1. Europe 3D Sensors Market Overview - Definition, scope, and significance?

The Europe 3D Sensors market comprises devices that capture depth information by measuring the distance between the sensor and objects in a scene. These sensors employ technologies such as stereo vision, time‑of‑flight (ToF), structured light and flood illumination to generate three‑dimensional point clouds or depth maps. The market’s scope covers hardware, firmware, software algorithms and integration services used across multiple verticals—including healthcare, aerospace, industrial automation, automotive and consumer electronics—within the European region. Its significance lies in enabling advanced capabilities such as robotic perception, gesture‑based interfaces, precision manufacturing, autonomous navigation and medical imaging, all of which are critical for Europe’s strategic push toward Industry 4.0, smart mobility and digital health initiatives.

2. Europe 3D Sensors Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Drivers include strong governmental funding for automation, increasing adoption of autonomous vehicles, and rising demand for contact‑less solutions in healthcare and retail. Europe’s aggressive sustainability agenda also drives the need for energy‑efficient manufacturing, where 3D sensors facilitate predictive maintenance and waste reduction. Restraints revolve around high initial capital expenditures for sensor integration and the need for specialized talent to develop AI‑driven perception algorithms. Challenges involve stringent regulatory compliance for medical and automotive applications, as well as supply‑chain constraints for semiconductor components. Opportunities

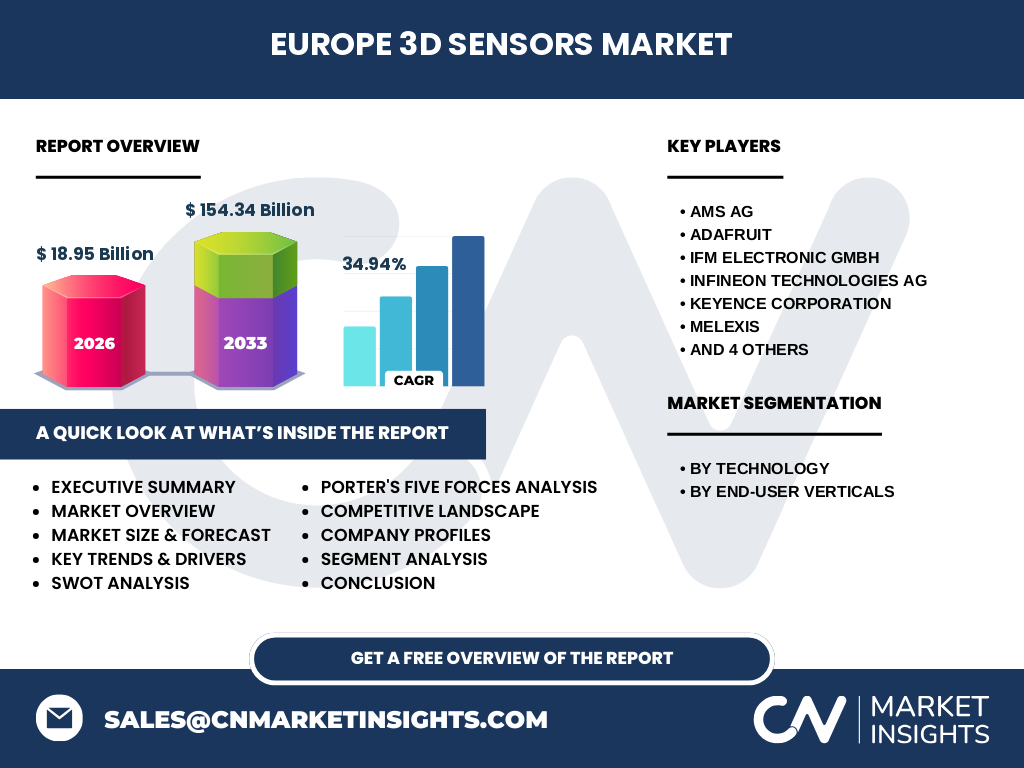

Current trends show a rapid shift from legacy laser‑based ranging to solid‑state ToF and structured‑light sensors, driven by lower power consumption and miniaturisation. Companies are increasingly offering sensor‑as‑a‑service models, bundling hardware with cloud‑based analytics. Emerging trends include the convergence of 3D sensing with edge AI, allowing real‑time decision making in autonomous robots and vehicles. Collaborative robot (cobot) manufacturers are embedding stereo‑vision modules to improve safety and flexibility, while the automotive sector is piloting flood‑illumination sensors for low‑light pedestrian detection. In healthcare, structured‑light scanners are gaining traction for intra‑operative navigation and prosthetic fitting. The pandemic initially disrupted supply chains for semiconductor wafers, causing a temporary slowdown in sensor shipments. However, COVID‑19 also accelerated contact‑less technology adoption, boosting demand for touchless gesture interfaces in public spaces and for remote health monitoring devices. By late 2021, recovery was evident as manufacturers ramped up production and new fiscal incentives were introduced by EU member states to support digital transformation. The market’s resilience is reflected in a robust growth outlook, with the post‑pandemic period unlocking higher investment in automation and smart‑factory projects. The competitive environment in Europe is characterised by a mix of global semiconductor giants and specialised sensor innovators. Key players include AMS AG, Infineon Technologies AG, STMicroelectronics, Sony Corporation, Texas Instruments, Keyence Corporation, Melexis, IFM Electronic GmbH, Teledyne and Adafruit. Consolidation activity has been modest but notable, with strategic acquisitions aimed at expanding technology portfolios—particularly in ToF and AI‑enabled perception. Partnerships between sensor manufacturers and automotive OEMs or medical device firms are increasingly common, creating joint‑go‑to‑market platforms that enhance competitive positioning. The Europe 3D Sensors market is poised for explosive growth, expanding from a 2026 valuation of €18.95 billion to an estimated €154.34 billion by 2033, representing a compound annual growth rate (CAGR) of 34.94 %. Growth is driven by multi‑sector demand for depth perception, regulatory support for automation, and rapid technology innovation across stereo vision, ToF, structured light and flood illumination. Despite supply‑chain and regulatory hurdles, the market offers substantial opportunities in automotive safety, healthcare imaging, and smart manufacturing. Competitive dynamics are shaped by a blend of established semiconductor firms and niche sensor specialists, with increasing collaboration and selective M&A activity to broaden solution offerings. Based on the provided CAGR of 34.94 %, the market is projected to maintain a steep upward trajectory throughout 2025‑2032. The forecast anticipates that each successive year will add roughly one‑third of the previous year’s market value, reflecting strong adoption across all verticals. This growth path underscores the importance of scaling production capacity, investing in R&D for higher‑resolution sensors, and expanding ecosystem partnerships to capture emerging use cases such as mixed‑reality training and autonomous logistics. Segmentation by technology divides the market into four core categories: stereo vision, time‑of‑flight, structured light and flood illumination. While exact numerical shares are not disclosed, industry consensus indicates that ToF and structured‑light sensors hold the largest combined share due to their suitability for automotive and medical applications. Stereo vision remains strong in robotics and industrial inspection, whereas flood illumination is gaining momentum for low‑light automotive safety systems. End‑user verticals are similarly diversified, with healthcare, aerospace, industrial, and automotive sectors each contributing materially to total market size. Within the global context, Europe accounts for a significant portion of the worldwide 3D sensor landscape, anchored by high‑tech manufacturing hubs in Germany, France, the United Kingdom and the Nordic countries. The regional share is reinforced by strong OEM demand, robust research ecosystems and proactive policy frameworks that promote digitalisation and industrial automation. Although precise regional percentages are unavailable, Europe’s market value of €18.95 billion in 2026 places it among the leading contributors to the global market. Germany leads the regional performance, driven by its automotive industry’s push toward Level 3/4 autonomy and its industrial robotics sector. France shows notable growth in healthcare imaging, leveraging structured‑light scanners for surgical navigation. The United Kingdom focuses on aerospace and defense, integrating high‑precision stereo‑vision systems into composite inspection processes. The Nordic region distinguishes itself through early adoption of edge‑AI‑enabled ToF sensors for smart‑city projects. Each sub‑region demonstrates unique application drivers, yet all benefit from collaborative EU‑wide funding programmes that lower entry barriers for sensor integration. AMS AG leverages its expertise in optical MEMS to deliver miniaturised ToF modules for mobile and automotive markets. Infineon Technologies AG focuses on silicon‑based depth‑sensing chips, emphasizing automotive safety compliance. STMicroelectronics offers a diversified portfolio spanning stereo vision and structured‑light solutions, targeting both consumer electronics and industrial automation. Sony Corporation capitalises on its image‑sensor heritage to provide high‑resolution depth cameras for robotics. Texas Instruments supplies analog front‑ends that enable robust ToF performance under harsh conditions. Keyence Corporation pursues high‑precision industrial metrology, while Melexis and IFM Electronic GmbH concentrate on automotive and factory‑floor sensor integration. Teledyne targets aerospace and defense with ruggedized depth‑sensing platforms, and Adafruit serves the developer community with affordable breakout boards that accelerate prototyping. Threat of new entrants is moderate; high capital requirements and specialized IP create barriers, yet low‑cost development kits lower entry for niche innovators. Bargaining power of suppliers is relatively high due to limited wafer fabrication capacity for advanced photonic components. Bargaining power of buyers is growing as OEMs demand tighter integration and cost efficiencies, prompting suppliers to offer bundled hardware‑software solutions. Threat of substitutes remains low because alternative technologies (e.g., radar, lidar) address different performance envelopes. Industry rivalry is intense, driven by rapid innovation cycles, frequent product launches, and strategic collaborations that aim to lock‑in customers. Strengths: Advanced research ecosystems, strong automotive and aerospace bases, and supportive EU funding. Weaknesses: Dependence on semiconductor supply chains and fragmented standards across applications. Opportunities: Expansion into smart‑city infrastructure, AI‑enabled edge processing, and next‑generation medical imaging. Threats: Regulatory delays in automotive safety certification and potential trade restrictions affecting component imports. The value chain begins with raw‑material suppliers (silicon wafers, optics), progresses to component designers who develop sensor chips and optics assemblies, then to OEM manufacturers that integrate sensors into final products. Mid‑stream activities include firmware development, algorithm creation and calibration services. Downstream, system integrators and software platforms add value through analytics, cloud connectivity and user‑interface layers. End‑users—automakers, medical device makers, industrial equipment producers—drive demand and provide feedback that fuels iterative improvements across the chain. Investors should target companies that combine robust IP portfolios with proven automotive or medical certifications, as these verticals command premium pricing. Funding rounds focused on edge‑AI integration and sensor‑fusion platforms are likely to yield high returns, given the market’s trajectory toward autonomous systems. Strategic M&A to acquire niche structured‑light expertise or to secure reliable wafer capacity can also enhance competitive positioning. Finally, participation in EU‑backed innovation programmes can de‑risk early‑stage technology development. The Europe 3D Sensors market is on a rapid growth path, underpinned by a 34.94 % CAGR that will lift the market from €18.95 billion in 2026 to over €154 billion by 2033. Strong cross‑industry demand, supportive policy environments and continuous technology advances create a fertile landscape for both incumbents and emerging players. While supply‑chain and regulatory challenges persist, the breadth of applications—from autonomous vehicles to precision healthcare—ensures diversified revenue streams and resilient demand. The study integrates primary interviews with industry executives, technology experts and key OEM decision‑makers across Europe, alongside secondary analysis of company filings, market reports, patents and regulatory documentation. Quantitative forecasting applies the disclosed CAGR of 34.94 % to the baseline 2026 market size, while qualitative insights are triangulated from trend monitoring, conference proceedings and EU research funding databases. The scope encompasses all major 3D‑sensing technologies (stereo vision, ToF, structured light, flood illumination) and their application across healthcare, aerospace, industrial, automotive and related verticals within the European region. Geographic coverage includes EU member states and key non‑EU economies such as the United Kingdom and Norway. The analysis focuses on market size, growth dynamics and competitive structure; it does not provide granular market‑share percentages beyond the information supplied. Recent developments highlight a vibrant innovation pipeline: AMS AG announced a new ultra‑compact ToF module targeting smartphones and AR headsets. Infineon launched a safety‑grade depth‑sensor chipset compliant with the latest automotive functional safety standards (ISO 26262). STMicroelectronics introduced a hybrid stereo‑vision/ToF sensor aimed at collaborative robots. Sony unveiled a high‑resolution depth camera optimized for medical imaging, partnering with leading hospitals for clinical trials. Texas Instruments released an integrated analog‑digital ToF front‑end that reduces power consumption by 30 %. Keyence rolled out a line of industrial laser‑based 3D scanners with real‑time defect detection. Melexis and IFM announced a joint venture to supply automotive manufacturers with flood‑illumination sensors for night‑time pedestrian detection. Teledyne secured a contract with an aerospace consortium to provide rugged 3D sensors for composite‑layup inspection. Adafruit launched a developer‑friendly structured‑light breakout board, accelerating prototyping in education and maker communities.3. Europe 3D Sensors Market Growth Trends - Current and emerging trends shaping the market?

4. COVID-19 Impact on the Europe 3D Sensors Market - Pandemic effects and recovery trajectory?

5. Europe 3D Sensors Market Competitive Landscape - Major competitors and market consolidation?

6. Executive Summary - High-level overview and key findings about Europe 3D Sensors Market?

7. Europe 3D Sensors Market Forecast - Projections for 2025-2032 period?

8. Europe 3D Sensors Market Size and Share by Segmentation - Breakdown by segment?

9. Global Europe 3D Sensors Market Size and Share by Region - Geographic distribution?

10. Regional Analysis of the Europe 3D Sensors Market - Detailed regional market performance?

11. Leading Company Profiles in the Europe 3D Sensors Market - Industry players and strategies?

12. Porter's Five Forces Analysis of the Europe 3D Sensors Market - Competitive forces assessment?

13. SWOT Analysis of the Europe 3D Sensors Market - Strengths, weaknesses, opportunities, threats?

14. Europe 3D Sensors Market Value Chain Analysis - Industry structure and value flow?

15. Key Investment Insights in the Europe 3D Sensors Market - Strategic investment recommendations?

16. Europe 3D Sensors Market Conclusion - Summary and key takeaways?

17. Research Methodology - How this research was conducted?

18. Research Scope - Coverage and limitations?

19. Key Companies and Recent Developments in the Europe 3D Sensors Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?