What is the North America Flatbread Market Overview – definition, scope, and significance?

The North America Flatbread Market encompasses the production, distribution, and consumption of ready-to-use flatbreads such as tortilla, pita, and naan across the United States, Canada, and Mexico. It includes flatbreads sold through supermarkets, hypermarkets, convenience stores, bakeries, and online retail channels. The market is significant because flatbreads serve as a versatile base for a growing variety of meals—from traditional Mexican tacos to health‑focused wraps—driving broad consumer appeal and supporting a multi‑billion‑dollar food segment.

What are the primary drivers, restraints, challenges, and opportunities shaping the North America Flatbread Market?

Key drivers include increasing demand for convenient, ready‑to‑eat meals, rising interest in ethnic cuisines, and a shift toward healthier, whole‑grain flatbread options. Restraints stem from price sensitivity in commodity‑based ingredients and supply chain volatility for wheat and corn. Challenges involve intense competition from alternative breads and regulatory scrutiny around labeling (e.g., “gluten‑free”). Opportunities arise from product innovation—such as high‑protein or low‑carb formulations—and expansion of online retail, which accelerates reach to younger, digital‑native consumers.

What current and emerging growth trends are influencing the North America Flatbread Market?

Current trends feature a surge in premium flatbreads enriched with seeds, legumes, and functional ingredients. Emerging trends include plant‑based flatbread alternatives made from chickpea or soy flour, and limited‑edition regional flavors that cater to ethnic authenticity. Additionally, the growth of “food‑as‑experience” concepts in restaurants and fast‑casual chains is prompting co‑branding collaborations between flatbread manufacturers and culinary brands.

How did COVID‑19 impact the North America Flatbread Market and what is the recovery trajectory?

The pandemic accelerated home‑cooking and the demand for shelf‑stable, easy‑to‑prepare products, leading to a temporary boost in flatbread sales through supermarkets and online channels. Supply chain disruptions caused short‑term inventory gaps, but the market recovered quickly as consumer confidence returned. Post‑COVID, the trajectory remains positive, supported by sustained interest in convenient meals and continued strength in e‑commerce distribution.

Who are the major competitors and what is the level of market consolidation in the North America Flatbread Market?

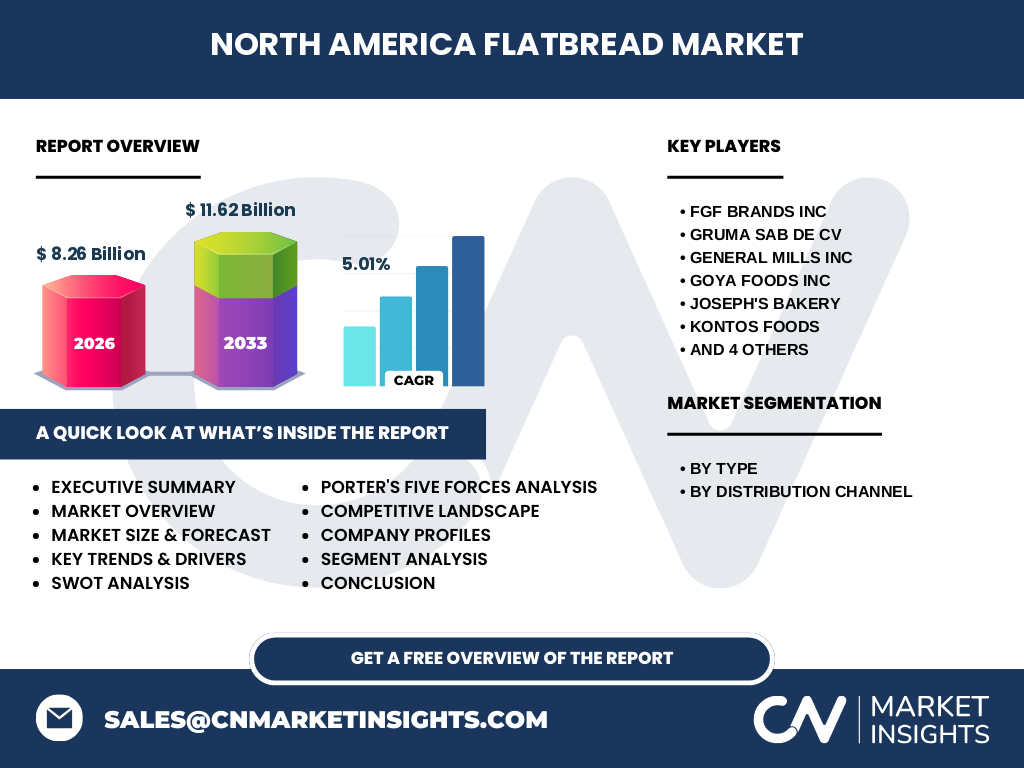

The competitive landscape features a mix of multinational grain processors and specialized bakeries. Prominent players include FGF Brands Inc, GRUMA SAB de CV, General Mills Inc, Goya Foods Inc, Joseph’s Bakery, Kontos Foods, Leighton Foods AS, Mi Rancho, Ol© Mexican Foods Inc., and Toufayan Bakeries. While the market is fragmented with many regional and niche brands, consolidation is evident through strategic acquisitions—particularly by larger grain conglomerates seeking to broaden their flatbread portfolios.

What are the high‑level findings presented in the Executive Summary of the North America Flatbread Market?

The executive summary highlights a market size of $8.26 billion in 2026, projecting growth to $11.62 billion by 2033, representing a compound annual growth rate (CAGR) of 5.01 %. Growth is driven by health‑forward product innovation, expanding ethnic food consumption, and robust online retail channels. Key insights stress the importance of diversifying product lines (tortilla, pita, naan) and leveraging distribution strengths in supermarkets and e‑commerce to capture incremental demand.

What are the forecasted market dynamics for the North America Flatbread Market from 2025 to 2032?

Forecasts indicate a steady upward trajectory, with the market expanding from its 2026 baseline of $8.26 billion to surpass $11.6 billion by the end of the forecast horizon. The 5.01 % CAGR suggests consistent demand across all flatbread types, with the greatest growth anticipated in specialty and health‑focused segments. Distribution trends forecast continued gains for online retail, while traditional supermarket channels remain the volume leaders.

How is the North America Flatbread Market sized and shared across its major segments?

Segmentation is performed by product type—tortilla, pita, and naan—and by distribution channel, including supermarkets & hypermarkets, convenience stores, bakeries, and online retail. While exact monetary shares are not disclosed, the tortilla segment historically commands the largest portion due to its ubiquity in Mexican and Tex‑Mex cuisine. Pita and naan together capture a growing niche, driven by Mediterranean and Indian food trends. Channel-wise, supermarkets & hypermarkets dominate volume, with online retail showing the fastest growth rate.

What is the geographic distribution of the North America Flatbread Market on a regional basis?

The market is concentrated in the United States, which accounts for the bulk of consumption due to its large population and diverse culinary preferences. Canada contributes a smaller but steady share, while Mexico adds regional significance, especially for tortilla products. Overall, the North American region maintains a unified growth pattern, supported by cross‑border trade and similar consumer trends.

What detailed regional analysis can be provided for the North America Flatbread Market?

In the United States, flatbread sales are propelled by both mainstream grocery chains and a vibrant ethnic food sector. The West Coast shows higher adoption of health‑oriented flatbreads, whereas the Southwest leads in tortilla volume. Canada’s market growth aligns with increasing multicultural demographics and a rising demand for gluten‑free pita options. Mexico remains a key supplier and consumer of tortillas, influencing price dynamics across the continent.

Which leading companies are operating in the North America Flatbread Market and what are their strategic approaches?

FGF Brands Inc focuses on value‑priced tortilla lines for mass retailers. GRUMA SAB de CV leverages its global grain expertise to launch fortified flatbreads. General Mills Inc integrates flatbread products into its broader snack portfolio, emphasizing convenience. Goya Foods Inc targets Hispanic consumers with authentic tortilla and pita offerings. Joseph’s Bakery differentiates through artisanal, bakery‑fresh flatbreads. Kontos Foods and Leighton Foods AS concentrate on specialty and premium segments, while Mi Rancho, Ol© Mexican Foods Inc., and Toufayan Bakeries serve niche regional markets.

How does Porter’s Five Forces analysis apply to the North America Flatbread Market?

• Threat of new entrants: Moderate, due to capital requirements for large‑scale baking facilities but lower barriers for niche artisanal brands. • Bargaining power of suppliers: Moderate, as wheat and corn are commodity inputs with multiple sources, yet price volatility can affect margins. • Bargaining power of buyers: High, especially large retailers that demand competitive pricing and extensive SKU assortments. • Threat of substitutes: High, with alternative breads, wraps, and low‑carb options competing for shelf space. • Industry rivalry: Intense, driven by product innovation, pricing battles, and aggressive promotional activities among the listed key players.

What SWOT insights can be drawn for the North America Flatbread Market?

Strengths: Established consumer base, versatile product applications, and strong distribution networks. Weaknesses: Sensitivity to raw‑material cost fluctuations and limited differentiation among basic tortilla products. Opportunities: Development of functional flatbreads (high‑protein, fortified), expansion of online sales, and co‑branding with restaurant chains. Threats: Rising competition from low‑carb wraps, potential regulatory changes on labeling, and supply chain disruptions.

What does the value chain of the North America Flatbread Market look like?

The value chain begins with raw‑material sourcing (wheat, corn, alternative flours), followed by dough preparation, baking, and packaging. Distribution splits into three main pathways: direct supply to large retailers, wholesale to smaller convenience stores and bakeries, and fulfillment through e‑commerce logistics providers. End‑users include household consumers, food‑service operators, and institutional buyers. Value‑adding activities such as fortification, flavor innovation, and sustainable packaging occur primarily at the manufacturing stage.

What key investment insights are recommended for stakeholders in the North America Flatbread Market?

Investors should prioritize companies with robust R&D pipelines targeting health‑focused flatbreads and those expanding digital sales capabilities. Acquisitions of niche artisanal bakeries can provide rapid entry into premium segments. Additionally, financing initiatives that improve supply‑chain resiliency—such as diversified grain sourcing contracts—will mitigate raw‑material risk and support sustained margin growth.

What conclusions can be drawn about the North America Flatbread Market?

The market demonstrates solid growth prospects, underpinned by a 5.01 % CAGR and a projected increase from $8.26 billion to $11.62 billion by 2033. Consumer trends toward convenience, health, and ethnic diversity are driving product innovation across tortilla, pita, and naan categories. While competition is fierce, firms that capitalize on online channels, functional ingredients, and strategic partnerships are positioned to capture the most value.

How was the research for this report conducted?

Research methodology combined primary interviews with industry executives, secondary analysis of company filings, trade publications, and market databases. Data triangulation ensured consistency across product type, distribution channel, and regional insights. Forecast modeling applied historical growth patterns and macro‑economic indicators to derive the 5.01 % CAGR projection.

What is the scope of this research and what limitations should readers be aware of?

The scope covers flatbread products (tortilla, pita, naan) sold in North America across listed distribution channels. Geographic focus includes the United States, Canada, and Mexico. The analysis does not extend to flatbreads produced for export or specialty segments outside the defined product categories. Financial figures are limited to the provided market size, forecast, and CAGR.

Which key companies have made recent developments in the North America Flatbread Market?

FGF Brands Inc announced a new line of whole‑grain tortillas aimed at health‑conscious shoppers. GRUMA SAB de CV launched fortified pita breads with added calcium and iron. General Mills Inc entered a partnership with a leading fast‑casual chain to supply ready‑to‑heat naan wraps. Goya Foods Inc introduced a gluten‑free tortilla range. Joseph’s Bakery expanded its bakery‑fresh pita distribution to additional regional grocery chains. Kontos Foods unveiled a plant‑based flatbread targeting vegans, while Leighton Foods AS released a limited‑edition spice‑infused naan. Mi Rancho, Ol© Mexican Foods Inc., and Toufayan Bakeries have each reported capacity upgrades to meet growing demand.