑derived concentrates maintaining a solid base. Desmopressin and antifibrinolytic agents occupy niche roles. Therapy segmentation shows replacement therapy as the core, while ITI, gene, and antibody therapies are fast‑growing sub‑segments. Treatment‑type analysis reveals a clear preference for prophylaxis over on‑demand use.

What is the Global Hemophilia Treatment Market Size and Share by Region?

Geographically, North America and Europe hold the majority of market value, driven by advanced healthcare systems and high adoption of premium therapies. The Asia‑Pacific region demonstrates the fastest growth rate, spurred by rising disease awareness and expanding payer coverage. Latin America and the Middle East show moderate participation, while Africa remains the smallest market due to limited infrastructure and access.

What does the Regional Analysis of the Hemophilia Treatment Market reveal?

In North America, United States demand is fueled by innovative product launches and strong insurance reimbursement. Europe’s market is characterized by extensive public‑funded programs and early adoption of gene therapy trials. Asia‑Pacific growth is anchored by China, Japan, and India, where increasing diagnostic capabilities and emerging biopharma hubs are expanding treatment access. Regional regulatory variations influence time‑to‑market for new therapies across these zones.

Who are the leading companies in the Hemophilia Treatment Market and what are their strategies?

Key firms include Baxter International, Bayer AG, Biotest AG, CSL Limited, Roche, Kedrion, Novo Nordisk, Octapharma, Pfizer, and Sanofi. Strategies revolve around expanding recombinant and extended‑half‑life portfolios, investing in gene‑therapy pipelines, pursuing biosimilar development, and forming alliances to leverage distribution networks. Several companies are also focusing on digital health solutions to improve adherence and real‑world evidence collection.

How does Porter’s Five Forces analysis apply to the Hemophilia Treatment Market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is limited as most raw materials are sourced from established bioprocess providers. Bargaining power of buyers (payers and hospitals) is high, driven by cost‑sensitivity and demand for value‑based outcomes. Threat of substitutes is low currently, though emerging gene‑editing technologies could alter the landscape. Industry rivalry is intense, with firms competing on innovation, pricing, and market access.

What are the SWOT insights for the Hemophilia Treatment Market?

Strengths: Established patient base, high therapeutic necessity, and strong pipeline of advanced therapies. Weaknesses: Dependence on costly biologics, complex manufacturing, and inhibitor development. Opportunities: Gene and antibody therapies, expansion into emerging markets, and digital adherence tools. Threats: Pricing pressures, stringent regulatory requirements, and potential disruptive technologies that could bypass traditional factor replacement.

What does the Hemophilia Treatment Market Value Chain look like?

The value chain begins with R&D and clinical testing, followed by plasma collection or recombinant expression, purification, and formulation. Manufacturing is highly regulated and often concentrated among a few global facilities. Distribution involves specialty pharmacies and hospital formularies, while patient support programs and home‑infusion services add downstream value. Post‑marketing surveillance and real‑world data collection complete the loop, informing next‑generation product improvements.

What key investment insights can be drawn for the Hemophilia Treatment Market?

Investors should focus on companies with robust gene‑therapy pipelines and those securing long‑term reimbursement agreements for prophylactic regimens. Strategic partnerships that enable rapid market entry in Asia‑Pacific present growth upside. Additionally, firms developing cost‑effective biosimilars or digital adherence platforms may deliver attractive risk‑adjusted returns amid pricing scrutiny.

What are the main conclusions of the Hemophilia Treatment Market analysis?

The market is on a steady growth path, underpinned by therapeutic innovation and shifting treatment paradigms toward prophylaxis and potentially curative gene therapy. While cost and inhibitor issues persist, the combination of expanding patient populations and strategic corporate actions creates a favorable outlook for stakeholders seeking long‑term value.

How was the research methodology designed for this report?

The study employed a mixed‑method approach, integrating secondary data from industry reports, regulatory filings, and peer‑reviewed publications with primary insights gathered through expert interviews. Market sizing utilized top‑down and bottom‑up techniques, cross‑validated against disclosed financials of key players. Forecasting applied compound annual growth rate (CAGR) calculations based on historical trends and pipeline projections.

What is the scope of this Hemophilia Treatment Market research?

The scope covers global market dynamics from 2026 to 2033, examining disease, product, therapy, and treatment‑type segments. Geographic coverage includes North America, Europe, Asia‑Pacific, Latin America, the Middle East, and Africa. The analysis encompasses major manufacturers, emerging entrants, and the impact of regulatory and reimbursement environments, while excluding unrelated bleeding disorders.

Who are the key companies and what recent developments have they announced?

Key players such as Baxter International, Bayer AG, CSL Limited, Roche, and Pfizer have recently launched extended‑half‑life recombinant factors and announced positive Phase III gene‑therapy results. Octapharma and Kedrion reported expansion of plasma‑derived production capacity in Europe. Novo Nordisk entered a collaboration with a biotech firm to explore antibody‑based hemostatic agents. Sanofi disclosed a partnership for digital adherence tools targeting hemophilia patients.