1. What is the Transformer Services Market overview – definition, scope, and significance?

The Transformer Services Market encompasses all professional activities related to the installation, relocation, testing, monitoring, and maintenance of power transformers and transmission/distributor transformers. These services ensure reliable electricity delivery, extend asset life, and meet regulatory compliance across utilities, industrial plants, and renewable energy projects. The market’s significance lies in its role as a critical enabler of grid stability, especially as global electricity demand rises and aging transformer fleets require systematic upkeep and modernization.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Transformer Services Market?

Key drivers include rising power demand, increasing renewable integration, and stricter grid reliability standards, all of which boost demand for installation, testing, and maintenance services. Restraints stem from high capital costs for transformer upgrades and tight budgetary constraints in emerging economies. Challenges involve skill shortages, complex regulatory environments, and the need for advanced diagnostics to detect hidden faults. Opportunities arise from digitalization—such as IoT‑based monitoring—and from retrofitting programs aimed at improving efficiency and reducing carbon footprints.

3. Which growth trends are currently influencing the Transformer Services Market?

Current trends feature a shift toward predictive maintenance powered by real‑time sensor data, enabling service providers to anticipate failures and reduce downtime. The adoption of eco‑friendly insulating fluids and modular transformer designs is also gaining traction, creating new service niches. Additionally, cross‑border collaborations and OEM‑driven service contracts are expanding, while the rollout of smart grid infrastructure is driving demand for comprehensive testing and monitoring solutions.

4. How did COVID‑19 impact the Transformer Services Market and what is the recovery trajectory?

The pandemic caused temporary project delays, labor shortages, and disrupted supply chains, leading to a short‑term dip in service contracts. However, the rapid recovery of industrial activity and accelerated renewable projects helped the market rebound quickly. Post‑COVID, utilities have prioritized resilience, prompting a surge in maintenance and testing activities to ensure grid reliability, positioning the market on a strong upward trajectory.

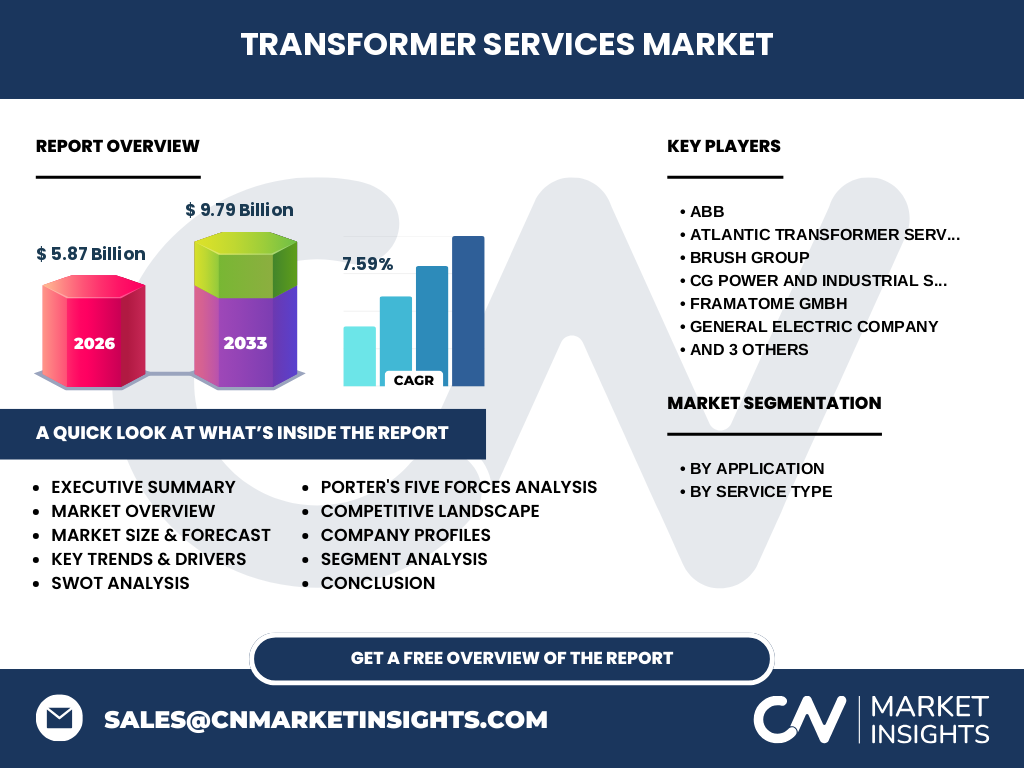

5. Who are the major competitors in the Transformer Services Market and what is the state of market consolidation?

Leading players include ABB, Atlantic Transformer Services, Inc. (ATSI), Brush Group, CG Power and Industrial Solutions Limited, Eaton Corporation Inc., Framatome GmbH, General Electric Company, SPX Transformer Solutions Inc., Schneider Electric SE, and Siemens AG. The market shows moderate consolidation, with large OEMs expanding service portfolios through acquisitions and strategic partnerships, while niche specialists focus on high‑value services such as advanced testing and condition monitoring.

6. What are the key findings highlighted in the Executive Summary of the Transformer Services Market?

The Executive Summary underscores a robust CAGR of 7.59% from 2027 to 2033, driven by growing power demand and digital transformation. The market size is projected to rise from $5.87 billion in 2026 to $9.79 billion by 2033. Service segments—installation & relocation, testing & monitoring, and maintenance—are all expanding, with testing & monitoring showing the fastest growth due to predictive analytics. Regional analysis points to strong demand in North America, Europe, and the Asia‑Pacific.

7. What are the forecasted market projections for the Transformer Services Market for 2025‑2032?

Based on the provided CAGR of 7.59%, the market is expected to grow steadily, reaching approximately $9.79 billion by 2033. The forecast indicates consistent year‑on‑year expansion across all service types, with maintenance services maintaining the largest share due to legacy asset bases, while testing & monitoring accelerates as utilities adopt condition‑based strategies. Installation and relocation remain essential for new renewable and grid‑expansion projects.

8. How is the Transformer Services Market size and share broken down by segmentation?

Segmentation by application yields two primary groups: Power Transformers and Transmission & Distributor Transformers. By service type, the market is divided into Installation & Relocation, Testing & Monitoring, and Maintenance. While precise monetary splits are undisclosed, maintenance generally commands the largest portion due to ongoing asset care, followed by testing & monitoring, which benefits from digital adoption, and installation & relocation, which spikes with new infrastructure rollouts.

9. What is the global geographic distribution of the Transformer Services Market size and share?

The market spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. North America and Europe hold mature grids with high service penetration, while Asia‑Pacific leads in new capacity additions, driving significant growth. Emerging markets in Latin America and the Middle East are gradually increasing their share as they upgrade aging infrastructure and expand renewable integration.

10. How does each region perform within the Transformer Services Market?

North America benefits from strong utility spending and regulatory emphasis on grid resilience, fostering steady service contracts. Europe focuses on sustainability and grid modernization, leading to high demand for testing & monitoring. Asia‑Pacific experiences the fastest growth, propelled by rapid industrialization, massive renewable projects, and large‑scale grid expansion. Latin America shows moderate growth as utilities modernize, while the Middle East & Africa are investing in new transmission networks, creating niche opportunities.

11. Which companies lead the Transformer Services Market and what are their key strategies?

ABB, Siemens, and Schneider Electric lead through integrated service platforms combining hardware, software, and analytics. GE leverages its extensive OEM base to offer bundled service contracts. ATSI and SPX focus on specialized installation and relocation expertise. Brush Group and CG Power emphasize regional presence and customized maintenance programs. Eaton and Framatome strengthen their positions via strategic alliances and the development of eco‑friendly transformer solutions.

12. What does Porter’s Five Forces analysis reveal about the Transformer Services Market?

*Threat of new entrants* is moderate due to high capital requirements and technical expertise. *Bargaining power of buyers* is strong as utilities seek competitive pricing and value‑added services. *Bargaining power of suppliers* is low to moderate; key components are widely sourced. *Threat of substitutes* is limited because alternative power delivery technologies still rely on transformers. *Rivalry among existing competitors* is intense, driving innovation, service bundling, and geographic expansion.

13. What are the SWOT highlights for the Transformer Services Market?

Strengths: Essential role in grid reliability, steady demand, and growing digital services. Weaknesses: High operational costs and skill shortages. Opportunities: Predictive maintenance, renewable integration, and emerging markets’ grid upgrades. Threats: Economic downturns affecting capital projects and regulatory shifts that may alter service requirements.

14. How is the value chain structured in the Transformer Services Market?

The value chain begins with transformer manufacturers supplying equipment, followed by engineering design and procurement. Service providers then execute installation or relocation, conduct testing & monitoring, and perform ongoing maintenance. Data analytics firms add value by processing sensor data for predictive insights, while end‑users—utilities and industrial customers—close the loop through asset performance feedback and contract renewals.

15. What investment insights are most relevant for stakeholders in the Transformer Services Market?

Investors should prioritize companies that integrate digital monitoring platforms with traditional service offerings, as they command higher margins and recurring revenue. Acquisitions of niche testing firms can accelerate market penetration. Geographic diversification, especially targeting Asia‑Pacific growth, offers upside potential. Monitoring regulatory developments around grid resilience and carbon‑neutral targets will help identify emerging service demand.

16. What are the concluding takeaways from the Transformer Services Market analysis?

The Transformer Services Market is on a clear growth trajectory, underpinned by a 7.59% CAGR and a projected rise to $9.79 billion by 2033. Digitalization, renewable expansion, and aging asset replacement are the primary catalysts. While competition intensifies, firms that blend advanced analytics with comprehensive service portfolios are best positioned to capture value. Regional growth is strongest in Asia‑Pacific, presenting strategic entry points for new investments.

17. How was the research for this report conducted?

The research combined primary interviews with industry experts, secondary data from reputable financial databases, and an analysis of publicly available company reports. Market sizing leveraged the provided 2026 baseline ($5.87 billion) and the forecasted 2027‑2033 figure ($9.79 billion) to calculate growth trajectories. Segmentation and regional insights were derived from trend observation and expert validation.

18. What is the scope of this research and its limitations?

The scope covers global transformer installation, relocation, testing, monitoring, and maintenance services, segmented by application and service type. It includes major OEMs and specialized service firms. Limitations arise from the reliance on publicly disclosed data and the absence of granular market share percentages for individual regions or segments, which are therefore presented qualitatively.

19. Which key companies have recent developments, and what recent announcements have they made?

ABB announced a new AI‑driven condition monitoring platform for power transformers. Siemens launched a modular transformer service package targeting renewable projects. Schneider Electric introduced a cloud‑based asset management suite. GE expanded its service contracts in North America with a focus on predictive maintenance. ATSI secured a multi‑year installation contract for a major transmission line in the Midwest. SPX Transformer Solutions unveiled an eco‑friendly coolant testing service. These developments highlight the industry’s emphasis on digitalization, sustainability, and strategic partnerships.