What is the Electronics Thermal Management Materials Market Overview – definition, scope, and significance?

The Electronics Thermal Management Materials Market comprises products designed to dissipate, spread, or store heat generated by electronic components. It spans conductive adhesives, thermal films, gap fillers, gels, phase‑change materials, and greases, serving consumer electronics, automotive, aerospace, and telecommunications. Efficient thermal management is critical for device reliability, performance, and lifespan, making this market a foundational pillar of modern electronics manufacturing.

What are the main drivers, restraints, challenges, and opportunities shaping the Electronics Thermal Management Materials Market?

Key drivers include rising power densities in chips, growth of electric‑vehicle electronics, and expanding data‑center infrastructure. Restraints stem from high material costs and stringent environmental regulations. Challenges involve material compatibility with miniaturized designs and supply‑chain constraints. Opportunities arise from emerging 5G and AI applications, novel nanocomposite materials, and increasing adoption of phase‑change solutions for compact devices.

Which growth trends are currently influencing the Electronics Thermal Management Materials Market?

Current trends feature a shift toward lightweight, high‑conductivity polymer composites, integration of thermal management directly into printed circuit boards, and the use of smart materials that adapt conductivity with temperature. Additionally, manufacturers are pursuing greener formulations, while the automotive sector is driving demand for flexible gap fillers that withstand vibration and extreme temperatures.

How did COVID‑19 impact the Electronics Thermal Management Materials Market and what is the recovery trajectory?

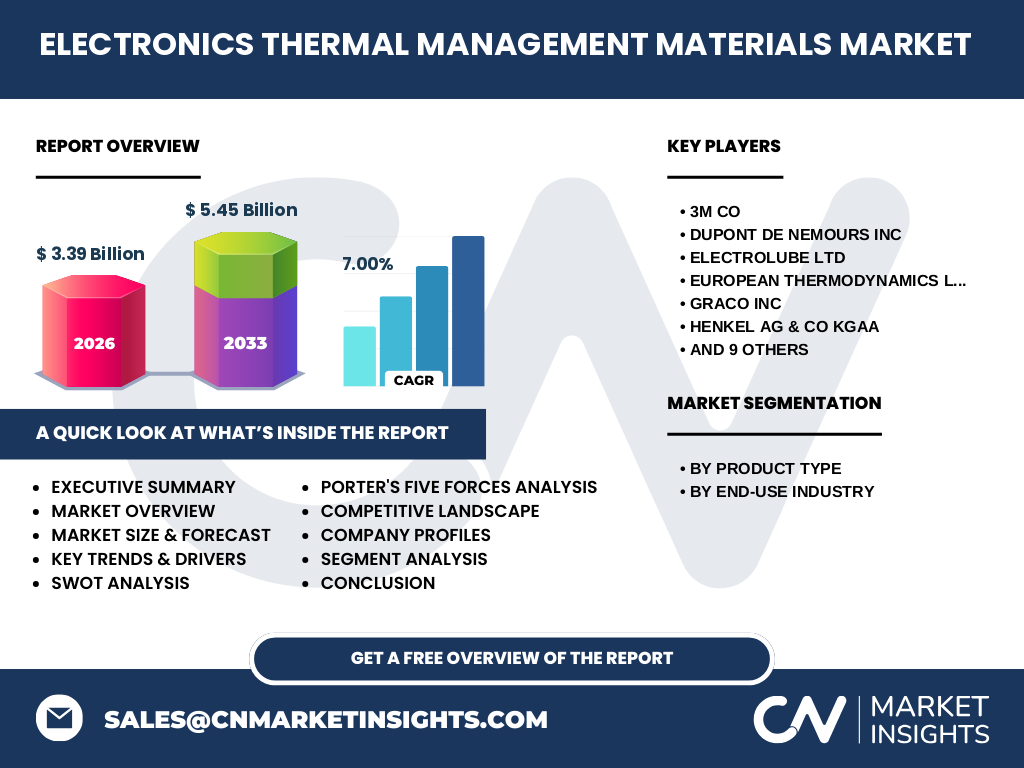

The pandemic caused temporary disruptions in supply chains and a slowdown in consumer‑electronics production, leading to a short‑term dip in demand. However, accelerated digital transformation, remote work, and the surge in data‑center expansion have propelled a rapid rebound. Recovery is evident in the projected CAGR of 7% from 2027 to 2033, indicating robust post‑pandemic growth.

What does the competitive landscape look like for the Electronics Thermal Management Materials Market?

The market is moderately consolidated, with a mix of multinational chemical giants and specialized niche firms. Leaders such as 3M, DuPont, Henkel, and Honeywell command significant product portfolios, while companies like Electrolube, Momentive, and Wacker Chemie focus on high‑performance specialty grades. Recent consolidation includes strategic acquisitions to broaden thermal‑gel and phase‑change capabilities.

Can you provide an executive summary of the key findings about the Electronics Thermal Management Materials Market?

The market reached a size of $3.39 billion in 2026 and is projected to grow to $5.45 billion by 2033, reflecting a 7% CAGR. Growth is fueled by higher thermal loads in electronics, expanding automotive electrification, and demand for efficient cooling in telecom infrastructure. Product diversification, especially in phase‑change and nanocomposite materials, offers lucrative opportunities, while cost pressures and regulatory compliance remain focal challenges.

What are the forecast expectations for the Electronics Thermal Management Materials Market from 2025 to 2032?

Based on the provided CAGR of 7%, the market is expected to sustain steady expansion, moving from the 2026 baseline of $3.39 billion toward the 2033 forecast of $5.45 billion. This trajectory suggests incremental annual growth, driven by continuing miniaturization of electronics, higher power outputs, and broader adoption of electric‑vehicle platforms that require advanced thermal solutions.

How is the market size and share divided by product type and end‑use industry?

By product type, the market is segmented into conductive adhesives, thermal management films, gap fillers, thermal gels, phase‑change materials, and thermal greases. Each segment addresses specific cooling challenges—adhesives for component bonding, films for thin‑profile heat spreading, gap fillers for uneven interfaces, gels and greases for high‑temperature stability, and phase‑change materials for transient thermal spikes. End‑use industries include consumer electronics, automotive, aerospace, and telecommunications, with consumer electronics and automotive representing the largest demand pools due to high device density and electrification trends.

What is the global market size and share by region?

The global market totals $3.39 billion in 2026, expanding to $5.45 billion by 2033. While specific regional dollar figures are not disclosed, the market is broadly distributed across North America, Europe, Asia‑Pacific, and Rest of World, each contributing to the overall growth through distinct application drivers such as semiconductor manufacturing in Asia‑Pacific and aerospace projects in Europe.

What does the regional analysis reveal about market performance?

Asia‑Pacific leads in volume due to large-scale consumer‑electronics production and rapid automotive electrification. North America shows strong growth in data‑center and telecom sectors, while Europe maintains a steady share driven by aerospace and stringent regulatory standards fostering high‑performance thermal solutions. Emerging markets in Latin America and the Middle East are beginning to adopt advanced thermal materials as local manufacturing capabilities expand.

Which companies are leading the Electronics Thermal Management Materials Market and what strategies are they employing?

Key players include 3M, DuPont, Henkel, Honeywell, and Wacker Chemie. Their strategies encompass product innovation (e.g., nanocomposite greases), strategic partnerships with semiconductor manufacturers, acquisitions of niche product lines, and sustainability initiatives to develop low‑VOC and recyclable thermal compounds. Smaller firms such as Electrolube and Momentive focus on specialized high‑temperature gap fillers to capture niche segments.

How does Porter’s Five Forces framework apply to the Electronics Thermal Management Materials Market?

Supplier power is moderate because raw materials like silicone and ceramic powders are sourced from a limited pool of suppliers. Buyer power is high, especially from large OEMs demanding performance guarantees and cost efficiencies. Threat of new entrants is low due to high R&D costs and regulatory barriers. Substitute products are limited, reinforcing market stability. Competitive rivalry is intense, driving continuous innovation and pricing pressure.

What are the SWOT insights for the Electronics Thermal Management Materials Market?

Strengths: Critical role in device reliability; diversified product portfolio.

Weaknesses: High material costs; complex certification processes.

Opportunities: Growth of electric vehicles, 5G infrastructure, and AI chips; emergence of bio‑based thermal compounds.

Threats: Regulatory constraints on hazardous substances; supply‑chain disruptions for specialty fillers.

How is the value chain structured for the Electronics Thermal Management Materials Market?

The value chain begins with raw‑material suppliers (silica, alumina, polymer resins), moves to formulation and compound manufacturing, followed by product testing and certification. Distribution channels include direct sales to OEMs, distributors, and online platforms. End‑users integrate the materials during assembly, and after‑sales services encompass technical support and material‑performance monitoring.

What key investment insights can be drawn for stakeholders in the Electronics Thermal Management Materials Market?

Investors should focus on companies with strong R&D pipelines in nanocomposite and phase‑change technologies, as these segments promise higher margins. Strategic acquisitions of niche gap‑filler producers can accelerate market entry. Additionally, funding sustainability‑focused material development aligns with upcoming regulatory trends and offers differentiation in competitive bids.

What are the main conclusions and takeaways from this market analysis?

The market is on a solid growth path, reaching $5.45 billion by 2033 with a 7% CAGR. Demand is propelled by higher power densities and electrification across multiple industries. Innovation in high‑conductivity, environmentally friendly materials will be decisive. Companies that invest in advanced formulations and strategic partnerships are poised to capture the expanding opportunity.

Which research methodology was employed to compile this report?

The study combined primary interviews with industry experts, secondary data from company filings, market databases, and trade publications. Quantitative analysis used historical sales data to validate the 2026 market size, while forward‑looking models applied the disclosed 7% CAGR to generate the 2033 forecast. Competitive benchmarking and SWOT assessments were derived from the same sources.

What is the scope of this research and its coverage limitations?

The scope covers global market size, product‑type and end‑use segmentation, regional distribution, and competitive dynamics for the period 2025‑2033. Limitations include the use of publicly available financial figures only; detailed regional revenue breakdowns and market‑share percentages beyond the aggregate figures are not provided.

Which key companies have announced recent developments in the Electronics Thermal Management Materials Market?

Recent announcements include 3M launching a low‑viscosity thermal adhesive for smartphones, DuPont unveiling a high‑temperature silicone gel for aerospace, Henkel introducing a recyclable phase‑change material, and Honeywell releasing a conductive adhesive optimized for electric‑vehicle battery modules. Additionally, Wacker Chemie announced a partnership with a leading data‑center provider to supply custom thermal greases, while Momentive disclosed a new line of gap fillers with enhanced thermal conductivity.