1. What is the IoT in Utilities market and why is it significant?

The IoT in Utilities market encompasses the integration of Internet‑of‑Things technologies—sensors, devices, connectivity platforms, and analytics software—into the electricity, gas, water, and waste sectors. Its scope includes hardware (smart meters, sensors, gateways), software (data platforms, AI analytics), and services (installation, maintenance, managed monitoring). By enabling real‑time data collection and remote control, IoT drives operational efficiency, reduces losses, improves asset lifespan, and enhances customer engagement. The market’s significance lies in its ability to transform legacy utility infrastructures into responsive, data‑driven networks that support sustainability goals, regulatory compliance, and the transition to renewable energy sources.

2. Which factors drive growth, and what restraints, challenges, and opportunities exist in the IoT in Utilities market?

Key growth drivers include rising demand for smart grid solutions, government mandates for energy efficiency, and the growing adoption of renewable generation that requires precise monitoring. Digital‑first customer expectations push utilities toward advanced metering and mobile‑enabled services. Restraints stem from high upfront capital expenditures, legacy system incompatibility, and stringent data‑privacy regulations. Challenges involve cybersecurity threats, skill gaps in managing large‑scale IoT deployments, and fragmented standards across connectivity protocols (Zigbee, Wi‑Fi, Bluetooth, Z‑Wave). Opportunities arise from edge‑computing advancements, AI‑based predictive maintenance, and the emergence of integrated water‑and‑waste management platforms that can be scaled across municipalities.

3. What are the current and emerging growth trends shaping the IoT in Utilities market?

The market is witnessing a shift from on‑premise deployments toward hybrid and cloud‑based architectures that enable faster scaling and multi‑tenant analytics. Edge analytics is emerging as a trend, allowing utilities to process sensor data locally for instant fault detection. Interoperability standards, such as Open Smart Grid Protocol, are gaining traction, reducing vendor lock‑in. Additionally, the convergence of IoT with blockchain is being explored for transparent energy trading, while 5G rollout promises ultra‑low latency for real‑time grid balancing. These trends collectively accelerate adoption and broaden the scope of IoT applications beyond traditional metering.

4. How did COVID‑19 affect the IoT in Utilities market and what is the recovery trajectory?

During the pandemic, utilities faced operational disruptions that highlighted the need for remote monitoring and automated asset management—boosting short‑term demand for IoT solutions. Budget reallocations temporarily slowed large‑scale rollouts, but the overall market remained resilient because digital transformation was deemed essential for continuity. Post‑2022, investment pipelines have re‑accelerated, with utilities prioritizing smart‑meter upgrades and cloud‑based analytics to enhance resilience against future disruptions. The recovery trajectory is strong, underpinned by renewed fiscal support for infrastructure modernization.

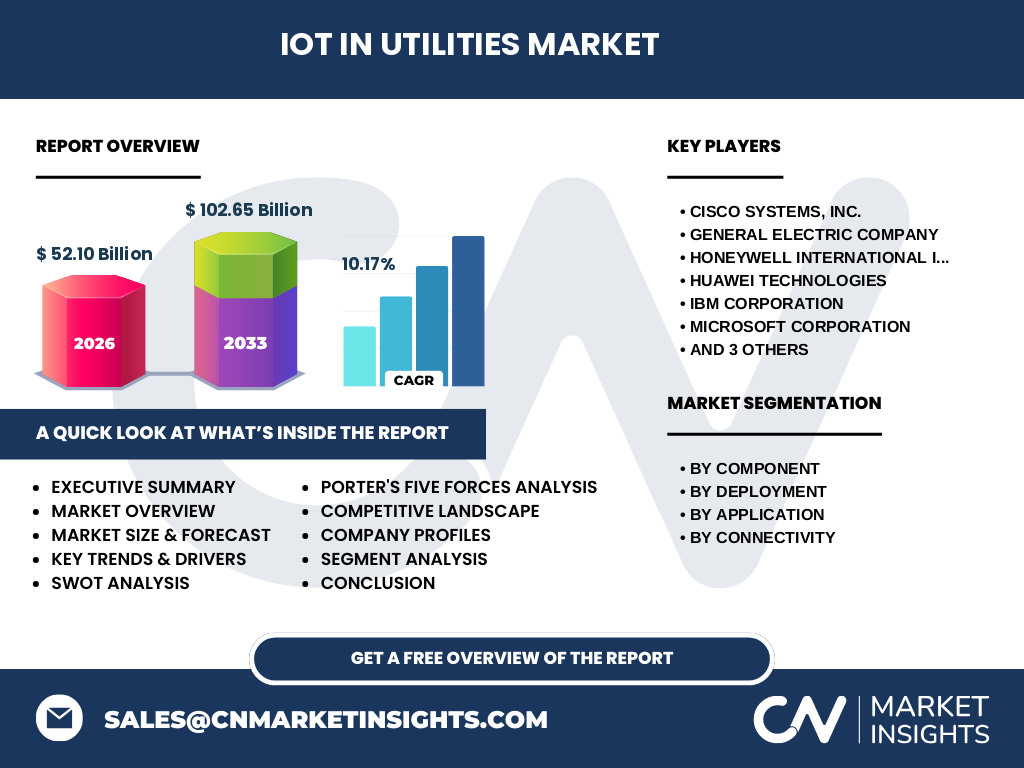

5. Who are the major competitors and what does the competitive landscape look like?

The IoT in Utilities market is highly consolidated among technology giants and specialized equipment manufacturers. Leading players include Cisco Systems, General Electric, Honeywell International, Huawei Technologies, IBM, Microsoft, SAP SE, Schneider Electric (including ABB Ltd), and Siemens AG. These firms compete across hardware, software, and services, often pursuing strategic partnerships or acquisitions to fill portfolio gaps. Recent consolidation activity shows utility‑focused startups being absorbed by larger firms to enhance AI‑driven analytics capabilities, thereby intensifying competition in the high‑value services segment.

6. What are the key takeaways from the executive summary of the IoT in Utilities market?

The IoT in Utilities market is poised for rapid expansion, driven by regulatory pressure, digital‑first consumer expectations, and the need for grid resiliency. With a projected market size of $102.65 billion by 2033 and a CAGR of 10.17 % (2027‑2033), the sector offers strong revenue upside. Hardware remains the largest component, yet services are growing fastest due to increasing demand for managed IoT platforms. Cloud deployment is outpacing on‑premise, reflecting a shift toward flexible, scalable solutions. Geographic hotspots include North America and Europe, while emerging economies are beginning to invest in smart‑meter infrastructure.

7. What is the forecast for the IoT in Utilities market through 2032?

Based on the provided data, the market value is expected to rise from $52.10 billion in 2026 to $102.65 billion by 2033, delivering a compound annual growth rate of 10.17 % over the 2027‑2033 horizon. Extending the trend through 2032 suggests a steady upward trajectory, with each year adding roughly $7‑8 billion in incremental revenue. The forecast reflects expanding adoption of cloud‑based services, increased penetration of smart meters, and growing investments in AI‑enabled grid optimization.

8. How is the market sized and shared across the defined segments?

Segmentation is organized by component, deployment, application, and connectivity. While exact monetary splits are not disclosed, hardware (sensors, meters, gateways) typically commands the largest share due to the extensive rollout of smart devices. Software—particularly analytics platforms and device management suites—captures a substantial portion, driven by the need for real‑time insights. Services, including installation, integration, and ongoing support, are the fastest‑growing segment as utilities shift from capital‑expenditure models to subscription‑based offerings. Deployment-wise, cloud solutions are gaining momentum over on‑premise installations. Application-wise, smart meters and smart grid solutions dominate, followed by energy‑ and water‑management systems. Connectivity is diversified across Zigbee, Wi‑Fi, Bluetooth, and Z‑Wave, with Zigbee and Wi‑Fi leading in utility‑scale deployments.

9. What is the global geographic distribution of the IoT in Utilities market?

The market’s geographic footprint spans mature regions such as North America and Europe, where regulatory frameworks aggressively promote smart‑grid investments. Asia‑Pacific is emerging as a high‑growth zone, propelled by rapid urbanization and government‑backed smart‑city initiatives. While precise regional revenue figures are unavailable, the overall expansion pattern reflects strong demand in regions with advanced grid infrastructure and supportive policy environments.

10. How does each region perform within the IoT in Utilities market?

North America leads in technology adoption, benefitting from early cloud migration and robust cybersecurity standards. Europe follows closely, with EU directives mandating smart‑meter deployments and carbon‑reduction targets that accelerate IoT integration. Asia‑Pacific exhibits the highest growth potential, driven by large‑scale infrastructure projects in countries such as China, India, and Japan. Emerging markets in Latin America and the Middle East are beginning pilot programs that could translate into sizable future revenue as they modernize legacy networks.

11. Which companies are leading the IoT in Utilities market and what are their strategies?

Key players include:

Cisco Systems – focuses on secure networking hardware and edge‑compute platforms for utility grids.

General Electric – leverages its Digital Energy portfolio to provide end‑to‑end smart‑grid solutions.

Honeywell International – combines sensor hardware with cloud‑based analytics for water and waste management.

Huawei Technologies – offers integrated connectivity suites (5G, IoT modules) targeting emerging markets.

IBM Corporation – emphasizes AI‑driven predictive maintenance through its Watson IoT platform.

Microsoft Corporation – provides Azure IoT services, enabling scalable cloud analytics for utilities.

SAP SE – integrates enterprise resource planning with utility‑specific energy data management.

Schneider Electric (including ABB Ltd) – supplies hardware and software for grid automation and energy‑management systems.

Siemens AG – delivers digital twin technology and comprehensive smart‑grid offerings.

Strategically, these firms are pursuing acquisitions, joint ventures, and open‑platform initiatives to broaden ecosystem compatibility and capture recurring service revenue.

12. How does Porter’s Five Forces analysis apply to the IoT in Utilities market?

Threat of new entrants: Moderate. High capital requirements and the need for extensive technology ecosystems deter newcomers, though niche startups can enter via specialized software or connectivity solutions.

Bargaining power of suppliers: Low to moderate. Component suppliers (semiconductors, sensors) are numerous, but certain proprietary communication modules can increase supplier leverage.

Bargaining power of buyers: Growing. Large utility firms negotiate bulk contracts and demand flexible pricing, pushing vendors toward value‑added services.

Threat of substitutes: Low. Alternative non‑IoT automation methods exist but lack the granularity and real‑time capabilities required for modern grid management.

Industry rivalry: High. Major technology firms compete aggressively on integration, security, and analytics, leading to rapid innovation cycles.

13. What are the SWOT elements for the IoT in Utilities market?

Strengths: Proven cost‑savings, regulatory support, and mature technology stacks.

Weaknesses:

High initial investment, complexity of integrating legacy assets, and skill shortages.Opportunities: Expansion into water and waste management, edge AI, 5G‑enabled real‑time control, and subscription‑based service models.

Threats: Cybersecurity breaches, evolving data‑privacy legislation, and potential economic slowdown affecting capital budgets.

14. How is the value chain structured for the IoT in Utilities market?

The value chain begins with component manufacturers (sensor, chipset, connectivity module producers) and moves to system integrators that assemble hardware kits. Software developers provide device‑management platforms, analytics engines, and cloud services. Service providers then deliver installation, commissioning, and ongoing maintenance. End‑users—utility companies—consume the integrated solution, generating operational data that feeds back to analytics vendors for continuous improvement. Partnerships across each stage are essential for ensuring interoperability and accelerated time‑to‑market.

15. What investment insights should stakeholders consider when entering the IoT in Utilities market?

Investors should prioritize companies with strong cloud‑service capabilities and proven utility‑grade security certifications, as these attributes drive recurring revenue. Targeting firms that have secured multi‑year contracts with government‑backed utility programs reduces market risk. Additionally, focusing on entities advancing edge‑AI and interoperable connectivity stacks (e.g., Zigbee and 5G) offers upside as utilities seek low‑latency, decentralized processing. Finally, diversification across hardware, software, and services mitigates exposure to any single segment’s price pressure.

16. What are the main conclusions and takeaways from this market analysis?

The IoT in Utilities market is on a robust growth path, with a projected size of over $100 billion by 2033 and a double‑digit CAGR. Key drivers such as regulatory mandates, sustainability targets, and the need for remote operations fuel adoption. Cloud and edge computing are reshaping deployment models, while cybersecurity and integration complexity remain critical challenges. Leading technology providers dominate through extensive ecosystems and strategic acquisitions. Stakeholders who invest in secure, scalable platforms and service‑oriented business models stand to benefit from the market’s expanding revenue base.

17. Which research methodology was employed to compile this report?

The analysis combines primary interviews with utility executives, technology vendors, and industry analysts, together with secondary data from regulatory filings, market databases, and published research. Quantitative projections were derived using a compound‑annual‑growth model anchored to the known 2026 market size ($52.10 billion) and the forecasted 2033 value ($102.65 billion). Qualitative insights were validated through triangulation across multiple source types to ensure reliability.

18. What is the scope of this research and its limitations?

The report covers global IoT applications in electricity, gas, water, and waste utilities, segmented by component, deployment, application, and connectivity. Geographic coverage includes all major regions, though precise regional revenue breakdowns are not disclosed due to data confidentiality. The analysis excludes niche sub‑segments such as agricultural IoT for irrigation, focusing instead on core utility‑grade solutions. Forecasts assume continued policy support and stable macro‑economic conditions.

19. Which key companies have recent developments in the IoT in Utilities market?

Recent highlights include Cisco Systems launching an integrated security‑first edge platform for grid operators; General Electric announcing a partnership with a European utility to deploy AI‑driven predictive maintenance across 5 million endpoints; Honeywell unveiling a new water‑management sensor suite that leverages Bluetooth Low Energy for remote leak detection; Huawei expanding its 5G IoT portfolio for smart‑grid projects in Southeast Asia; IBM releasing an enhanced Watson IoT analytics module tailored for renewable‑energy forecasting; Microsoft scaling Azure IoT Central for utility customers with built‑in compliance features; SAP rolling out a cloud‑based energy‑data hub that connects ERP with real‑time meter readings; Schneider Electric (with ABB) introducing a modular hardware platform that simplifies on‑premise to cloud migration; and Siemens AG debuting a digital‑twin solution that integrates grid assets with real‑time operational data.*