1. Europe Autotransfusion Devices Market Overview - Definition, scope, and significance?

The Europe autotransfusion devices market comprises equipment and accessories that collect, process, and reinfuse a patient’s own blood during surgery or trauma care. The scope covers whole‑system devices, consumables, and related services used across hospitals, specialty clinics, and ambulatory surgery centers. Its significance lies in reducing reliance on allogeneic blood, lowering transfusion‑related complications, and delivering cost‑effective peri‑operative care, thereby supporting the region’s high‑volume surgical landscape.

2. Europe Autotransfusion Devices Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising surgical volume, heightened awareness of patient blood management, and supportive reimbursement policies that favor autologous transfusion. Restraints stem from high upfront capital costs and stringent regulatory requirements for device validation. Challenges involve integrating new technology into legacy hospital infrastructure and ensuring staff training. Opportunities arise from technological innovations such as compact, single‑use systems, and expanding applications in trauma and organ‑transplant procedures, which can unlock untapped market segments.

3. Europe Autotransfusion Devices Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward disposable, single‑use autotransfusion kits that simplify workflow and improve safety. Emerging trends include the integration of automated data analytics for inventory management and the development of hybrid devices that combine cell‑salvage with point‑of‑care diagnostics. Additionally, hospitals are adopting bundled procurement models, driving volume sales of both products and accessories across the region.

4. COVID-19 Impact on the Europe Autotransfusion Devices Market - Pandemic effects and recovery trajectory?

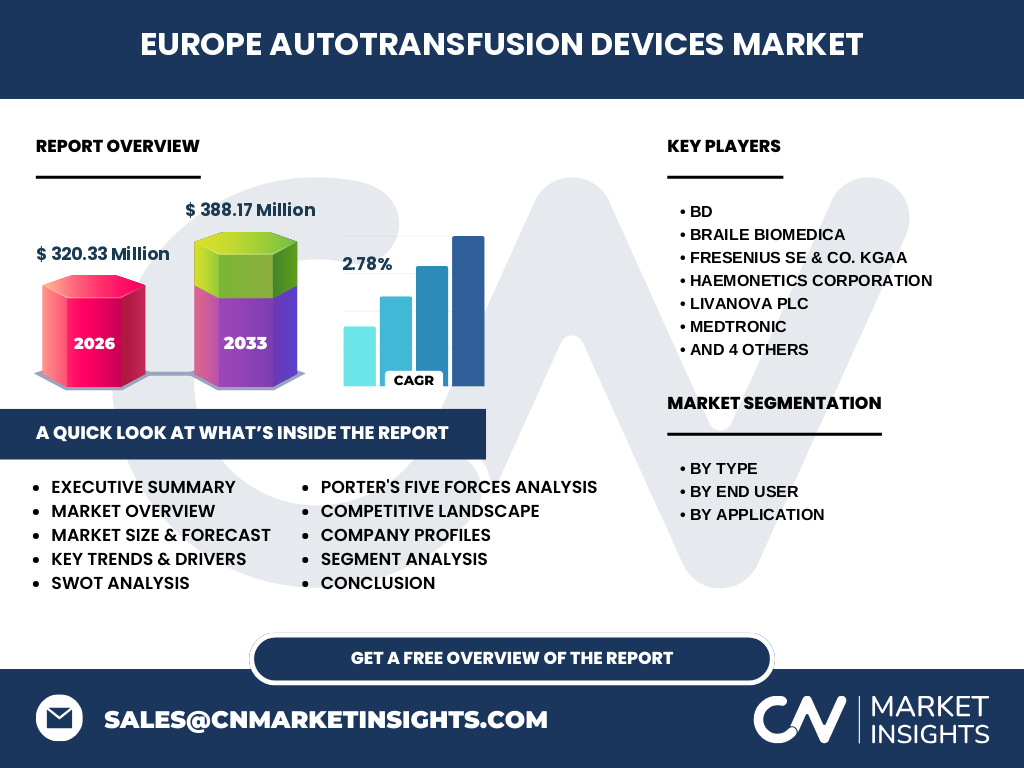

The COVID‑19 pandemic temporarily slowed elective surgeries, leading to a short‑term dip in device utilisation. However, the crisis accelerated risk‑based blood management protocols, reinforcing the value of autotransfusion. Post‑pandemic, elective procedures have rebounded, and hospitals are prioritising blood‑conserving technologies, resulting in a steady recovery that aligns with the projected CAGR of 2.78% through 2033.

5. Europe Autotransfusion Devices Market Competitive Landscape - Major competitors and market consolidation?

The market is moderately consolidated, with ten leading manufacturers dominating the landscape. Key players such as BD, Haemonetics, Medtronic, and Fresenius SE & Co. KGaA hold strong product portfolios and extensive distribution networks. Recent consolidation activity includes strategic acquisitions and partnerships aimed at broadening product ranges and enhancing service capabilities, reinforcing competitive pressure while fostering innovation.

6. Executive Summary - High-level overview and key findings about Europe Autotransfusion Devices Market?

The Europe autotransfusion devices market was valued at €320.33 million in 2026 and is forecast to reach €388.17 million by 2033, growing at a CAGR of 2.78%. Growth is driven by increasing surgical volumes, patient‑centred blood management policies, and technological advances. Hospitals remain the largest end‑user, while specialty clinics and ambulatory surgery centers are gaining traction. The competitive arena is characterised by a mix of global giants and specialised regional firms, all pursuing innovation and strategic collaborations.

7. Europe Autotransfusion Devices Market Forecast - Projections for 2025-2032 period?

Based on current trends, the market is expected to expand steadily from the 2026 baseline of €320.33 million to €388.17 million by 2033. This growth reflects an annualised increase of approximately 2.78%, supported by expanding applications in cardiac, orthopedic, transplant, and trauma surgeries, as well as gradual adoption in ambulatory settings across Europe.

8. Europe Autotransfusion Devices Market Size and Share by Segmentation - Breakdown by segment?

By type, the market is split between core devices and their accessories, with accessories representing a growing share due to consumable turnover. End‑user segmentation shows hospitals as the primary segment, followed by specialty clinics and ambulatory surgery centers. Application‑wise, cardiac surgeries hold the largest share, while orthopedic procedures, organ transplantation, and trauma interventions each contribute to a diversified demand profile.

9. Global Europe Autotransfusion Devices Market Size and Share by Region - Geographic distribution?

Within the global context, Europe accounts for a substantial portion of autotransfusion device sales, reflecting mature healthcare systems and high surgical activity. While exact global percentages are not disclosed, Europe’s €320.33 million valuation underscores its position as a leading regional market, with growth expectations aligning closely with broader global expansion trends.

10. Regional Analysis of the Europe Autotransfusion Devices Market - Detailed regional market performance?

Western European countries such as Germany, France, and the United Kingdom demonstrate the highest adoption rates due to advanced hospital networks and supportive reimbursement frameworks. Northern Europe shows strong growth driven by early technology adoption, while Southern and Eastern European markets present emerging opportunities as healthcare infrastructure upgrades continue and cost‑efficiency pressures rise.

11. Leading Company Profiles in the Europe Autotransfusion Devices Market - Industry players and strategies?

Leading firms include BD, Braile Biomedica, Fresenius SE & Co. KGaA, Haemonetics, LivaNova, Medtronic, Redax S.p.A., SARSTEDT AG & Co. KG, Teleflex, and Zimmer Biomet. Their strategies focus on product innovation, expanding service contracts, and leveraging partnerships to broaden market reach. Many are investing in R&D for miniaturised, single‑use systems and targeting emerging end‑users such as ambulatory surgery centers.

12. Porter's Five Forces Analysis of the Europe Autotransfusion Devices Market - Competitive forces assessment?

Threat of new entrants is moderate due to high regulatory barriers and capital intensity. Bargaining power of suppliers is low, as component sourcing is diversified. Bargaining power of buyers is moderate; large hospital groups can negotiate volume discounts. Threat of substitutes remains low because alternative blood management methods cannot fully replicate autotransfusion efficiency. Industry rivalry is high, driven by product differentiation and aggressive marketing among the top ten players.

13. SWOT Analysis of the Europe Autotransfusion Devices Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established clinical benefits, cost savings, and strong regulatory backing. Weaknesses: High initial equipment cost and complexity of device integration. Opportunities: Expansion into ambulatory surgery centers, development of disposable kits, and digital connectivity for device monitoring. Threats: Potential price pressure from healthcare payers and rapid technological shifts that could render existing platforms obsolete.

14. Europe Autotransfusion Devices Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (e.g., medical‑grade plastics, sensors), proceeds to component manufacturers, then to system integrators who assemble complete devices. Afterward, distributors and OEM partners deliver products to hospitals and clinics, followed by after‑sales service and consumable replenishment, which together generate recurring revenue streams.

15. Key Investment Insights in the Europe Autotransfusion Devices Market - Strategic investment recommendations?

Investors should focus on companies that offer integrated solutions combining hardware, consumables, and data services, as this model drives recurring revenue. Targeting firms with strong presence in high‑growth regions (e.g., Northern Europe) and a pipeline of single‑use technologies can enhance portfolio returns. Strategic M&A in the accessories segment may also provide quick market share gains.

16. Europe Autotransfusion Devices Market Conclusion - Summary and key takeaways?

The European autotransfusion devices market is on a steady growth path, supported by clinical demand, policy encouragement, and innovation. With a projected market size of €388.17 million by 2033 and a 2.78% CAGR, the sector offers attractive opportunities for manufacturers and investors alike, particularly in emerging end‑users and disposable‑device segments.

17. Research Methodology - How this research was conducted?

Primary data were collected through interviews with key opinion leaders, hospital procurement managers, and company executives. Secondary sources included industry reports, regulatory filings, and financial statements of listed manufacturers. Data triangulation ensured consistency, and market sizing was derived using a bottom‑up approach, aggregating product‑level revenues across the defined segments.

18. Research Scope - Coverage and limitations?

The study covers the European autotransfusion device market from 2026 to 2033, segmented by type, end‑user, and application. It focuses on major manufacturers and excludes niche, non‑commercial devices. Geographic granularity is limited to regional trends rather than country‑specific market shares, reflecting the available data set.

19. Key Companies and Recent Developments in the Europe Autotransfusion Devices Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent highlights include BD’s launch of a next‑generation cell‑salvage system with integrated data analytics, Haemonetics’ partnership with a leading European hospital network to expand autotransfusion services, and Medtronic’s acquisition of a niche accessories maker to strengthen consumable offerings. Fresenius announced a collaboration with a specialty clinic consortium to pilot disposable kits, while Zimmer Biomet introduced a compact device tailored for orthopedic surgeries, underscoring the industry’s focus on innovation and strategic alliances.